Overview of Basic Investing

A no-fluff rundown of investing basics — what markets actually do, asset allocation vs. security selection, the EMH, and money market instruments like T-bills and CDs.

OK so let’s just get into it.

1. What financial markets actually do

- Informational role

- Lets you shift consumption across time

- Spreads risk around

- Separates ownership from management — which gives you the agency problem (more on that later)

When you invest, there are basically two decisions on the table:

asset allocation and security selection.

If you lean hard on asset allocation? That’s top-down portfolio management.

If you lean hard on security selection? That’s bottom-up.

Going bottom-up means you’re hunting for individual names that look attractively priced — which means you’d better be sharp at securities analysis, and you’re more exposed to “oops I was wrong” risk.

Knowing this little checklist doesn’t really mean you understand finance. lol but I’m writing it down anyway because, you know, exam.

Risk-return tradeoff

High risk, high return. That’s the whole thing. Moving on.

Efficient market hypothesis

The hypothesis: prices already bake in all the info available to investors. If that’s true, then “undervalued” or “overvalued” securities don’t really exist.

If you don’t buy it → go active.

If you kiiinda buy it → go passive.

The book says we’ll get into how the wildly creative active-management folks try to find profit anyway in Part 6.

Real vs. financial assets

- Real assets: stuff that actually generates income.

- Financial assets: stuff that says how that income/wealth gets divvied up among investors.

Step one for this whole book is getting comfortable with financial assets, so let’s start there.

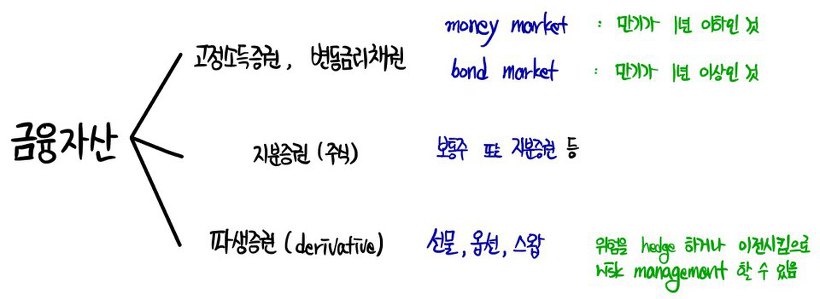

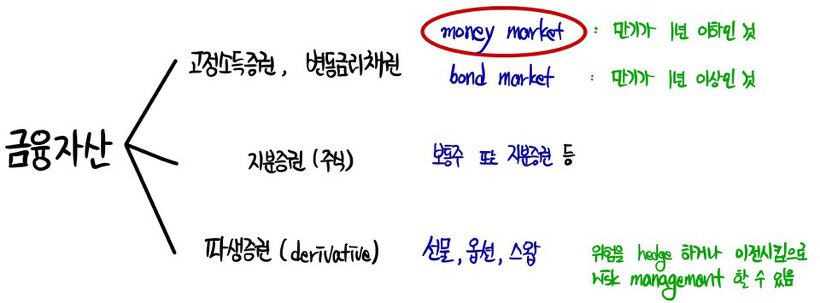

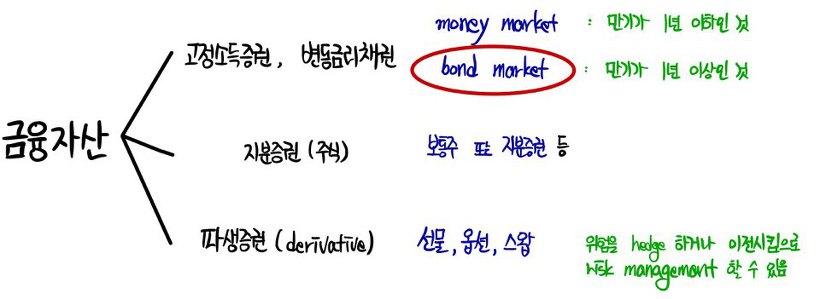

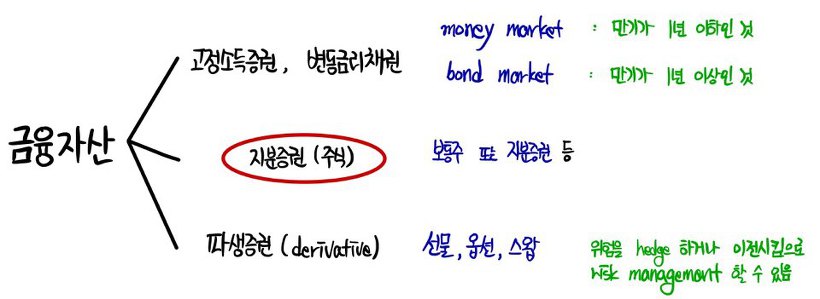

Financial assets split into three buckets:

- Fixed income

- Equities (stocks)

- Derivatives

Money market

1. U.S. Treasury bill

The most liquid thing in the money market, full stop.

