Bonds

Cruising through bonds for CFA prep — par, discount, and premium bonds, how market interest rates set the price, and how it all lands on the financial statements.

Alright, back to CFA exam prep mode,

and this time I’m easing into Non-Current Liabilities. heh

Last post, I went kinda~hard on the effective interest rate method from the side of the company that issues the bond,

so this one I want to cruise through a little more. hehehe

Is that why I was scribbling so frantically up front!?!? hehehe

First things first — bonds split by face value into

issued above face / below face / right at face,

which we call Premium Bond / Discount Bond / Par Bond, like we said before.

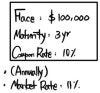

If a bond with face value 100,000 says coupon rate = 10%,

the future cash flows are nailed down exactly,

and that bond trades at a price equal to the present value of those future cash flows! heh

The discount rate we use to pull those future cash flows back to today is the Market interest rate,

and that number is literally what investors and issuers have landed on in equilibrium through supply and demand,

which means it’s also a number that bakes in “the market’s assessment of the company,” right?!

(ex. Samsung Electronics? In my view, yeah, you’re definitely keeping your promise on the future cash flows for the life of this bond, okay okay, acknowledged. Gimme a 5% return and I’m in. → The bond trades at the price you get by computing Present Value at market interest rate = 5%.)

(ex. GD Corporation? It wouldn’t be weird at all if you went bankrupt tomorrow, and you’re asking to borrow from me right now? Heh~ Respect for the courage. Fine, then gimme a 30% return. That’s the floor before I lend you a single won. → The bond trades at the price you get by computing Present Value at market interest rate = 30%, go ahead.)

The market interest rate determined in the market through this whole process

and the coupon rate written on the bond — together they decide whether it’s issued at par, at a discount, or at a premium,

and more specifically,

Then that $P_0$ we just calculated is the BV we record on the B/S at initial recognition, and that price goes by the name

“Amortized Cost.”

Let’s look at how this shows up on the financial statements from the issuer’s side, start to finish!

(Everyone — we are NOT doing the acquirer’s (investor’s) side lol lol lol it is genuinely, disgustingly complicated!!!!!!!! I’ll mention it veeeery briefly way at the end^^~)

So first — when it’s issued as a Par Bond, what do the financial statements look like in year 1?!?!?!?!

The Amortized Cost goes on the books as Book Value under the account Bond Payable,

and on the asset side, since cash rolls in from investors, 100,000 gets recorded.

And that cash flow (as we’ll see more when we get to the cash flow statement way at the back) gets recorded as CFF (Cash Flow from Financing).

Honestly this could be passed over without a mention, but since it’s already baked in that we’re learning cash flows eventually, feels like I’m forcing the mention in here.

Anyway, let’s lock in that cash flows tied to principal go to CFF!

And we just learned the accounting treatment using amortized cost.

For a par bond like this, the amortized cost just ends up equal to the face value. T_T

We kick off with 100,000 as the amortized cost,

and if we run the effective interest rate method, it just keeps riding along like this.

That checks out!?!?! hehehe

So the ongoing accounting treatment shakes out like this.

Right?!?!?!?!

The expense that goes out each period is interest expense.

As we’ll get into when we hit the cash flow statement later,

(OK, we won’t go that deep, but)

for interest expense,

under US-GAAP it’s classified only as Cash Flow from Operations,

while under IFRS, interest expense can go one of two ways.

It can be classified as CFO like under US-GAAP, or it can be classified as CFF — cash flow from financing activities… heh.

This is one of those spots where IFRS is a little sloppy, but let’s just keep it in the back of our heads! hehe

So from all that, two things to file away.

Anything tied to principal → CFF.

Interest paid → CFO only under US-GAAP, but CFO or CFF under IFRS.

(This is interest expense! Interest income is a separate conversation! But I’m not touching interest income here.)

Yes!!!

OK now we get into the actual meat.

- When the company issues as a Discount Bond.

Since we’ve fully made peace with the effective interest rate method,

we already know what the bond looks like on the B/S from the start of x1 through the end of x3 under these conditions.

Just run the numbers:

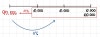

(beginning of x1) → (end of x3)

97,556 → 98,287 → 99,099 → 100,000

So the year-1 financial statements come out like this.

Well, the only tiny difference is that less than 100,000 in cash rolls in,

so on the B/S it gets amortized through a contra account called discount on bonds payable.

OK OK OK OK, and —

here’s something kinda important — we already knew the amortized cost at the end of x1, right?!?! How much was it?!

