Income Tax Expense

Breaking down how corporate tax expense actually works — from taxable income reconciliation to current vs. deferred tax — purely from the CFA angle, heh.

Hmm… I haven’t actually gotten to the corporate tax chapter in intermediate accounting yet…… heh

So I won’t be able to add commentary on how it’s taught for the CPA in this post… heh

I’ll write this purely from the CFA angle! hehehe Here we go!

Everyone pays taxes, right??? Yeah yeah, you’re all paying taxes. You’re paying indirect taxes like the 10% VAT,

and if you have a job or a part-time gig, you’re paying “income tax” too.

A corporation is a person too, you know? It’s a legal entity that the law recognizes as existing,

and if it’s a joint-stock company, the whole point of its creation is to make money — so it should have to pay income tax too, right?

Exactly. That’s corporate tax. To spell it out a little more, it’s basically corporate income tax.

So now we’re going to look at how corporate tax actually gets recorded.

The money the company earned during the period gets written on the I/S,

so… is the amount we record as corporate tax expense just calculated by slapping the period’s tax rate on it?

Nope, that’s not how it works…….

The taxing authority recalculates the profit this company earned by its own standards.

This process is called tax reconciliation.

The starting point seems to be that the profit as the company sees it (Pretax Financial Income)

and the profit as the taxing authority sees it (Taxable Income) are different from each other.

Why on earth would they be different!?!?

They have to be different…..

Because companies use accrual-basis accounting….

Ex1. From the company’s perspective, Unearned Revenue (advance payments received) is money you got but you haven’t actually delivered the service yet, so it hasn’t been recognized as revenue. But the taxing authority is like, “Hey, you guys got the money!!! Pay your taxes!!!!”

Ex2. If a company breaks the law and pays a Penalty (a fine), the company books it as an expense. But it would be hilarious if the taxing authority also recognized that as an expense lol — because then the fine would have a tax-saving effect…

Anyway, since the perspectives on what counts as income are different like this,

the corporation’s revenues and expenses go through reconciliation.

So once this reconciliation is done properly, are we finished calculating the corporate tax this company has to pay?!?!?!?!?!

Yeah yeah — what we just calculated is the tax actually being paid this time around!!!

So is that what gets recorded as Tax Expense on the company’s I/S?!!??!

T_T T_T T_T sob sob, unfortunately…. there’s one more thing….

What we calculated above was only Current Tax Expense. There’s another piece —

something called Deferred Tax Expense.

It’s only when these two get combined that the Tax Expense showing up on the current period’s I/S is actually formed.

The idea is that on a corporation’s financial statements, on top of the money actually paid, additional info gets layered on top to give a more useful picture.

To understand what this deferred tax thing is,

you now need to learn the concept of Temporary / Permanent Difference.

Let’s start the discussion right here!

Temporary Difference: a difference that arises from a timing gap in taxation.

(Apparently in practice, Permanent Difference situations are way more common than Temporary Difference. That’s what I’m told.)

OK let’s first look at the situations where Temporary Difference shows up, and learn the concept that way.

Like the very first example up top — money received in advance has come into the taxing authority’s crosshairs, but it’s an amount the company hasn’t recognized as income yet.

So in year x2, when the income actually gets recognized, the tax on it was already paid back in year x1, so it gets offset during reconciliation.

For depreciation: the company will expense things using whatever depreciation method it picks.

The taxing authority does not recognize the depreciation method the company picked, and instead uses the taxing authority’s own depreciation method.

This is called MACRS (Modified Accelerated Cost Recovery System) — for CFA purposes this isn’t particularly important,

but anyway, the company’s depreciation gets modified and then applied. So there’ll be taxes paid early, and taxes paid later — that’s the deal!

Warranty, Bad Debt Expense, “loss allowances” — they’re all similar concepts, so let me say it all in one go:

For example, suppose you’ve invested in another company’s bonds and you’re collecting the stated interest on each interest payment date, and that company suddenly starts looking shaky —

there’s an accounting treatment on the company’s financial statements where this gets expensed in advance.

Warranty isn’t corporate bonds, but it’s also an accounting treatment that pre-records expenses you expect to happen down the road.

