Inventories (1): Acquisition Cost

We kick off our B/S line-item series with inventories — what they are, how acquisition cost first hits the books, and the cash-vs-credit purchase breakdown.

OK so by now we kinda know what B/S, I/S, and C/F are,

and we kinda know how revenue and expenses get recognized — that’s where we’re at.

Nice!

So now let’s start studying the individual line items on the B/S, one by one.

This isn’t a CPA exam — if I had to map it onto something familiar, it’s closer to a “Financial Analyst” type exam,

so honestly the most important question is, “what effect does a financial item have?” — that’s the focus!!!

Alright then, let’s go!!!

Inventories

First up: inventories.

Before we dive in, when you study any line item, there are 3 key things to keep in mind.

When a line item first hits the B/S, how do we record it?

After we record it, do we just leave it sitting there quietly~~~, or do we have to mess with it as the years tick by? — that’s subsequent recognition.

And eventually we’ll need to take it off the B/S too, so when we yank it off, what’s the accounting treatment?

Think of every line item as following this kind of three-step study process.

OK then — “what is inventory?”

The definition of inventory is:

“products that have finished production and are being held for sale, & work-in-progress that hasn’t been finished yet, & raw materials bought for production, etc.”

That’s how it’s defined :-)

First, since some of you might be total beginners, let’s take a really wide look at how inventory shows up and disappears.

There are tons and tons of paths inventory can take through a company, but two of them are the headliners.

Heads up…

What you make in-house is called “finished goods (제품),” and what you buy from somewhere else and stack up to flip is called “merchandise (상품).”

A distribution company would buy merchandise from somebody else and resell it at a markup, right? Here’s roughly how inventory shows up and goes away in that case.

When the distribution company buys merchandise from a manufacturer, inventory goes up,

and since they’re going to sell that inventory to consumers, once it’s sold, inventory disappears.

And for both the buying and the selling,

there are two scenarios: pay cash on the spot, or buy/sell on credit.

OK now let’s really get into the spirit — the SPIRIT! — of the revenue-expense matching we were screaming about earlier.

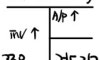

First, the cash purchase case.

Since it’s literally just hand over cash, poof inventory appears, the change on the B/S is:

Cash vanishes with a poof, and inventory slides smoothly in.

(Note: when I show increases/decreases or the effect of increases/decreases on the financial statements, I’ll use ↑ and ↓ symbols!!)

But — say we bought it on credit instead.

Then for now, we get the inventory without handing over any cash.

Instead we’d write something like a promissory note saying we’ll pay for that inventory within X days.

In accounting, this kind of liability is called Account Payable (A/P),

and since this is a “current obligation” for our company, it’s a debt (liability),

so for now, as Inventory shows up, A/P pops up on the liabilities side.

Then once we actually pay it off,

we hand over the cash and “we have fulfilled all our obligations~” — meaning, since there’s no remaining obligation, A/P also gets wiped off the liabilities side.

In the end,

whether we pay cash or use credit, on the B/S

the result on the B/S looks the same!

OK OK OK,

and since no revenue has happened yet, there are no expenses either,

and we haven’t touched the expense side at all yet.

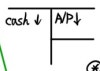

Now let’s say this inventory got sold!

We’ll look at the cash sale case too.

Companies aren’t charities, so they’re going to take a margin!

They’d resell it — buy something for 80, sell it for 100, like that!!!!!!!

(Revenue is 100, expense is 80, right?!)

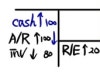

So 100 in Cash comes in, and the 80 portion of the inventory we were holding goes out,

so 20 is left over on the Asset side, and that 20 has to go somewhere on the credit side — but where?????????

It gets recorded right there in Retained Earnings (R/E).

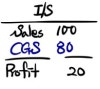

And the thing that explains this profit in more detail was the I/S, right???????

Let’s hop over to the I/S for a second. On the I/S, how does that profit of 20 get handled? Well,

the Inventory goes to CGS (CoGS; Cost of Goods Sold).

Basically, this is an expense.

It’s the amount sacrificed to generate revenue of 100,

and to generate revenue of 100, we sacrificed the Inventory we’d spent 80 to buy,

so this is how revenue and expenses get matched.

A credit sale gives you the same result.

What’s that A/R sitting in the middle?

It’s the receivable that says “hey, you owe me money” after a sale on credit.

So after we hand over only the inventory, we have to keep in hand a document saying they owe us — that’s a receivable,

and in accounting it’s called A/R (Account Receivable).

And once they pay us, we wipe that asset off and Cash bumps back up!

And then once the inventory is sold, that leftover 20 still flows through R/E the same way,

and honestly this is the amount that trickles down through Sales and CGS on the I/S!!!!!!!

So what we just saw is:

the inventory we bought to sell sits piled up on the B/S as Inventory,

the chunk that generates revenue disappears, and that part flows over to CGS on the I/S,

and the leftover profit shows up as R/E in the Equity portion of the B/S!!!!!

That’s the big-picture view of the whole thing!

But of course it’s not like every single transaction triggers a B/S update.

I mean, what company does inventory transactions just once!?!?!

