Bond Valuation and Risk

We actually price a bond this time — figuring out what it's worth today by adding up the present value of all those future coupon payments.

Last time we just kinda glanced at bonds — like, “oh look, these things exist~~~” — that level. Surface stuff.

Now we’re actually going to grab one specific bond and put a price on it. A bond with some coupon rate, and we figure out what it’s worth.

Pricing it isn’t actually that hard. The whole thing rides on one idea: the present value of the cash flows the bond throws off.

OK let me back up.

Say you have $A sitting around. You park it in the bank and just leave it alone. It grows. By how much? It grows by $rA$. So one year later you’ve got:

$$\left( 1+r \right) A$$in your hands. Cool.

The reason I’m bringing this up — what I actually want to know is the flip side. Money I’ll get in the future — what’s it worth right now?!?!

So suppose someone promises to pay me $B sometime in the future. The present value of that promise — we don’t know it yet, so let’s just call it

$$x$$And then we ask: how much $x$ do we need such that, if we leave it in the bank, it grows into $B$ one year from now? That’s the logic.

If you have $x$, then $rx$ gets added on, and it should equal $B$.

So getting $B$ a year from now is the same as having

right now. That’s all this is saying.

What if it’s $B$ in two years instead?

Let’s see.

Same principle, just stacked.

OK so now the situation is — I went out and bought a bond.

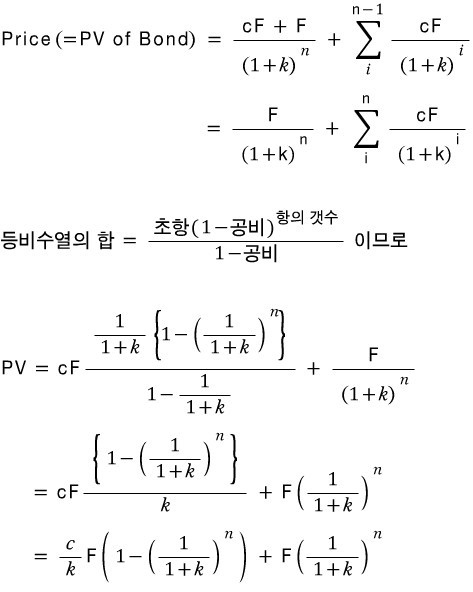

If you hold a bond, you get $c\%$ of its Par value (call it $F$) every year. So you get $cF$ after 1 year, $cF$ again after 2 years, $cF$ after $(n-1)$ years… and then at year $n$ (maturity) you get $cF$ plus $F$ itself back.

Now if we add up all those red things — that sum is the present value of holding the bond. What that bond is worth to you, right now.

Call it the Present Value of the Bond. And this would be the price of the bond.

Written out as a formula, it looks like that.

Oh — quick note. Why did I write $k$ instead of $r$ up there? $k$ is the required rate of return — the interest rate the investor wants.

The investor doesn’t want to just dump money in a bank and pull $r$ out of it. They went looking for something else. Right now, that something else is bonds. So instead of $r$, we use $k$.

Alright, an example, an example.

Bond with a Par value of $1000. The issuer says they'll pay $100 coupons each year. Three years left on it. And the annualized yield going around in the bond market right now is 12%.

Let’s see what the present value of this bond comes out to.

So it’s saying: it’s rational to buy a bond with a face value of $1000 for $951.97.

So yeah — bonds can sell below their face value, and how much below is called the discount rate.

We could write it like this.

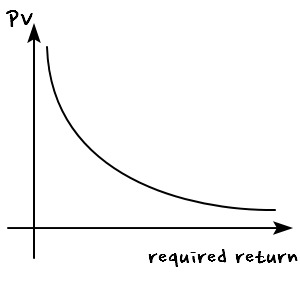

OK so this time — let’s see how the coupon rate affects the bond price, and how the required return affects the bond price.

Sounds fancy when you say it like that, but it’s not.

Roughly: a higher coupon rate means the periodic payments are bigger, so PV is higher. Make sense?

A higher required return means the investor demands more interest income, so PV is lower!!!

Bonds that sell below their face value in the market are called discount bonds, and the more the investor’s required return exceeds the coupon rate, the deeper that discount goes.

What does that mean? Let’s write it out using the PV formula.

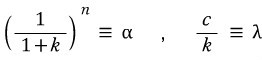

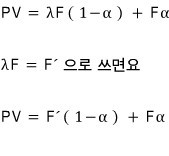

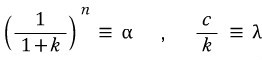

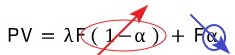

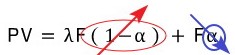

I cleaned it all up. Let me rename the symbols a bit so the meaning pops out more easily.

OK now let me actually read this.

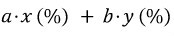

Look at this formula for a sec.

“Ahhh — so what we’re adding is $x$ amount of effect $a$, plus $y$ amount of effect $b$~~”

You can read it that way, right? The formula above is doing exactly that.

