Equity

A casual (expectations: low!) walkthrough of equity on the balance sheet — paid-in capital, par value, share premium, and just enough accounting cycle to get by for the CFA exam.

Earlier we covered things like inventory and tangible assets in at least a bit of detail, but for the other line items showing up on the B/S and I/S, the plan was to just look at them roughly~

So that’s the spirit we’ve been going in. We already covered financial assets and accounts receivable, right???

Continuing in that same spirit, looks like it’s time to knock out a few more line items.

Since this is a “look at it roughly” kind of session, I’d say keep your expectations low — putting that out there first —

and now let’s dive in!!!

This time we’re looking at the Equity side.

We haven’t really gone deep on Equity up to this point,

and the plan here isn’t to go deep either, heh heh heh

(BUT — since we’re going to try to wrap our heads around the “accounting cycle” this time around, focus focus!!!! Most important part!!!!!)

First things first — what’s the definition of Equity?

Asset − Liability. That’s literally the definition heh heh heh

This can get a little confusing, so let me just say it plainly once.

Equity’s value equals Net Asset value, which is Asset − Liability.

Huh?!?!? What does that even mean lol

So,

“Equity is something that describes net assets.”

(This is one of those parts where you kind of need the accounting cycle in your head to really get what it’s saying…) Anyway, heh heh heh

For our CFA exam purposes, we don’t look at every single thing in Equity — apparently 4 things are enough.

Here they are.

OK, first up — number one!

1. Paid-in Capital

Simply put, this is the money shareholders paid into the company. It’s called Contributed Capital.

Paid-in Capital itself splits further into two pieces.

Capital stock — that’s ‘자본금,’ and

Additional Paid-in Capital — ‘주식발행초과금,’ aka 주발초.

How are each of these calculated and shown on the B/S?

Capital stock = par value × number of shares issued. That’s what shows up.

And when shares get issued above par value, the leftover crumbs pile up in an account called share premium.

For example: 1 share of common stock with par value 5,000 won issued at 7,000 won?

Capital stock 5,000 / Share premium 2,000

— like that.

And actually there are cases where a stock with par value 5,000 is issued at 4,000, and in that case, instead of share premium, it gets recorded under a line item called ‘discount on stock issuance’….

No… why bother going through the trouble of splitting it up like this?

And the near-universal rule in our country’s stock market is that pretty much every stock has a par value of 5,000 won…..

(There are stocks that aren’t par 5,000, but it’s true there really aren’t many of them… heh)

So the reason for going to the trouble of splitting it up like this — first reason:

if capital stock is shown as par × number of shares, it makes calculating the number of issued shares super convenient.

Second reason:

share premium gets classified as capital surplus on the B/S, and the idea is that later, if the company’s financial situation gets really dicey, this is the cushion sitting there to relieve the pain~ — or so the story goes,

but it’s not important content, so let’s just leave it at that and move on~ heh heh heh

Oh and also — about preferred stock capital that shows up in Equity. Only Callable preferred stock gets recorded in Equity,

and Redeemable preferred stock gets recorded on the Liability side. We mentioned that in a previous post, right? ^^ heh heh heh

* Fun practical-world story

The “Redeemable” attached form is actually used a lot in things like Pre-IPO, apparently.

Before a company goes IPO, you have to attach options like Redeemable to attract investors, they say… heh heh

But wait — why do companies want to do Pre-IPO????

1. Could be to grab more funds via pre-IPO before the full IPO, then either start a new business or push sales further so they can get a higher valuation when IPO time comes.

2. To clean up the major shareholder’s stake a bit during pre-IPO — because once you go public, stake disclosures can mess with the stock price and that becomes a burden later.. heh heh Anyway, the form most often received in pre-IPO situations is apparently RCPS (Redeemable Convertible Preferred Stock).

You stack one more right on top of RPS — if we can’t get to IPO, pay us back via Put,

and if IPO does happen, the goal is to convert and exit into the market… that’s the pur…pose, heh heh heh

K-GAAP looks at this RCPS legally and books it as Equity, but when you go IPO you have to switch to IFRS, and under IFRS all RCPS jumps up to Liability — which creates situations where companies can’t go IPO at all, so… apparently this is a really important issue in practice, heh heh heh

In school or textbooks, preferred stock gets taught as ‘shares without voting rights,’ but if the articles of incorporation say voting rights are granted, then preferred stock can come with voting rights. (In the US there are tons of cases like this, so people sometimes assume preferred stock naturally comes with voting rights.) Then what does preferred stock give priority to?

1. Priority on dividends.

2. Residual claims on assets — preferred goes ahead of common.

There are also No Par shares, which have no Par Value (face value).