Because the taxing authority doesn’t recognize expenses like this that haven’t actually happened yet,

Temporary Difference can pop up.

Same deal for investments in other companies’ shares.

Under IFRS, if you’ve invested in another company’s shares (investment securities), they typically get classified and managed as FVPL or FVOCI,

and at each period-end they get remeasured at fair value, with unrealized gains and losses (that you haven’t actually realized yet) getting recognized either as P&L for the period or as other comprehensive income — and since it’d be plain wrong to say “ohhh you have income~ pay your tax~” on unrealized gains and losses,

Temporary Difference shows up like this.

Same thing for retirement benefits.

It’s money that only goes out the door when an employee actually leaves, but on the company’s financial statements there’s an accounting treatment where you expense it bit by bit as the years go by,

while for tax purposes, the expense is only recognized when that employee actually quits and the cost is really incurred,

so Temporary Difference shows up here too!

It also shows up in R&D.

Anyway, you’re starting to get a feel for Temporary Difference now, right?!!?!

Notice how, in the examples above, certain revenues or expenses are set up such that “there will necessarily be an opposite effect in the future,” right?!

And if the future is determined like that, shouldn’t that future effect be reflected in the books?~~~

That right there is the starting point of the Deferred Tax concept.

Since 100 was recognized as income in advance for tax-calculation purposes, that much would’ve been tacked on when computing corporate tax.

And since the tax on that 100 was already paid, when that revenue of 100 actually shows up on the I/S later, it conversely

needs to be backed out during tax calculation,

so to express “we have tax we’ll pay less of later~” — using an account called DTA (Deferred Tax Asset),

there are cases where the accounting treatment recognizes it as an asset.

And the other way around,

If more expense was deducted in the tax calculation, that means less revenue was effectively recorded, so less tax was paid in year x1. But

since a future where less expense gets deducted is guaranteed to come,

on the company’s financial statements, to express “we have tax we’ll pay more of later~”,

using an account called DTL (Deferred Tax Liability),

the accounting treatment recognizes it as a liability.

So to summarize:

The Tax Expense that shows up on the I/S is calculated like this.

OK OK OK OK OK OK OK OK OK OK OK OK OK OK.

You probably still don’t quite get it.

From here on out, I’ll start with easy examples and crank up the difficulty bit by bit.

You’ll see that this corporate tax part is actually nothing to be scared of, so don’t worry!

Let’s try calculating the amount that’ll get recognized as Tax Expense on the I/S for this kind of case!

Say that through tax reconciliation, a Temporary Difference of +2000 was created.

Meaning: because of the taxing authority’s revenue calculation, 2000 more was recognized as revenue, so when computing tax, 2,000 gets added on top of this company’s income of 10,000,

and Tax rate = 20% gets applied to that, giving 2,400 as Current Tax Expense. (That’s the amount actually paid to the taxing authority.)

But here, since that +2000 in revenue is guaranteed to result in -2000 less revenue in the future,

that amount represents “we have tax we’ll pay less~” — so the DTA account entry gets created,

and 2000 × 0.2 = 400 worth of DTA pops into existence.

So the Tax Expense going on the I/S will be displayed taking into account not just Current Tax Expense but also Deferred Tax Expense,

so 2400 minus 400 gives us 2000 as the final Tax Expense.

The calculation is just done through this formula.

And let’s say year x2 is the year where, in reconciliation, that pre-recognized revenue of 2000 finally gets backed out.

Same way here,

Running through the formula, Tax expense comes out to 2,000,

so the value falls out without any trouble.

Hey!?!!?!?!?!?

GD Park you jerk, you didn’t just sell me snake oil right now, did you?!?!?!?!?

If you just look at the result, Tax expense turned out to be nothing more than financial-statement income times the Tax rate!!!!!!!!!!!!!!!!

That’s what came out…..

This was just a case that happened to work out that way.

For that to happen, two conditions have to be met:

There’s only Temporary Difference

A Stationary Tax rate is maintained

If both are met, then yeah — you can just multiply income by the Tax rate.

So if a problem looks like this, you can quickly mark the answer and move on.

