Bond Valuation

Bond valuation is just PV of future cash flows — once you lock in why price adjusts to match required return, the rest of fixed income stops wrecking your mental health. heh heh!!

Now the real Fixed Income content kicks off!!!!!

No less than… Bond Valuation finally starts. Right now!!!

I said “Bond Valuation” like it’s some big deal, but…

honestly, we already know this one.

Bonds, stocks, derivatives, land, buildings — whatever the asset, valuation is always the same thing:

“the present value of future cash flows.” That’s it.

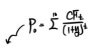

So say we’ve got these 3 bonds up on the board.

We can line all of them up as present values.

Let’s say there’s a bond with a face value of $1,000, a coupon rate of 10%, and a maturity of 10 years.

Then the future Promised Cash Flows are already locked in.

All we have to do is drag those cash flows back with a discount factor to get the present value,

and if we discount at 8% / 10% / 12% respectively, each bond’s present value pops out differently.

So what does that difference actually mean??????????

If the Required Rate of Return is 8%, that means the market is asking for 8% interest,

but a 10% coupon is handing over more than what market participants are demanding, right????

So is this bond secretly tossing market participants an extra 2% on top???????

Nope nope nope nope nope nope nope nope nope nope, it’s not. lol The price just shakes itself out to deliver exactly 8%, on the nose.

If the bond’s price forms a bit on the higher side,

it gets nudged back into line to match the market participants’ required rate of return.

(And to be clear — it’s not the issuer sitting there setting the price. It’s market participants trading the thing, going “whoa, a bond paying 10% on $1,000? I’d call that fair at 1,050!” and the guy next to him goes hey I’d call it at 1,100! and then boom, the price gets pushed up to 1,134, converging to the equilibrium price.)

So summing it all up, here’s the picture.

When the market’s required return equals the coupon rate, the bond trades at face value,

when the coupon rate is higher the price goes above face / when the coupon rate is lower it drops below face —

you really have to lock this principle in.

That way the bond stuff that just keeps coming after this / even into Level 2, your mental health will not be in a constant state of decay! heh heh heh

I strongly, strongly recommend doing the discount-and-sum on those Cash Flows by hand at least once. heh heh!!

OK so — in a market where the required rate of return was 10%, a bond with a 10% coupon was trading at Par Value,

and then suddenly the required rate in the market jumps to 12% —

(like, hey man, I think the economy’s about to turn, so if you want me to take this trade, you’ll have to price in a higher return for me — that’s the kind of thing that forms the bond price)

anyway, if the required rate suddenly moves, it’s going to show up in the bond price, right!?

Let’s study that.

First up, for a bond with coupon = 10%,

let’s draw a graph as a function — how the price shakes out

for every possible required rate —

drawn out, it looks like this.

First, this kind of curve is called the “Price Yield Curve” — (y-axis is price, x-axis is yield, so I guess they just named it the obvious thing)

But look at the shape of this curve — it’s convex, bowed downward, see that?

So bond prices have this characteristic:

when the price goes up, it goes up (relatively) more than it goes down,

and when the bond price goes down, it goes down (relatively) more gently than it goes up — that characteristic.

But why does that convex function show up like that???????

Precisely because of the principle that valuation of financial assets is “the present value of cash flows that will occur in the future” —

it’s because the calculation shakes out like this!!!!!

In other words, the factors that create the degree of convexity are the same ones sitting there — the y in the denominator, the CF in the numerator, whether t runs from 1 to 10 or 1 to 20 —

these factors mean that depending on what kind of bond you’re looking at, some bonds are crazy convex and some bonds are barely convex at all.

And being highly convex means the bond price responds more sensitively to changes in y,

and how each factor responds goes like this:

Ugh… but who the hell is going to memorize all of these one by one…….

I’m definitely going to forget,

so when studying bonds, it’s way better to lay the Promised Cash Flows out on a timeline and picture it in your head.

Think of it like: if you grab the trunk and shake hard from below, which tree shakes more and reacts more sensitively? — burn that picture into your head,

and then:

“Ah, the more cash flows there are in between (the higher the coupon), the less price sensitive it is.”

“If maturity is long (the tree is tall), it whips around more easily. Price sensitivity climbs as maturity stretches out.”

You’ll remember it with zero confusion, right!?!?!? heh heh heh

Anyway, the fact that the price yield curve is convex is a huge win from us-the-investor’s point of view.

But some bonds out there have a Call option attached,

where if the issuer decides things aren’t going their way, they can just pull the whole thing back and redeem it —

a bond that’s favorable to the issuer — that’s NOT going to have the convex shape that’s favorable to investors, is it!?!??!

Yep yep yep yep yep, exactly. lol lol

The Price-Yield curve of a bond with a Call option attached,

when the call is about to get exercised, doesn’t give you a convex curve — it actually draws a concave one. heh heh heh heh heh

I’m guessing this content shows up later!!! :-)

Looking at the Price-yield Curve,

can you feel it? Gain / Loss on bond price is something that happens when the market’s required rate of return changes?!

Let’s chew on this a little more.

At t=0 the market’s required rate of return was 6%,

so some bond with a 6% coupon would’ve been issued at Par — but instead of buying it at Par,

at t=1 they bought it at $1,057.82.

Because the market required rate of return had dropped to 3%, the price had climbed up there.

And they waited until t=2 — at this point the market’s required rate of return hadn’t moved from 3%,

and if you punch it into the calculator for the bond price right here,

it comes out to $1,029.34, and they sold at this point, so they unloaded the bond at that price —

so I bought at 1,057.82 / sold at 1,029.34, I took a loss, right?!?!?!?!? — you might think,

but did this person actually take a loss????