When it matures, whoever’s holding it gets paid the face value. Maturities all over the place — 4 weeks, 13 weeks, 26 weeks, 52 weeks, etc.

Price risk basically zero — because, uh, the U.S. can’t go bankrupt. Why? Because they can just print dollars. Easy.

Minimum unit is $100, which is *cheap* (most other money-market stuff has a $10,000 minimum).

Exempt from state and local taxes.

There’s an ask price (sell) and a bid price (buy), so yeah — there’s a spread.

The yield is annualized on a 360-day basis using the bank-discount method. heh.

2. Certificate of deposit (CD)

It’s a kind of time deposit, so you can’t just yank your money out whenever.

BUT — CDs issued at $100,000 or more are transferable, so you can offload them before maturity. Or use them as an investment vehicle.

Short-term CDs: liquid. CDs of 3 months or longer: barely any liquidity, apparently.

The book doesn’t say why. Riddle me this.

3. Commercial paper (CP)

Maturity caps out around 270 days — like 9 months max?

Why? Because if you go longer, you have to register with the SEC, and nobody wants that hassle.

So in practice, almost all CP gets issued with a maturity inside 1 or 2 months. Face amounts come in multiples of $100,000.

Most people end up holding it indirectly via money market mutual funds.

(Mutual fund: a bunch of people pool a giant pile of money, then somebody invests it for them.)

4. Banker’s acceptance (BA)

The book’s explanation is genuinely incomprehensible. I’ve covered this one in another book, so I’ll do it from there instead. Skipping for now.

5. Eurodollar

Dollar-denominated deposits sitting in banks outside the U.S.

And get this — even branches of U.S. banks count, as long as they’re physically outside the U.S.

Why?? Because being outside the U.S. means being outside the Fed’s regulatory reach. So they get the separate “Eurodollar” label for that reason.

lol lol lol lol lol lol lol lol lol lol

(Genuinely considering dropping the class.)

Most Eurodollar deposits are large-denomination time deposits with maturities under 6 months.

6. Repurchase agreement (RP)

A form of short-term borrowing — specifically, overnight borrowing.

You sell the bond today with an agreement to buy it back tomorrow at a slightly higher price. Maturity = one day. The “slightly higher” part is your interest.

The central bank uses RPs to mess with the money supply, right…?

7. Federal funds

OK so people park money at banks. Banks park money at the FRB.

The FRB sets a minimum ratio by law — banks have to keep at least that much on deposit there.

The whole pretext is: keep some cash in the vault in case of a bank run.

That stockpile is what we call federal funds. So what does the FRB actually do with it?

When some big bank or financial center in NY runs short on its federal funds requirement → the FRB lends to them. Usually overnight. The interest rate on that loan is the federal funds rate.

Even though the federal funds rate has no direct relationship to investors, supposedly it’s used as one of the reference indicators in the money market, so a lot of eyeballs are on it.

…what kind of logic is that?

The logic of having no logic?

The logic of “even though it doesn’t relate to investors directly, it’s used as an indicator, so people pay attention”? Bro. lol lol lol

8. LIBOR market

London Interbank Offer Rate. The rate big London banks charge each other for loans.

This thing has basically become the benchmark rate in Europe’s money market. So when companies borrow, they’ll quote it like “LIBOR + 2%.”

Same vibe as the federal funds rate, basically.

Bond market

1. Medium- and long-term Treasury bonds

“Medium-term Treasury bond” doesn’t really click as a phrase, but here’s the deal — there’s the U.S. Treasury, right? They issue bonds.

- Maturity ≤ 1 year → Treasury bills (T-bills)

- Maturity 1 to <10 years → Treasury notes (T-notes)

- Maturity ≥ 10 years (up to 30) → Treasury bonds (T-bonds)

All of these pay interest (a “coupon”) every six months.

If the coupon’s, say, 4%! → that means 4% of face value (the number printed on the bond) every half-year.

Yield is reported as yield to maturity — the income you’d get from buying it now and holding through to maturity, expressed as an annualized number.

Chapter 10 goes into the gory details.

2. TIPS (Treasury Inflation-Protected Securities)

The principal is linked to CPI — it scales up as CPI rises.

So in theory, if you hold this thing, your real interest rate carries no risk.

Also covered in Chapter 10.

3. Federal agency debt

Various government-affiliated agencies issue securities under their own names. Think of it as the U.S. version of bonds issued by the Korea Land and Housing Corporation, etc.

- Federal Home Loan Bank: FHLB

- Federal National Mortgage Association: FNMA

- Government National Mortgage Association: GNMA, aka Ginnie Mae

- Federal Home Loan Mortgage Corp: FHLMC, aka Freddie Mac

These guys!!! Who, uh, blew up spectacularly in the 2008 Global Financial Crisis.