But in cases where even one of those conditions fails,

you have to use the orthodox method…..

And because you need to know the orthodox method,

that’s why I was rambling on this whole time :-0

OK OK OK OK OK OK so then,

a few details I glossed over earlier because I figured they’d just confuse you if I dropped them right at the start —

let me tell you just three more things.

The tax rate applied when calculating Current Tax Expense is the current stationary tax rate.

The tax rate applied when calculating Deferred Tax Expense is the future tax rate.

What that future tax rate gets multiplied against is not the Temporary difference generated in the current period,

but the cumulative temporary difference accumulated up to that point.

Let’s take another look at this part.

When calculating the tax to actually pay this time, of course the current tax rate gets applied,

so this part makes intuitive sense.

But why is it that when determining the DTA or DTL amount, the future tax rate gets applied?!?!?!?!?!

The “we have more / less tax to pay~” thing —

that more or less tax will get paid with the future tax rate applied,

so that’s why we have to express it using the future tax rate :-) Easy right, easy right.

And why is it that when determining the DTA / DTL amounts, it’s based on cumulative temporary difference?!

That’s precisely because DTA/DTL aren’t I/S accounts, they’re B/S accounts.

The B in B/S stands for Balance. Balance refers to the value of how much the company has cumulatively as of that point, right?!?!

So here, the calculation isn’t based on the Temporary diff generated in the current period,

it’s that the DTA or DTL amount is determined by looking at all the temporary diffs that have accumulated up to now.

Put it that way and you get it, right?!?!? haha

OK so anyway,

There’s only Temporary Difference

A Stationary Tax rate is maintained

If both conditions are met, you can just multiply income by the tax rate.

But if even one condition fails,

When using this orthodox method,

the three details I just mentioned —

The tax rate applied when calculating Current Tax Expense is the current stationary tax rate.

The tax rate applied when calculating Deferred Tax Expense is the future tax rate.

What that future tax rate gets multiplied against is not the Temporary difference generated in the current period, but the cumulative temporary difference accumulated up to that point.

— you have to be careful about these three details when calculating!!!!!

That’s how far I’ve explained.

So now let’s look at an example that actually requires the orthodox method.

(Let’s say Pretax Financial Income for both years is 1,000.)

Let’s calculate the tax expense for year x1, for two cases!!!!!

Let’s feel the power of the mighty orthodox method!!!!!!!!!!

So let’s calculate the Tax Expense that’ll show on the I/S for year x1.

First, a Temporary Difference of +200 was recorded (this is a value that will necessarily bring a -200 effect later on),

and a Permanent Difference of -100 was recorded — and this is a tax adjustment that will not bring a +100 effect later.

So, when calculating Current Tax Expense (the amount to pay this time),

we take our company’s Pretax F. Income of 1,000, add +200-100 to get 1,100, then slap the current tax rate of 40% on it to get 440,

and since the cumulative Temporary Difference for year x1 is +200, meaning we have less tax to pay later~ this needs to be expressed as DTA,

and the DTA value is 200, and since we’re assuming the future rate is also 40%,

applying 40% to that gives 80, which gets subtracted to get what should be recognized as Tax expense,

so it comes out like this.

This time, instead of 1,000 × 40% = 400,

we get 360, right?!?!?

There’s only Temporary Difference

A Stationary Tax rate is maintained

Because condition 1 wasn’t met, that’s why~ heh.

Anyway, the effective tax rate this time works out to 36%.

Because 1000 × 36% = 360,

the tax rate calculated this way is called the Effective Tax Rate.

To summarize: Temporary Difference creates absolutely no gap between the effective tax rate and the nominal tax rate.

It’s Permanent Difference that creates the gap between the two!

OK let’s look at the second example too. This is a situation where there’s only Temporary Diff, but the tax rate changes —

so it’s a case where condition 1 holds but condition 2 fails.

So what’ll Tax Expense come out to?!?!

The calculation is easy at this point so I’ll skip the explanation.

Now let’s think about it for a sec.

DTA is essentially “we have tax we’ll pay less of later~”, which, if you flip it, means “we already paid more!”

