Yield Spread

A casual breakdown of yield spreads — what G-spread and I-spread actually mean, why swap rates beat LIBOR as the private-sector risk-free rate, and how traders decide if a bond is cheap or rich.

Last time we looked at the Yield Curve, so this time let’s talk about the Yield Spread.

Actually — the full, proper story of Yield Spread is a Level 2 thing, and I did debate going all-in and tossing in my Level 2 notes too. But I’m writing this based on Level 1, so I’ll just keep it at the Level 1 level. heh

OK so. Bond prices — people often don’t quote them in currency units like $, they quote them in %. And every bond is basically the risk-free rate baked in (obviously you need the risk-free rate — otherwise why on earth would I buy something that isn’t a government bond??), plus “how much spread are you layering on top? (how many bp of spread?)”

In other words, all the bond-chatter in the world could collapse into: “what’s the spread on it?”

The idea is: ignore everything else, look only at the spread being layered on, and from that decide whether the thing is expensive or cheap.

Then the question becomes — what do we use as the risk-free rate (the Benchmark Bond)? Easy pick: government bonds. Specifically, the on-the-run issue. The spread layered on top of that is what people mean by the G-spread. (G for Government.)

But… hold on. Who here can actually borrow money at the government-bond rate? Government bonds are the price of the government borrowing. For someone like me, a random individual — or even a corporation — using government bonds as the risk-free rate is kind of weird.

So what should we use as the risk-free rate in the private sector??????????

Something convenient-looking would be LIBOR. But LIBOR is also kind of a problem, lol. It’s the rate at which the 8 major London banks lend to each other. And those 8 banks are themselves insanely, ridiculously high-quality…………..

So rather than using LIBOR straight up as the private-sector risk-free rate, what people do is use the swap rate on LIBOR as the private-sector risk-free rate. And the spread measured against that is called the I-Spread. (I for Interpolated.)

OK so let me tell you what a Swap rate is.

Swap rate: “what fixed % would you swap your floating rate for?”

A: “I’ve got a bond paying LIBOR — anyone want to swap rates with me?” B: “I’ve got a 3% fixed bond. Let’s swap. You get 3% fixed, I’ll take the floating.” C: “I’ve got a 4% fixed bond. Let’s swap. You get 4% fixed, I’ll take the floating.” D: “I’ve got a 5% fixed bond, but nah, I’m not swapping. Mine’s better.”

Roughly like that — the fixed rate the market settles on as fair in exchange for a floating rate is the Swap rate.

(The actual Pricing and Valuation of a Swap gets covered in detail in Derivatives, so don’t stress about it.)

(Figuring out that x% — as in, “current LIBOR trades cleanly for x% fixed!” — that’s what’s called Pricing a Swap.)

Anyway. Take that Swap rate and treat it as the private-sector risk-free rate, and the question “how many extra % of spread is embedded relative to this?” gives you the I-spread. For Level 1 I think knowing it at that level is totally fine.

The whole point of studying spreads, by the way, is basically this:

Getting rid of the lazy idea that YTM going up automatically means the thing got riskier.

(Sounds obvious when you say it out loud… heh)

OK — all of that was literally just warmup. Now we get to the real main event.

Zero Volatility Spread & Option Adjusted Spread.

Let’s start with the Zero Volatility Spread.

Every spread we talked about above was YTM-based. And YTM’s big advantage is that it collapses everything into a single geometric-mean-ish number. But the downside is — that number is extracted with the enormous assumption that the term structure of interest rates is completely ignored. In other words, it assumes the term structure is flat.

(Let me draw it out one more time.)

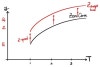

The thing that answers “how much spread is embedded relative to government bonds?” without leaning on the flat-term-structure assumption — that’s exactly the Zero Volatility Spread. The Z-Spread.

In a setup like this, the G-Spread is trivially 12% + x = 13.5%, so x = 1.5%.

Then — what exactly!!!!! is the Z-Spread computed from?!!!!! (What’s the calculation that dodges the flat-term-structure assumption as hard as possible?)

We think of it like this.

Where:

TS: Treasury Spot ZS: Zero Volatility Spread

The idea is: look at how much spread sits on top of the spot rate, using this setup —

One thing that falls out is:

And in diagram form, it’s this:

This means a Parallel Shift of the Yield Curve!

But… what if this bond is Callable?

Remember — we saw earlier that a bond identical in every way except that it’s callable is going to be priced cheaper, by exactly the amount of call risk the bondholder is sitting on, right?

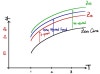

If you take the logic above and apply it straight to a Callable Bond, the ZS comes out larger than it “should” —

So we borrow the Option Adjusted Yield logic we saw earlier and bring it in here:

We already covered the Option Adjusted idea before, so this shouldn’t feel all that painful.

Anyway — since this (as α) carries over identically, and it’s still a Parallel Shift concept, if we draw the whole thing on one diagram:

The thing you actually need for the exam, I’m pretty sure, is just the ordering of the spreads.

(Z-spread < option adjusted < non-adjusted)

Still — if you keep the logic above in your head, there’s no real reason to get confused. heh heh heh

For reference (you don’t need to know this), as for why of all the names in the world it’s called “Zero Volatility” —

The details live in Level 2, so I think it’s fine to just go “ah, so it was computed assuming zero volatility” and move on.

OK — last thing, for real.

For both the Z-Spread and the Option Adjusted Spread, I kept hammering on Parallel Shift.

And you might be tempted to retroactively apply that to the G-spread we saw earlier — so, just to kill that temptation —

What we emphasized about the G-spread and I-Spread was not parallel shift — it was the fact that those assume the Term Structure is flat!!!!!

These need to be held apart in your head!!!

Aaaaand with that — everyone everyeveryeveryeveryeveryev everyone everyoneyoneyoneyone

Happy New Year~~~~

Happy New Year, everyone~

Originally written in Korean on my Naver blog (2021-12). Translated to English for gdpark.blog.