(They had a real hand in causing the GFC. Why? Because the government had been quietly backstopping them the whole time.)

For more, see this earlier post: http://gdpresent.blog.me/220590253428

4. International bonds

Do companies only raise funds via securities issued by institutions in their home country?! No no no.

That’s literally why Eurodollars exist, right???

But we’re in bond land now, not money market land. So instead of “Eurodollar,” we’d say Euro Bond, right?!

Quick heads up on terminology though — the “Euro” prefix is kinda misleading. It does not mean “related to the EU.”

It just means: securities denominated in a foreign currency get the “Euro” prefix, period.

In other words, what’s called a Euro bond is basically just an international bond.

- Yankee Bond = bond denominated in dollars

- Samurai Bond = bond denominated in yen

- UK?? Bulldog Bond.

- Korea? Apparently Arirang Bond. heh.

There’s a name for everything lol lol

5. Municipal bonds (munis)

These are bonds issued by state and local governments.

The huge thing about munis: interest income is not subject to federal tax!!!!

And — within the state that issued the bond — interest income is also exempt from state and local taxes!!! (Just interest income though. Capital gains and so on still get taxed.)

Two flavors:

- General obligation bonds — issued on the general credit of the local government.

- Revenue bonds — issued to fund a specific project.

Now, when comparing munis to other bonds, the tax-exempt thing matters a lot — you have to fold the tax rate into your comparison.

So you ask: “what if munis were taxed like everything else~~” and compute a hypothetical after-tax yield, then compare against everybody else’s yield.

It’s a formula a middle schooler can handle, so don’t sweat it.

6. Corporate bonds

The big word here: risk.

Everything above has basically zero default risk. Why??? Because Uncle Sam has its back.

But a company? There’s no automatic reason for the government to bail it out. Unless we’re talking GFC-level meltdown.

So you’ve got to actually think about default risk — the risk that the issuer goes bankrupt and stops paying interest. heh heh heh.

Chapter 10 has the full story, but here’s a quick taxonomy:

- Secured bond — has specific collateral backing payment if the company goes under.

- Unsecured bond (debenture) — no collateral. (Cheaper to compensate, naturally.)

- Subordinated debenture — lower priority on the company’s assets in bankruptcy.

- Callable bonds — bond with an option attached; the issuer has the right to buy it back from you at a pre-set call price.

- Convertible bonds — gives the holder the right to convert into a fixed number of shares.

Equity securities

1. Common stock (equities, equity)

Represents ownership in the company. One share = one vote on agenda items at the shareholders’ meeting.

Also gets you a proportional claim on the company’s financial profits.

This is exactly where the agency problem can show up.

→ Some patches for it: design the right compensation structure, get external monitoring, threat of proxy fights, threat of acquisition, etc.

Cf. Companies whose shares aren’t publicly traded → closely-held corporations. Most of them are run directly by their owners, apparently.

Two big features of common stock:

- Residual claim

- Limited liability

Residual claim = you’re at the bottom of the priority list when claiming the company’s assets and profits.

So if the company tanks, you first pay off bondholders, then preferred stockholders, then everybody else with higher priority, and only if there’s anything left over does the common shareholder get a piece. If there’s nothing left??? Womp womp, bye.

Limited liability = if the company goes under, the max you can lose is what you originally put in.

Compare with a sole proprietorship (unlimited liability) where they can come after your car and your house. With common stock, they can’t. Your shares go to zero — that’s the extent of it. No further liability.

2. Preferred stock

Has the genes of both stocks AND bonds.

The bond-like side: it pays a fixed “interest.” That makes it look a lot like a perpetuity (a bond with no maturity).

Also: preferred stockholders don’t get voting rights → also bond-flavored.

But there’s stock DNA too — dividends. Dividends.

And preferred stockholders get paid their dividend before common stockholders.

3. American Depository Receipt (ADR)

A certificate representing ownership of shares in a foreign company. Trades in the U.S.

The “ownership of shares” framing is kind of interesting on its own.

This is the most common way American investors get exposure to foreign-company shares, basically.

Heads up — ADS stands for American Depository Shares, and it’s used interchangeably with ADR.

I should also organize the derivatives market, but… nah, too lazy.

Why? Because I drilled this section into my skull when I was studying for the Derivatives Investment Advisor cert in the military, watching online lectures on loop…

So I’ll just upload my ridiculously well-organized handwritten Derivatives Investment Advisor notes from back then. lol

Of course, I’ll go deeper in the “The Derivatives I Studied” series too! >_<

Right here! >_<

http://gdpresent.blog.me/220834858303

Originally written in Korean on my Naver blog (2016-03). Translated to English for gdpark.blog.