So we take a period — quarterly, annually, whatever — and aggregate all those transactions together,

and the B/S and I/S get prepared.

Same idea though.

On the B/S, you’ve got the Inventory amount that was already piled up at the start,

- whatever extra got purchased during that period,

and then at period-end, you look at the Inventory that’s left,

oh???? there’s a bit of a difference??????

Why’s there a difference? There’s a difference because that gap got sold,

and where did we just say the gap goes?!?!?!?? Yes yes, CGS!

So we can write this formula.

I just explained it in words above,

but seriously this is a formula you do NOT need to memorize lol lol it’s that obvious

Right?! Right?!?!!? Makes sense, doesn’t it?!?!?!?

Then this diagram should click too.

Consider this the “big picture of how inventory flows” view.

OK, now let’s zoom in on “initial recognition” a bit more.

Above, we just briefly looked at a distribution company that buys inventory it’ll resell at a markup,

stacks it up, sells it, pockets the leftover profit~

That kind of thing, just briefly.

Now let’s say it’s a manufacturing company. Hmm, what should I pick? Let’s say a semiconductor company.

We’re running a company that makes semiconductors, and to make those semiconductors, we need gold.

So we’re going to buy this gold from another country,

and just to ship one of these in, we have to pay airfare, and we have to take out insurance for the shipment and pay the premiums,

and we have to pay customs duties when it lands in our country… a huge number of other costs (incidental costs) get piled on.

The gold itself costs 100, but those incidental costs were 50….

So how much do we say we paid for it?????

Record it as 100, since the price was 100?

Or,

write 150, because the actual cost of getting that gold here was 150?

The answer is:

“For any Asset, the amount you put into the cost of that asset has to include all reasonable incidental costs up to the point where the intended purpose of acquiring that asset is exactly READY.”

Why?!?!?!?!?

No, why!!!!!!!!lol lol lol lol lol lol lol lol lol lol lol lol

Annoyingly, why!!!!!!lol lol lol lol lol lol lol lol lol lol lol

lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol

The reason is, this is exactly how the Matching Principle gets satisfied….

For something to go out as an expense, it has to go out timed to when revenue is confirmed,

but when you’re buying inventory, there’s no revenue yet to match against….

So the concept is: bury all of it as an Asset, and then when revenue gets recognized, it goes out as an expense together with the revenue.

Now let me throw one diagram at you and explain everything off of it.

Please ignore the blue text for now!

I want to wipe all of that off and re-upload the photo, but if I start image-editing on top of it, this post will take forever to write…. I’ll just push through using the original as-is as much as possible, sorry T_T T_T T_T please bear with me T_T T_T

What we’re holding to sell is Inventory,

and all reasonable incidental costs up to the point where the “for sale” purpose of that Inventory is exactly Ready have to be baked in.

First you’ve got the raw material price,

then yeah, the airfare to ship it in, the insurance, taxes… and so on,

and just leaving raw materials sitting there isn’t going to magically turn them into semiconductors, right?

We’ve also got to pay wages to the workers in the factory. Because only then do those people thump-thwack! turn raw materials into semiconductors!!!!

This way, the semiconductor is finally made, and everything is Ready for the purpose of selling.

It’s exactly up to here that gets recorded as inventory.

(If it gets sold later, where did we say it goes??? Yes yes yes yes, CGS~)

And then any costs after it becomes Ready for Sale — those do NOT flow through inventory. That’s the point.

Whoa………. this is so interesting lol lol lol lol lol lol lol lol

But — there’s something that kinda got exposed because I couldn’t edit that diagram,

and the reason the word “reasonable” keeps tagging along whenever they say “reasonable incidental costs” is….

there must be exceptions, which is exactly why they keep slapping that word on lol lol lol lol lol lol

There are exceptions, and

these exceptions seem like they only really matter for exam purposes.

But you kinda get it intuitively, right???? Burning a fine into Inventory would be way too funny lol lol lol lol

As for stuff like a rebate, in our cultural sensibility it has a kind of negative ring to it,

but actually rebates are super common in business (no wait… there’s nothing wrong with throwing in a little extra for a client who buys a ton from you, right?)

and this gets accounted for as just a price reduction.

But there’s one thing that’s really weird lol lol lol lol lol lol

No like lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol

In the red-text diagram, the fact that it didn’t just say “Freight” but said “freight-in” was a little weird lol lol lol lol lol lol

Yeah. lol lol lol lol lol lol Freight-out does NOT go through Inventory.

But when you actually think about it, it makes sense.

When you’re bringing it in, there’s no revenue to match yet, so we must not expense it yet,

Freight-out means it’s being sold and shipped out,

which means there IS revenue to match against, so that doesn’t flow through Inventory — it goes straight through expenses!

So up to here, we’ve looked at how Inventory gets onto the B/S in the first place,

i.e., how it’s “recognized.”

So next,

let’s look at “subsequent recognition” after the initial recognition!!!!

(Phew… barely hit this week’s goal T_T T_T this is rough… my week…)

Originally written in Korean on my Naver blog (2021-04). Translated to English for gdpark.blog.