It was 98,287!!?!?!

But how exactly do we compute 98,287?

It’s “the present value of the remaining future cash flows from that point forward,” right???

Sure, starting from the initial price of 97,556,

doing ×1.11 − 10,000 gets you there too,

but it’s worth knowing the principle: “present value of the remaining future cash flows from that point on.”

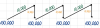

As a diagram,

it looks like this!

And I already wrote out all the ongoing accounting treatment too. hehe

Since all of it was covered back in the par bond case,

there’s nothing really new to call out separately. heh

So if we watch how this bond’s BV (book value) moves

(well, it’s all stuff from the previous post on the effective interest rate method, but)

you can see the diagram climbing up to the upper right like thiiiiiiiiiiis!?!?!

The principal slowly rising (and so the discount on bonds payable slowly shrinking)

— that’s the shape of borrowing money in discount-bond form. hehe

OK OK OK OK, there are also a couple of things worth knowing,

and what are they?

“How much is the ‘interest expense’ the company records on the I/S in year xx?!!?!?”

And

“How much is the total interest expense the company pays, all-in, by issuing that bond?!?!??!”

Exam questions can totally be structured so all you need is one of those numbers.

But if you drew out the entire amortization schedule just to answer that one question,

you’d be answering at a glacial pace, right?????

So let’s lock in this principle.

- The interest expense recorded in the current period is always the effective interest rate × the BV (the liability I’m currently carrying) of the bond at the beginning of that fiscal year.

(And if it was disposed of on April 1 of year xx or something, you only need to pay interest expense up to that point, so you compute the interest only for the months actually held out of the 12. — In practice, it’s originally calculated on a daily basis, but since intermediate accounting exam problems are usually built so you can solve on a monthly basis, the formula above is monthly too!)

- And the total interest expense you pay, all-in, is

the cash flows you pay out over the future period (in the example above, 10,000 + 10,000 + 10,000 + 100,000) minus

the money you received when you borrowed (97,556),

and it’s honestly obvious that the actual interest you end up bearing for having borrowed that money is exactly that, right?!!??!?!?!

For reference, keep in mind US-GAAP also lets you use a method that spreads the total interest expense (in this example, 130,000 − 97,556 = 32,444) equally over the years, straight-line style. So in this example, 32,444 spread over 3 years means recording 10,815 per year as interest expense is allowed under US-GAAP — just file that away!

Alright, let’s look at the premium bond case too!

Since we’ve seen all the principles already, let’s blast through it with diagrams!

The diagrams look completely identical, right?!?!?! hehe

Yeah yeah yeah, so in that case

this time,

Since it’s literally the same, we can just move on, right?!!?!?! hehe

So I think the basic bond accounting treatment you need at the CFA Level 1 level is pretty much all covered. hehe

Let me hit just a few side items a tiny bit more

and wrap this post. :-) hehe

Up to this point, I haven’t mentioned costs for issuing the bond. (They’re called issuance costs…)

But in reality, to issue a bond an underwriter like a securities firm gets involved in the middle,

and you have to pay fees to that firm for running the operation.

Meaning, in the discount-bond example above, instead of receiving 97,556 clean, you receive 97,556 from bondholders, and out of that amount,

once you tally up all the costs of actually issuing the bond, it works out to 3,000 in costs,

so the money that actually lands in our company is 94,556 — that’s what I mean.

Then how do we account for this?!??!

The money we borrowed from bondholders is 97,556, so the bond is booked on the B/S at that amount, and the 3,000 just hits the I/S as a separate expense.

Or, we just treat the amount our company borrowed as 94,556.

The answer is 2.

Because you straight-up cannot expense the 3,000……..

Under accrual accounting, expenses get matched to revenues — but there’s no revenue to match this against…..

So the borrowed amount itself gets booked as 94,556.

This part is just for reference now. heh

Everyone —

this is where it’s decided whether you really, truly understood the effective interest rate method.

OK OK OK OK OK OK

let’s get this.

The 97,556 we received was the present value pulled in by discounting the future cash flows at 11%, right?!?!?!

Right?!??!?!?!

And these investors are expecting an 11% return, and they’re waiting for the money that matches that.

The money that matches is 10,000 (year x1), 10,000 (year x2), 110,000 (year x3), right!?!?!?!?

As a diagram,

naturally — since it was the value pulled in at 11%,

if you give them back exactly those cash flows, you’re giving them the 11% rate.

But if there were issuance costs

From this point on, if you honor the promise you made to the bondholders,

it’s clearly never going to be 11% anymore.