In the US, No Par is actually more common,

and in Korea, No Par isn’t impossible but apparently there just aren’t many companies issuing them.

OK OK, let’s keep going.

The number of Issued Shares came up above,

and we kind of need to nail down the concept of share counts a bit better.

The different types of share counts need to live cleanly in your head by concept.

Authorized Shares: 수권주식수.

Written into the articles of incorporation as “we plan to issue this many shares going forward.” This is the amount approved by shareholders.

Within this authorized count, the board of directors can decide on its own and adjust the number of shares without having to call a shareholders’ meeting and get shareholder approval… it’s basically a ceiling, you could say?

(Total planned shares to be issued.)

Then within that ceiling, there’s a chunk that’s already been issued, and a remaining chunk up to the ceiling that hasn’t been issued yet.

Issued Shares is exactly that — the number of shares issued to date.

The remaining chunk up to the ceiling that hasn’t been issued is called Unissued Shares.

Among issued shares (Issued Shares),

we further split into “Outstanding Shares,” which are the shares being traded in the market,

and “Treasury Stock,” which is the chunk that was issued but the company itself is holding.

OK and now the next line item — Retained Earnings (이익잉여금).

This one is… well… calculated as Beg R/E + Net Income − Dividends declared….

This is easy, so… can we skip??!

Ahh but it feels a little sad to just skip past it, so let me say juuust a tiny bit more about retained earnings hahahahaha

(Honestly, recommend just Skipping.)

Retained earnings is actually further broken into 3 subcategories.

Retained earnings ⇒ Unappropriated retained earnings / Legal reserves / Voluntary reserves

We said earlier that Net Income gets reflected in retained earnings,

but more precisely, it gets reflected in “unappropriated retained earnings.” That is, the line item representing “the company’s capacity to pay dividends” is this one right here.

Then what are legal reserves and voluntary reserves?

Legal reserves are “the portion the law mandates you set aside” (in our country, the line item ‘이익준비금’ = profit reserve is used).

It’s mandated by Korea’s Commercial Act, and the rule says: “in the case of cash dividends (including dividends in kind), at least 1/10 of the dividend amount has to be set aside as profit reserve until it reaches 1/2 of capital stock” — meaning, “once the legal reserve crosses 1/2 of capital, you don’t have to do this mandatory ‘setting aside’ anymore.”

Net effect: at least 1/10 of the dividend stays parked in retained earnings before the dividend gets paid.

(I didn’t mention stock dividends. A stock dividend swaps unappropriated retained earnings for capital stock, and since the substance of that transaction isn’t actually distributing wealth to shareholders…. heh heh it’s tricky heh heh heh It’s content you don’t really need to know, so I’m just cruising past it too hahahahahaha If you’re curious, please step into the world of Intermediate Accounting (for CPA)~ Welcome to hell heh heh)

Let me just do one rough pass on voluntary reserves too.

These are line items the company sets aside voluntarily — not regulated by law, just decided by the company on its own. (On an actual B/S you’ll see line item names like “business expansion reserve” or “sinking fund reserve.”)

Why would you set anything aside here?!?!

If there’s 1 trillion sitting in unappropriated retained earnings, shareholders might start going “stop locking it up in unappropriated and pay us dividends already!!!!!!!!!!!”

Isn’t this a move to break that? The company shoves some into voluntary reserves, like —

“Shareholders…. please, please don’t ask for dividends ^.^ The money we made is meant for us to bet on the right investment, or to deploy when a business plan comes together so we can earn even bigger money ^.^ Believe Me!” — something like that, I think, is the intent heh heh heh heh

Oh and above I used terms like “set aside (적립), transfer (대체)” etc.

Basically, when current period net income lands in unappropriated retained earnings,

some of that amount can flow to legal reserves, or it can flow to voluntary reserves, right?

Sending it whoosh~ over to another retained earnings item like that is called “setting aside (적립).”

And from voluntary reserves, you can also send it back to unappropriated retained earnings and just pay it out as dividends.

Sending it back from voluntary to unappropriated is called “reversal (이입).”

Just terminology….. ^^;;; heh heh heh

Yes yes, you skipped! Right?

That was an excellent choice hahahahaha

OK then, next!

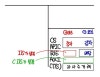

Number 3 on the list above was AOCI,

but instead of doing AOCI, to finish off the shares-side stuff first,

we’ll hit number 4 from the list — Treasury Stock — first, and then circle back to Accumulated Other Comprehensive Income.

4. Treasury Stock (the official Korean name is 자기주식 but… heh)

Actually, 자사주 and 자기주식 are technically different words…. heh heh A share that an employee of a company buys in their own company is called 자사주 (employee share ownership),

and when a company buys back its own shares, that’s 자기주식취득 (treasury stock acquisition)….

