Buying on Margin and Short Sales

A casual breakdown of how buying on margin works — borrowing from your broker to buy stocks, why margin calls happen, and why losses hurt way more than gains feel good.

When you want to buy stocks, do you have to pay for the whole thing out of your own pocket?

No no no no — there’s a thing where the brokerage actually lends you money to buy stocks.

It’s called buying on margin.

Basically, the investor borrows part of the purchase price from the brokerage. “Part of” — meaning they’re not handing you the whole amount, all-in. You have to put down at least a required minimum (called the margin / credit deposit) into your brokerage account, and then the brokerage covers the rest.

How does the brokerage get that money? They borrow it from banks and other financial institutions at the call rate, slap a fee on top, and re-lend it to customers. And the stocks you bought on credit? They sit in the brokerage’s name as collateral for the loan.

The FRB caps how much stock you can buy on margin — somewhere around 50%. Meaning at least 50% of the purchase price has to be your own money, and the brokerage can lend you the other 50%.

OK so let’s say you bought the stock. If the price keeps climbing, you pay off the interest you racked up on the borrowed money, and whatever’s left over is yours. Sweet.

The problem is when the price falls. Because the loss comes out of your share of the purchase, suddenly the margin percentage doesn’t hold up anymore.

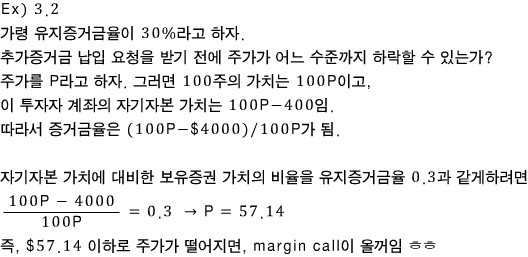

So how do we actually compute this? First — how is the margin percentage even defined?

Like that.

So a $10,000 stock gets clobbered down to $7,000 — let’s look at this. The key question: that $3,000 drop, whose share is it? Right — it’s unconditionally mine. The brokerage didn’t do anything wrong; the idea that they should eat part of the loss with you is kinda nuts, right???

Anyway. Say you initially bought the $10,000 stock with $6,000 of your own money plus $4,000 borrowed from the brokerage.

Then the stock drops $3,000 — what happens to my margin percentage?

This is exactly why we need a thing called the maintenance margin. The broker sets it.

And if you fall below the maintenance margin, the broker calls you up and says, “hey, deposit more cash or securities into your margin account.” This is called a margin call!!! (There’s a movie called Margin Call. I should rewatch it.)

OK so buying on margin is, simply put, just investing with borrowed money, right? But the important point — and I really mean important — is this: the loss when prices fall is way bigger than the gain when prices rise. Why? Simple: when you make a profit, you owe interest, so a chunk of your profit gets shaved off into the (-) column. When you take a loss, it’s the loss plus the interest piled on top. Naturally… heh haha.

Let’s just look at it with formulas. The profit when a $10,000 stock rises 30%, vs. the loss when a $10,000 stock drops 30%. (Let’s say the interest is around 9%.)

When the stock rises:

When the stock falls:

The upside was 21%, so you might think the downside would be a clean -21%. Nope. Not even close. But yeah, obvious in hindsight.

Next up: short sales. Short sales.

Short sales — in one word? A dirty trick.

Short selling is selling a stock you “don’t have”…

How do you sell a stock you don’t have?!?!?! Yeah… you don’t have it… it’s not like you’re selling clouds or something, that’s weird… OK actually you’re not literally selling a stock you don’t have — you borrow the stock and sell it.

Again again again. The investor borrows shares from the brokerage and sells them.

And then the investor has to give back the borrowed shares, right??? Obviously you have to buy the exaaaact same ones and return them. So the investor goes back into the market, buys the same stock, and hands it back to the brokerage. This is called clearing the short position.

Normally when we hold stocks, we profit when the price goes up, right? With short selling, you profit when the price goes down.

Yeah yeah, of course, right?!?!!! So — you take a goooood look at some stock and decide it’s about to crash? Cool, go ahead and short it.

But remember earlier when we were going through order types, and I was talking about the stop buy order — I said that when you’re short selling, you place a stop buy order to cap your losses, right…!!??

OK OK, what does that mean?

You thought the price would fall so you borrowed shares and sold them. But the price could just as easily rise. So the investor places a stop buy order as a safety net.

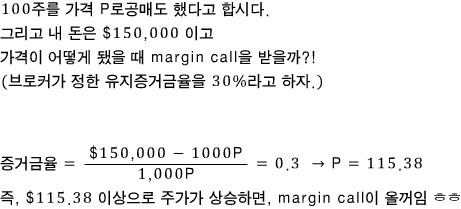

Since the investor has to eventually buy the stock back in the market and return it to the brokerage, they’re on the hook for however much the price climbs. So let’s say you borrowed the stock and sold it at $100 (presumably because you thought it'd fall to $80).

Just in case, you put a stop buy order at $110 as your insurance policy. If the price actually creeps up to $110, the order fires, you buy it back, return it… (boom — your loss is capped at $10.)

OK OK, one more thing. With buying on margin, what you owed the brokerage was money you borrowed. With short selling, the stock you borrowed is the debt.

So the margin calculation looks like this:

OK OK, got it. Moving on.

Originally written in Korean on my Naver blog (2016-04). Translated to English for gdpark.blog.