Property, Plant and Equipment (3): Revaluation Model

IFRS lets you pick the Revaluation Model for PPE — and here's why that's a big deal (and a headache) compared to just sticking with the Cost Model.

OK so here’s where we’ve landed so far.

When a company first buys some PPE (Property, Plant and Equipment) and wants to put it on the B/S — the question is, at what amount?

We figured out how to nail down that acquisition cost.

And then we looked at how, instead of just dropping its value bit by bit over time as some kind of “revaluation” thing, we follow the Matching Principle and allocate the cost over time — that’s Depreciation.

Handling subsequent measurement only like that is called the Cost Model.

And under US-GAAP, for PPE, the cost model is your only option. That’s it. Done.

But IFRS? IFRS gives you another choice on top of the Cost Model — you can also pick the Revaluation Model for subsequent recognition.

Which means everything I’m about to say about Revaluation only applies under IFRS. If you’re in US-GAAP land, this whole post is content you don’t even need to think about!!!!!!!!!!

(This kind of split is genuinely annoying to study….)

OK so what does the Revaluation Model actually do?

Conceptually it’s a little similar to the LCM (Lower of Cost or Market) method we use for Inventories.

Inventories also start at acquisition cost on the B/S — let’s say you booked them at 10,000 won. But the whole point of holding inventory is For Sale, and when you actually try to sell them, the market is offering you… 5,000 won. Take it or leave it!!!

In that situation, is it really reasonable to keep them sitting on the B/S at 10,000 won…? So under LCM, if a write-down is needed, you write it down — and you book an inventory valuation loss/gain!!!!!!!!

But PPE is a different beast — its purpose is For USE, not For Sale.

Picture some ancient state-owned enterprise. They bought some land in Seoul forever ago for 60 million won. It’s still sitting on the B/S at 60 million won. You go check the market price… and it’s 100 billion won. Apparently cases like that have actually happened.

But… it’s awkward, right……….?

Should land that’s on the B/S at 60 million suddenly get bumped to 100 billion????

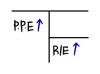

Let’s say you do bump it to 100 billion on the B/S.

That gain flows up and now Retained Earnings goes up. And R/E is the pool shareholders can pull dividends from. But this gain from the real estate revaluation is an unrealized gain/loss????

So R/E is fatter, shareholders see the number and start asking for dividends… but this isn’t actually money you can pay out T_T T_T T_T T_T

To actually realize that gain so you can pay the dividend… you’d have to sell the land. And then this PPE — which is For USE — can’t be used anymore. The whole business that was running on it shuts down too.

But hold on, even so —

leaving something worth 100,000,000,000 won

booked at 60,000,000 won also feels deeply wrong, doesn’t it?!?!?

“I PROMISE I won’t ask for dividends, just please show the real number!??!?!?!”

— said someone. And his name was IFRS.

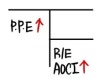

Agreed — the gain from revaluation is an unrealized gain/loss!

So we built AOCI (Accumulated Other Comprehensive Income) to park that kind of stuff, and we’ll just route it through there!

The bucket shareholders pull dividends from is still R/E, so don’t worry about that!

BUT — even if it’s unrealized, losses still have to flow through Net Income and land in R/E. And much later, when the gain actually gets realized, then it has to flow through Net Income into R/E!!!!!

(In other words, Revaluation Surplus eventually becomes Retained Earnings, and this kind of move is called a transfer.

Now — for how you transfer Revaluation Surplus into Retained Earnings, there’s the “do it all at once when the asset gets disposed of” method, and there’s also the “drip it over a little at a time during the holding period” method. But that’s outside CFA scope, so I’m just brushing past it ^^)

AOCI is the broad/umbrella account, and the specific sub-account that gets credited from this revaluation is Revaluation Surplus.

And one more time, just so it sticks —

Revaluation, where you re-mark PPE at Fair Value, is IFRS only! US-GAAP doesn’t allow it!!!!!!!!!!

And to make sure companies don’t just go wild with the Revaluation model however they please, there are some rules around it.

Yep, allowed ~

In practice, apparently a lot of companies only use the revaluation model for land. Because the AOCI that piles up from the revaluation makes the Equity side bigger, which makes financial ratios look really healthy. (Debt to Equity)

And land doesn’t get depreciated to begin with — but for other PPE, if you revalue up, that means the depreciation expense going out also goes up, right?

So the move is: only revalue land.

Basically, this revaluation model can be a tool to dress up a company’s creditworthiness.

But every once in a while, you’ll see companies apply the revaluation model to depreciable assets too, even with the depreciation going up.

When you see that, you should be able to go: “Oh…. y’all are that desperate….?…."

(Doo-X did this, and apparently among older KOSDAQ listings, about 50 or so pulled this move — and out of those, all but 2 have since been delisted.)

Shut up

You can’t cherry-pick an individual asset

No!

The standards don’t pin down a fixed interval — it’s fine to only do it when market prices have shifted meaningfully

(In practice, apparently usually once every 3–5 years.)

Ok, here’s a scenario.

100 → 120 → 90 → 110

* Impact on the financial statements when you do a Revaluation

- First, Total Assets & Equity go up (yes, even if it’s just AOCI, it still goes up)

- So Debt to Equity goes down (= D/E)

- Depreciation is now calculated on that new, higher price, so depreciation goes up. → ROA, ROE go down.

: In exam land, they’re not going to tell you “only land was revalued” the way it actually works in practice… so point 3 wouldn’t apply in cases where only land gets revalued…

One more time for emphasis — the Revaluation model is IFRS only!!!!!

Was it 2011 when Korea actually adopted IFRS?

But I feel like it was a little while after that when I first heard about the profession called property appraiser…

I don’t know the details well, but property appraisers must’ve gotten a ton more work after IFRS adoption, right? Which means their market value also went up?!?!

Because if you DON’T revalue your land you’re leaving money on the table, and if you DO, you have to periodically get a Fair Value assessment from a property appraiser?!?!?

You really never know how things are gonna shake out for any given career hahahahahahahahaha

Similar story — apparently the department the top science students in 12th grade used to flock to was Physics heh heh heh heh (whew, born in the right era… given how much I liked physics… I might not have even made it into the Physics department haha)

What else… when I was applying to college, the most prestigious department at the time was… electrical engineering(?)… but hasn’t all that prestige migrated over to industrial engineering or CS by now?

What’s gonna be the department holding that crown next…..heh

This one’s for the thumbnail (it’s cute so haha)

Originally written in Korean on my Naver blog (2021-05). Translated to English for gdpark.blog.