Hmm…. like if I’m working at a listed company and I bought shares in my own company….

But if the financial statements somehow magically went “oh?!?!? Our company’s employee GD Park bought our company’s shares!!!!!!!!!!!!” and reflected that in the financial statements….

the management support team might come for my head hahaha for causing chaos hahahahahahahahahaha

Anyway — shares an employee buys in their own company → 자사주 / a company buying its own shares → 자기주식.

There’s a distinction in the words, but for convenience I’ll just use 자사주 / 자기주식 interchangeably heh heh heh heh

(No wait… I should fix all the terminology later heh heh heh)

Anyway — treasury stock. The company can’t exercise voting rights on it.

Because the Commercial Act defines it that way.

For something to qualify as an Asset,

a key requirement is that the company has to be able to Control it.

But it can’t even exercise voting rights;;; what;;;;

So treasury stock goes in as a contra-account deducted from equity. That’s exactly what it is, heh heh heh

But here’s the thing even rookie investors know —

when news comes out that a company is buying back its own shares, the stock price goes up, right?????

Why does a company do a share buyback?!?!?!?

1. Stock price support: open up any value investing book and you’ll see this — company insiders know the outlook better than anyone, and their decision to buy back shares is a clear positive signal~

And apparently it’s clearly effective in the short term.

BUT — the fact is, share buybacks don’t actually improve a company’s fundamentals!!

The model accountants tend to use a lot when valuing a company is something called RIM — Residual Income Model, I think.

Anyway, according to that model, share buybacks don’t move the fundamentals so…..

2. Defense against hostile M&A & 3. Strengthening the controlling shareholder’s stake.

4. Employee Benefit: buying in advance to prep for employees exercising stock options or for employee stock ownership plans.

OK that was the fun-story portion,

now back to exam mode!

A company can transact in its own shares in 3 ways:

Share buyback / Reissuance / Retirement.

For each of these, you need to understand the effect on the B/S.

Since this is a contra-account to equity, it can get a little confusing,

but since it’s shown up on the exam before, you need this much down!

(Honestly, you just need to nail the logic and re-derive it when solving questions, so it’s not that bad… heh heh)

And among the equity accounts, one more thing you need to know:

5. Non-Controlling Interest (NCI) — there’s a thing called 비지배지분 (non-controlling interest).

This actually wouldn’t show up in intermediate accounting, which deals with the accounting treatment of a single company.

Because the non-controlling interest account appears in consolidated financial statements,

and consolidated financial statements pull in info from multiple companies including subsidiaries the parent has obtained control over,

so this is something studied in advanced accounting……..

And advanced accounting is the domain of CFA Level 2!!!!!!!!

So we don’t need to know it in detail — just know it simply.

Um…….

The diagram explains it too, but let me say it really simply and roughly.

Easier feel if I phrase it in terms of a line item, so let’s use inventory as the example.

Say Company A’s inventory is 1,000, and Company B’s inventory is 100.

But A holds 80% control over B.

Common-sense reading: A’s consolidated financial statements should record inventory as

1,000 + 100 × 0.8 = 1,080

but —

accounting doesn’t do it that way.

In A’s inventory line, it writes the full 1,000 + 100 = 1,100,

writes all of it,

and then writes 20 in the “non-controlling interest” line in equity.

So in the end the net assets reconcile to 1,080 —

that’s the accounting treatment.

Really weird, right???? But, as you study advanced accounting, you’ll start to feel that this method is actually more rational.

Details — see you at CFA Lv2!

And finally, the one we jumped over earlier —

AOCI (Accumulated Other Comprehensive Income).

Let’s look at accumulated other comprehensive income.

OK now this one…….

is content where you really need to grasp the accounting cycle from a big-picture perspective,

so let me explain it simply.

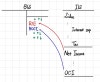

First — what shows the main financial info of a company?

Of the 5 financial statements,

the B/S, which shows the accumulated results since the company was founded,

and the I/S, which shows the results of the period being reported on this time —

these two are what you’d call important.

And the B/S has

the credit side, which shows how the company has been Financing,

with the credit side broadly showing how much was financed from creditors and how much from shareholders,

and the debit side showing how the money raised that way got invested.

Then there’s the concept of net assets of the company,

and what describes those net assets is precisely capital (Equity), they say.

The capital accounts that describe net assets — you could call them the core of the B/S,

and these capital accounts basically — how do they work —

A company gets created and earns money. When money’s earned, it has to be distributed to stakeholders.

First it goes to creditors.