The company, trying to do accounting at the 11% effective rate,

cannot go expense 11% of 94,556, which is 10,401!!!!!!

The promise to the bondholders is 11% of 97,556, which is 10,731 — that’s what has to get expensed!!!

So at exactly what rate does the company have to run the effective interest rate method accounting?

I tried to nail it pretty precisely. lol lol lol lol lol

It comes out exactly at 12.27762%. lol lol lol lol lol

(Face values on bonds often go up to 10 billion won, just like that, so sensitivity down to the 5th or 6th decimal place can actually matter. In practice, when leasing a very expensive asset like an airplane (leases are almost the same as bonds, we’ll cover it in the next post),

when you’re computing the effective interest rate at that point, apparently in practice they set it with extreme sensitivity down to the 6th or 7th decimal. hehe)

(Anyway, because I didn’t bring my financial calculator….. the price of finding this value was enormous. T_T T_T Everyone, carry your financial calculators. T_T)

Did that land?!?!?!

Ha-hah!

Then let’s move on!!! hehe

And next up, there’s the case of a Callable Bond….

Wow lol lol lol lol, after going through intermediate accounting and then looking at this, it was brutally merciless.

We haven’t even learned things like condition changes or accrued interest treatment for bonds,…..

and yet they’re already teaching Callable Bonds…….

Anyway, a Call on a bond is the issuer’s right.

The right to say “hey everyone, I’m paying back everything I borrowed from you, right now.”

You can issue a bond with this kind of option attached.

Then why would a company decide to pay it all back at once?

Obviously, the decision gets made when paying it all back and re-borrowing is more advantageous. hehe

(The advantageous situation could be driven by the broader market economy, or it could be something specific only to that company.)

Anyway, when you do that kind of repayment,

a current-period gain or loss can pop out like this.

A current-period gain/loss of BV − FV can arise~.

Since it’s really just a matter of recognizing that and being able to calculate it,

it’s not hard!!!! hehe

Last one.

Do NOT use this part as reference, for real lol lol lol I’ll just ramble a tiny bit!

So the bond we’ve been looking at represents, on the B/S, the “current obligation the company is carrying” under Liabilities, right?

Within that, we’re looking specifically at the “financial liabilities” side,

and financial liabilities are actually classified into six types.

But in intermediate accounting, where you learn how a single company does its own accounting, you only learn about 2 types — AC financial liabilities and FVPL,

and in advanced accounting, where you learn about consolidating multiple companies, you learn the remaining 4 types.

Anyway, AC financial liabilities and FVPL financial liabilities (these are the IFRS names).

(On the financial asset side, they split into AC financial assets, FVPL financial assets, and FVOCI financial assets. ^^ hehe There’s no symmetry or anything like that.^^^^^^^^^ How wonderful.^^^ hehe)

What we saw above — the general treatment following the effective interest rate method at amortized cost — is the accounting treatment for AC financial liabilities.

But there’s actually also a classification called FVPL financial liabilities, where — forget the effective interest rate method — any income or expenses from it just get hammered straight onto the I/S as expenses, apparently. hehe

But to be classified as FVPL financial liabilities…. it has to be held-for-trading stuff (items intended for repurchase in the short term, or derivative instruments (for hedging)), or alternatively a case where an accounting mismatch pops up, in which case the company can designate it as FVPL, but……

There’s a veeeeeery tiny mention of FVPL in IFRS terms up above. :-)

Meaning: they wouldn’t actually ask about the accounting treatment for this on an exam.

If they have any conscience!!!!!!! lol lol lol

Oh, and the truly last thing.

Since our dear bondholders are people who worry a lot about “what if I don’t get my money back!!!!!!!!”,

naturally they can attach all sorts of conditions when lending money.

(This will get covered in more detail in the Fixed Income subject anyway, but)

these conditions are called Debt Covenants, and the info about them is described in something called the Bond Indenture of the bond. hehe

If we try to classify the kinds of conditions that can be attached, they split into Affirmative / Negative and so on….

Since this part gets covered in detail in Fixed Income anyway,

no worries no no no no,

and since we have completely nailed the effective interest rate method accounting treatment — which is the single most important thing for exam purposes —

let’s move on to the next chapter with peace of mind!!!!!!!!!!

The very next one is!!!!!!!!!!!!

Leases!!!!!!!!!!!!!!!!!!!!!

Originally written in Korean on my Naver blog (2021-07). Translated to English for gdpark.blog.