Types of Bonds

A quick rundown of bond types by how they pay interest — floaters, inverse floaters, PIK bonds, index-linked, and the contingency provisions baked right in.

Alright, let’s keep rolling!

Last time we said we’d classify bonds by how they pay interest — which, honestly, basically just means classifying the types of bonds out there.

So… what kinds are there?

1. Floating Rate Note (FRN, aka Floater)

A bond with a variable interest rate. The coupon floats around with some reference rate.

2. Inverse Floater

Inverse floating rate bond (?)

Yeah — exactly what the word “inverse” suggests. It moves opposite to the reference rate. Reference rate goes up? Coupon goes down. And vice versa.

3. Step-up Coupon Bond

You can pretty much tell what this is just from the name — the coupon rate steps up in stages as time goes on.

So this hedges you against rising-rate risk to some extent. Nice.

(Apparently it usually comes paired with a callable feature.)

4. Credit Linked Coupon Bond

The coupon is linked to creditworthiness — credit gets better, coupon goes down; credit gets worse, coupon goes up… heh.

5. PIK (Payment-in-Kind) Bond

This one’s different in how the interest gets paid.

Interest is paid out in more bonds — same kind, “in-kind.” Then at maturity, the principal plus all those accumulated bonds-as-interest get paid out together in cash.

From the investor side, yeah… that’s a bond with absolutely massive credit risk hanging over it.

(Apparently it gets used in the early days of a company, when there’s no real cash flow yet.)

6. Index Linked Bond

Just like the name says — linked to some index.

Now, since the inflation-linked variant naturally falls under this bucket, let’s actually think it through.

OK, so suppose we link only the coupon to inflation.

The 3% coupon becomes 3.3% once you bake in π.

⇒ But the Face Value (par) doesn’t have inflation baked in… so you’re not fully protected against inflation. Half-measure.

So how do we get inflation reflected cleanly in both the Face Value and the Coupon?

⇒ Link the Face Value to π, and just leave the coupon rate alone!

Then Face Value = $1,100.

And paying 3% on that gives $33 — which is exactly the same as paying 3.3% on $1,000! Same thing.

* But wait — what if deflation hits? Couldn’t you end up not even getting your principal back?!?

- You can make it Principal Protected.

- Or you can build it as a pure interest-indexed bond, where only the coupon does the floating. That’s what they say, anyway.

Contingency Provision

“When some specific event happens, this thing kicks in~” — written right into the Bond Indenture.

It’s also called an Embedded Option, in the sense that it’s baked in — you can’t peel it off and sell it separately.

In plain terms, it just means the bond has one of these riding inside: 1. Callable / 2. Putable / 3. Convertible.

So a bond with no Contingency Provision attached is called a straight bond, or option-free bond!!!!

Hold on!!!!

Callable = the issuer’s right (good for the issuer / bad for the investor)

Putable = the investor’s right (bad for the issuer / good for the investor)

Now — since we already roughly picked up what an option is from the Derivatives section…

(And if you didn’t, totally fine — we’ll get to all of it la~~~ter ^.^, and it’ll be covered properly when we hit Fixed Income Valuation. So for now, just treat this like a vocab-organizing pass!!!!)

…assuming we know, and just sketching Callable Bonds with broad terminology-organizing strokes:

If it’s a Callable Bond, the style splits into three flavors based on when the right can be exercised.

If you can only exercise it at one specific date, at a set price (exercise price / strike price) — that’s European Style.

If there are multiple set dates, each with its own exercise price — Bermuda Style.

And if it’s none of those — i.e. you can pull the trigger any time during a set window — that’s American Style!! heh heh.

(Honestly, totally fine if none of this makes sense yet!

The whole point is to absorb every CFA subject,

and once you’ve absorbed them all, it’ll all click!)

Also, some terminology to file away around option exercise:

Just take the terms call protection period and now callable with you!

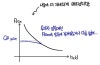

When and why would the right actually get exercised?!?!!!?

A fall in interest rates means bond prices go up (you’ll feel this in your bones once you do Valuation).