Present Value, sliced into 100 parts: $\alpha$ portion of it comes from $F$, and the remaining $(1-\alpha)$ portion comes from $F'$. That’s what’s going on!!!

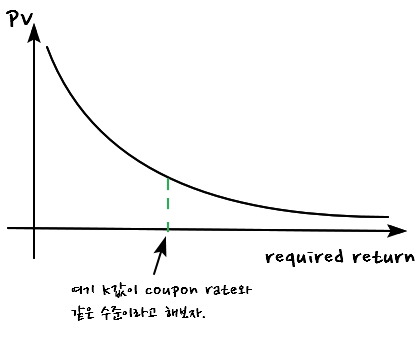

i) If $c=k$, then $\lambda=1$, so $F = F'$. So PV is:

$$PV = F(1-\alpha)+F\alpha = F$$PV just equals the face value $F$. That’s it.

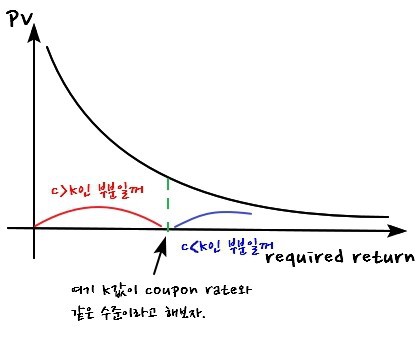

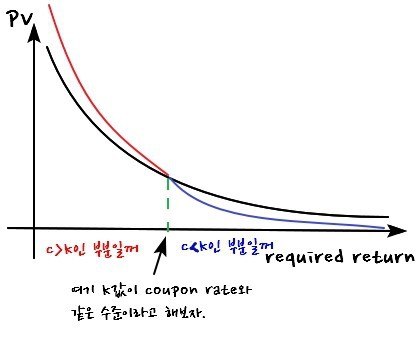

ii) If $c > k$, then PV is a weighted sum of $F'\,(>F)$ and $F$, so the sum is unconditionally larger than $F$.

Meaning $PV > F$ — the bond’s price sits above its face value. Bond like that is called a premium bond.

iii) If $c < k$, same logic in reverse, $PV < F$. The bond’s price is below its face value — that’s a discount bond. >_<

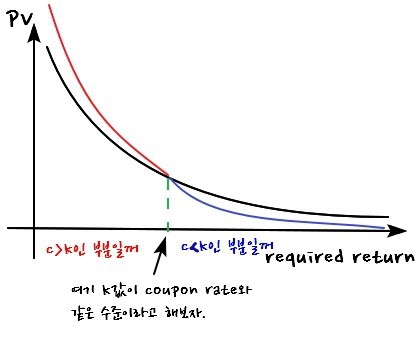

Now we can graph PV against $k$!!!!

It’d come out looking like that!?!?!

OK and if we plug in the stuff we just figured out —

First, written like this,

We can say it like this?!?!?!~~~~

OK OK OK OK OK but — what happens as the maturity gets longer and longer?!?!?! What does that do to the graph?!?!

First, as $n$ gets larger —

$\alpha$ gets larger.

Then —

in this formula,

we get this, right?!?! As maturity stretches out, the share coming from $\lambda F$ grows, and the share from $F$ shrinks.

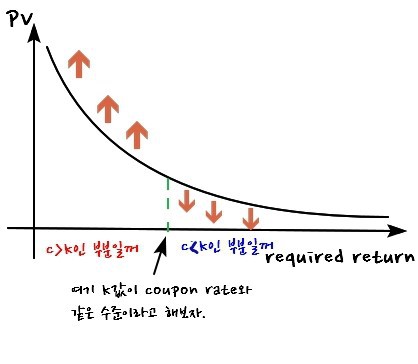

So what happens to overall PV? “Sometimes it gets smaller, sometimes it gets bigger.” Depends.

- When coupon rate $=$ required return: doesn’t matter what maturity does, PV stays put.

- When coupon rate $>$ required return: as the $\lambda F$ share grows, PV gets bigger.

- When coupon rate $<$ required return: as the $\lambda F$ share grows, PV gets smaller.

That’s the breakdown.

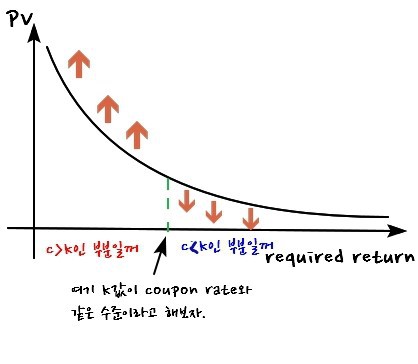

So on the graph, as maturity climbs —

the change looks like the curve is rotating around one fixed point as an axis!!!~~~

That might be confusing drawn that way, so let me redraw it like this.

Originally written in Korean on my Naver blog (2016-05). Translated to English for gdpark.blog.