But if the tax rate goes up,

it means “we paid more at a lower tax rate!” — which is actually a total windfall,

Conversely, DTL is “we have more tax to pay later~”, meaning “we paid less than we should’ve.”

And if the tax rate goes up — “we paid less at a lower tax rate T_T T_T T_T noooo T_T T_T it can’t go up!!! Stop!!!!”

In other words:

if the tax rate goes up, companies sitting on a lot of DTA win / if the tax rate goes down, companies sitting on a lot of accumulated DTL win — that’s how we can think about it!

Easy, right?!?!?!? hehehe The calculation doesn’t seem so bad anymore.

So calculation is fine —

let me add just a bit more meat and wrap this post up.

Depending on whether the Temporary Difference is positive or negative, either DTA or DTL gets created,

and this can sometimes get confusing!

So the summarized version is

You look at the difference between the amount of Asset and the amount of Liability from the company’s financial-statement perspective vs. the taxing authority’s perspective,

and you decide “oh, this is a situation where DTA gets created!” or “this is a DTL situation!” — that’s the method they taught us.

(I’m not so sure about this method… it actually feels more confusing to me, so even in the exam room I was doing it like “wait, did they make more revenue get recorded? Then they paid more tax, so they need to pay less later, so this is a DTA situation” — that’s how I was doing it….. They say dumb people gotta work harder, right? T_T)

But for prepping for conceptual word problems, there are cases where you need to know when DTA gets created.

What I mean is: the case where Net Operating Loss gets carried forward —

in cases like that, DTA gets recognized.

What that means is….

I haven’t mentioned Allowance yet, right?!

That part — what it means is….

If there’s a situation where the DTA value needs to be marked down a bit, you can use the account called Allowance to subtract that amount and display it.

(US-GAAP displays it as gross / IFRS displays it as net.)

And conceptually, these values should be presented at Present Value — that’d be more conceptually correct.

(DTA/DTL values are not discounted to present value when determining the amounts…… This is content that was going to come up at the very end…. heh heh.)

Also, in situations where it doesn’t look like it’ll ever reverse at all, it doesn’t get recorded at all — conceptually you can view this as being recognized as Equity.

That’s roughly the gist.

And just one more thing T_T T_T T_T

I’m sorry haha this is ridiculously not ending lol lol lol lol lol lol lol lol

lol lol lol lol lol lol lol lol lol lol lol lol lol lol

In the end, the most important thing in this section for CFA purposes

is having to calculate Tax Expense.

And since this is a bit removed from common sense, it’s a little tough at first.

And the conceptual word-problem prep that comes after this seems even harder…………………

Oh well……………………………………..

Anyway, the Tax expense section got wrapped up nicely in one post!!!!!!!

Should I add one more thing? It’s just kind of an interesting story. hehehe

In stock investing, among the things people look at a lot, “net income” is probably one of them.

But the truth is, depending on a company’s accounting policies, net income can actually be massaged…..heh

So Ken Fisher, the value-investing master, said you should look at revenue, not net income!!!

But while studying this corporate-tax-expense section, this thought occurred to me:

“Wait — since the taxing authority’s rules are used to measure revenue and expenses and calculate the period’s corporate tax expense, couldn’t looking at the corporate-tax-expense side, rather than net income, be one tool for judging whether this company is truly generating good revenue or not?”

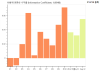

That thought hit me, so I tried running a decile analysis on this financial item.

First off, you can’t just go by whether the raw value of revenue or corporate tax expense is big or small — you’d have to normalize it somehow first.

You know how people commonly look at the ratio of net income to revenue, called net profit margin? I ran a decile test on that, and showing just a portion:

Right now this universe is the top 200 by market cap,

and you can pretty much say net profit margin doesn’t work at all.

But running the same process using corporate tax expense divided by revenue —

Oh.//..?? Pretty impressive, right?!?!

I’ll only reveal this much ^.^

Next time I’ll see you with Non-Current Assets!

Specifically the kind where bonds get presented at Amortized Cost!!!!!!!!!

It’s gonna be very interesting hehehe

See you next week~

Have a great week this week~

Originally written in Korean on my Naver blog (2021-06). Translated to English for gdpark.blog.