But think about it the simple way — the issuer (the person who borrowed money) borrowed at 10%, and now the market lets them re-borrow at 5%? Come on.

In that situation, if they have a clause that says “you can just pay everything off right now” — yeah, of course they’re paying it off.

Pay it all off, then re-borrow at 5%. lol.

So the moment an option like this gets bolted on, it’s just a given that the bond’s value goes up.

(How much it goes up depends on how juicy the conditions are.)

And flipping it around — from the perspective of the investor on the other side of a bond the issuer can just call away whenever:

“Ugh… past a certain point, they’re always going to exercise, so my upside literally caps out here.”

That kind of —

— that kind of picture!!!!! lol lol lol.

Don’t stress! We’ll grind through this in actual detail later, haha.

So much detail it’ll be a problem!

OK so — for a Callable Bond like this, which from the investor’s standpoint (the person lending the money) seems like nothing but a raw deal…

…are there actually investors who’d touch it?!?!

⇒ Yeah, of course, of course. Investors will just demand a higher yield to compensate for how lopsided it is. (Higher yield → cheaper price.)

So the gap between the same bond with a Callable feature versus without

is exactly the price gap that comes from that feature,

and that price gap can basically be read as the “value of the Option,” right?!?!?!?

(Which means — congrats, you already grasped one whole methodology for pricing options.)

Make-Whole Call Provision

This is when the Call gets exercised at a price of

Max(Market Value, Par + Accrued interest),

and because of that floor, there’s literally zero chance the investor takes a price loss on the deal.

Then why does this kind of Call even exist?

Apparently it’s used as a defense against hostile M&A.

(Like — “Hey hey hey hey?!!? Hold on — are you trying to take over our company right now??? Bro, the second you close that acquisition, you’re on the hook for exercising every single make-whole call bond — that’s gonna hurt, isn’t it??? Don’t do it.” (annoyed face) That kind of vibe?)

Anyway, the Fixed Price Call we were just talking about is the issuer’s right, and the one who benefits is the issuer!!!!

On the other hand, there are also Putable bonds — and since this one’s the investor’s right, the investor’s the one who benefits.

So when would the investor actually exercise it????

The mirror image of Call — when market rates rise (bond prices fall), you exercise Put, pull your money back,

and then drop it into newly issued bonds at those juicier rates, right?

(If framing it through bonds is confusing, here’s the more intuitive version: I lent money at 5%, but everyone borrowing now is offering 10%.

If I happen to have the right to tell my existing borrowers “pay back all~~~ my money. Right now,”

I just say pay it back now!, claw the money back, and re-lend at 10%. lol lol.)

Convertible Bond (CB)

A bond with the right to convert into stock baked in.

So when a CB gets issued, these are the things locked in at the time of issuance!

One thing to remember:

conversion is basically a “barter swap.” You give up the bond, you get the stock.

And the shares you convert into are newly issued shares — not ones already floating around the market!

There’s usually a conversion lockup period set,

but in any case, compared to just holding the stock outright, with a CB you’ve got zero risk of pure stock-price downside —

meaning, your downside is capped at… well, the value of the bond. That’s your price floor.

And because it’s that good a deal, the price is, predictably, way more expensive to match.

Warrant — this one’s similar to a Call option. It’s a bond with a “right to subscribe to new shares” attached.

That is — CB was a straight barter, bond-for-stock,

whereas a Bond with Warrant (bond + subscription right) actually requires a cash transaction to get the shares.

(Look at this. Coming straight off the FRA grind, CB and BW are basically just vocab-level definitions, right!?!??!)

Contingency Convertible Bond (aka CoCo Bond)

It does convert — but only automatically, and only when certain pre-set conditions get tripped.

(ex. When the BIS ratio improves past some threshold, it auto-converts to stock.)

Phew…. so many bond types….

We’re still in the pre-Valuation stretch of Fixed Income,

so this isn’t the main event, and yeah, it’s not the fun part either.

Hang in there just a little longer until we hit the fun stuff!!!!!!

Originally written in Korean on my Naver blog (2021-10). Translated to English for gdpark.blog.