Nope nope nope nope nope, they did not. Zero Capital Gain or Loss. None.

Because at t=1, I had accepted the market’s required rate of return of 3% — that’s why I bought it then —

and since the market’s required rate of return didn’t budge, no Capital gain or loss shows up,

and they just walked out having earned exactly the 3% they had signed up for.

If you punch it into the calculator like this:

it comes out as a clean annual return of 3%, right on the nose :-))) heh heh heh

Bottom line: As long as the Required rate of return doesn’t change, when you got in and when you got out doesn’t matter to your return.

It’s only when the Required rate of return changes that capital gain or capital loss shows up.

(Also — if you don’t bail in the middle and just hold all the way to maturity, you just collect the Promised Cash Flows as promised, and you end up with exactly the required rate of return as of when you bought it, and that’s that~)

And the content that comes next is originally about the Spot rate,

but I’ll bundle that all into the next post when we hit the Yield Curve.

Skipping it here:

Skip, skip!!

Don’t stress, it’ll all~~~~ click when we get to the Yield Curve. heh heh heh

OK here, let me just quickly wrap up with a little more on bond pricing.

Bond trades don’t always conveniently happen at t=0 (issuance) or right on the dot at t=1, t=2 when a Cash Flow lands.

If a bond trade happens at some awkward in-between timing like this,

then of the Cash Flow coming in at t=1, the 1/2 that A was holding before the trade should by rights belong to A,

and half of the Cash Flow at t=1 that accrued during the green interval belongs to B, right??????

So the price at T = 1/2 is:

Starting from the clean price — the price pinned to the reference point where no accrued interest has built up yet —

you add to the bond price the accrued interest that belongs to A.

Since B is going to collect the full coupon at t=1 after taking over the bond,

rather than doing the weird dance where B gets all of it at t=1 and then has to hand half back to A,

“hey B, you’re getting all of it at t=1 anyway — so when we do the bond trade now, just stack my share on top of the price and we’re square, cool?!”

That’s how the bond transaction goes, with the accrued amount bundled into the price.

A price like this — the actual price the bond is trading at right now — is called the

Cash Price / Full Price / Dirty Price.

But then, how should we actually calculate the accrued interest…….

Do we assume interest grew daily-compounded during that stretch of time / or do we assume it accrued on a simple daily basis….

On this, the assumption is that interest accrued on a simple daily basis, calculated as coupon × (t / T), as shown in the figure above.

And counting the days also needs a standard,

there are a bunch of day count conventions, but when you’re studying for the CFA they say knowing just these two will carry you through the material without any trouble:

So the day count convention is actually different for each financial product, apparently.

For example, LIBOR-linked financial assets follow the 30 / 360 day count convention — all baked in like that. heh heh heh

(But at Level 1, they don’t seem to be grilling you on which day count convention each financial asset uses :-))

But if you want to be really rigorous about it,

assuming interest accrues by “evenly splitting” it on a daily simple basis

is a little sus….

Because in reality it would be more accurate to say interest accrues with compounding.

In theory, the price you get by computing accrued interest with daily compounding like this is called the Theoretical Price.

So since it’s daily compounding:

Picturing and feeling the difference between the simple-daily evenly-split method / and the daily-compounding method:

The difference is whether interest grows in an amplifying, ballooning way as time goes by, or whether the same tiny amount of interest pops out every single day.

The problem is….. in actual practice, whether it’s bond trading or the bond payable section on financial statements, pretty much everything runs on Full Price,

and daily compounding basically never shows up……

and yet, in the CFA textbook, only the Theoretical Price is introduced…….

Even the CFA people are probably a little scared of writing exam questions on the Theoretical Price.

The people sitting for the exam aren’t elementary schoolers — there are actual industry pros taking it,

(hey, do you guys even know anything about bonds? The exam had a Theoretical Price question — that’s an error. Fix it. I’m the final boss of the bond market, wanna go?)

OK I’m exaggerating a bit, but dealing with that kind of pushback would be a headache…. so even so, if it shows up on the exam, it’s almost certainly going to show up as Full Price, right….

But then again, only Theoretical Price is introduced in the textbook. lolololololololol what am I supposed to do with thatlololololololololololol

So for exam prep on this:

First, calculate with Full Price and see if it matches one of the answer choices — if it does, circle it and move on,

if it’s not in the choices? Then calculate with Theoretical Price and check if that answer lands in the choices.

This feels like the right play for us exam candidates. (sigh) heh heh heh

Last thing — let me quickly hit Matrix Pricing and wrap it up.

Matrix Pricing is, when you’re valuing a bond that doesn’t trade much or hasn’t even been issued yet,

“inferring it from the YTM of other bonds with similar characteristics and using that for valuation” — that’s the idea.

A simple example goes like this:

I need to value a bond with a 3-year maturity right now,

but the only bonds in the market with similar characteristics are 2-year and 5-year —

in that case, we just use “Linear Interpolation” to roughly guess the YTM for the 3-year bond and roll with that.

Doing it this way looks theoretically fine, but……

the inescapable problem is you end up Over-Pricing it.

Normally when you’re doing valuation, if there’s Liquidity Risk, you fold that into the discount factor so the present value gets knocked down harder,

but just mashing numbers together like this means you’re slapping onto a bond of unknown (or nonexistent) liquidity

the yield information of a bond that actually has liquidity —

so whether you realize it or not, the starting point of the calculation itself is already overvalued!!! heh heh heh

Originally written in Korean on my Naver blog (2021-12). Translated to English for gdpark.blog.