The government is also a stakeholder. So results get distributed via Tax.

What’s left over is exactly the shareholders’ share,

and within this shareholders’ share there’s Net Income, which gets reflected in retained earnings that can be claimed via dividends,

and there’s OCI, which is also the shareholders’ share but cannot be claimed via dividends, and gets reflected in the AOCI account.

(Net effect: when a company produces results, those results have to be classified — Net Income or OCI? For example, money earned from selling goods? -> Net Income. Gain/loss under the revaluation model on tangible assets the company holds? -> OCI. That kind of thing.

But the types of gains and losses classified as OCI are 7. CPA students memorize them with the mnemonic 재재금관파해라. For CFA purposes, we’ll define 5 below.)

But — is the thing that describes net assets necessarily made up only of the company’s results???? No. As we saw above, things like treasury stock move through the company’s own direct transactions, right?

Anything not moved by the company’s results,

we say got moved by “transactions with shareholders,”

and stuff from transactions with shareholders gets “directly reflected” in the Equity account.

That was super brief,

but this is the big accounting cycle….. heh heh heh heh heh heh heh

OK back to CFA,

inside the results a company achieved during the reporting period, there’s Net Income and Other Comprehensive Income.

Let me bring this back to mind once and continue.

In the changes to net assets,

let’s split it into transactions with shareholders, and stuff from results (Net Income + Other Comprehensive Income).

Out of these, the stuff from results is what we call Comprehensive Income!

Please get this once,

and ultimately, as I explained above,

changes in Equity, which describes net assets —

Net Income gets reflected in R/E & OCI gets reflected in AOCI, like this.

Wait a second!!!!!!!!!!!!!!!!!!!!

What even is OCI!!!!!!!!!!!!!!!!!!!!

I literally just said “it’s the shareholders’ share but cannot be claimed via dividends” —

what on earth is that?????????????

(This is content we touched on over on the tangible assets side.)

First — among the stuff we’ve studied, what OCI showed up? Let’s get the feel from there.

Under IFRS, PPE can be managed under the Revaluation Model, and under this model,

things that feel like Unrealized Gain / Loss on that tangible asset got classified as OCI and reflected in AOCI.

Why?!?!?!?

50 years ago the company bought a small plot of land in Seoul to do business on,

and continued doing business….. and then 2020 rolls around and that land has gone to the moon…..

It was clearly bought for 50,000 won, but now it’s worth 5 billion;; haha hahahahaha hahaha

From the shareholder’s perspective?

Hey!!! That’s my money!!!!! Everyone knows it went to the moon, so hurry up and pay it out as dividends!!!!!

If that flew, this company would now have to sell the land to pay dividends.

Then… it wouldn’t be able to keep doing business either;; this can’t fly, so —

since it can’t be claimed as dividends but is still genuinely the shareholders’ share (it’s the share they’d receive if the company stopped doing business and liquidated),

the concept of other comprehensive income was born…. heh heh heh heh heh heh heh

OK so the items classified as other comprehensive income — I said there are 5 to memorize for CFA purposes.

What are those 5?!?!??!?

How are you supposed to memorize this (crying)………

Let’s just designate this as a list you skim once right before the exam!!!!!!!!

There’s no other way hahahahaha I can’t memorize it hahahahahahahahahahahaha hahahahahaha

The vibe is that most of them feel like Unrealized Gain & Loss.

(They are absolutely not all unrealized gains/losses.)

And one more fun story to wrap up —

It’s only been about 10 years since they started showing the statement of comprehensive income,

so why did they suddenly decide to show it…… ?!?!?!

What is accounting again?!

I think the definition was something like — a system that provides useful information to information users.

What would matter to those information users?

Showing the substance of the company well — that’s the obvious first thing,

but reflecting financial info into stock prices is also a key point you can mark down.

There was apparently a debate among accounting academics on the latter point — about OCI specifically.

“Hey….! What’s so important about how much some piece of land is worth, or unrealized gains/losses from FX rates and stuff… this company isn’t suddenly gonna sell that land, and it’s not like they’re gonna instantly liquidate their overseas investments right now, so why do we have to put this in results…?!!??!”

“No no, it might actually matter — looks like it has a pretty strong effect on stock prices.”

“Oh really!? Wanna run an experiment?!?!”

And they ran experiments on stock markets all over the world,

and the result came out…. weirdly….

fifty-fifty, they say….

So they decided to start showing OCI,

and apparently that’s why we’ve had it for about 10 years now… heh heh heh heh heh heh heh

How interesting how interesting how interesting heh heh heh heh heh heh

Originally written in Korean on my Naver blog (2021-09). Translated to English for gdpark.blog.