Price Risk, Reinvestment Risk, and Duration

YTM secretly assumes you reinvest every coupon at YTM itself — and that hidden assumption is exactly where price risk and reinvestment risk come from.

When you calculate the YTM of a bond, the thing you really have to keep in the back of your mind is:

YTM is secretly assuming that every intermediate cash flow — every coupon — is getting reinvested, continuously, at YTM itself.

I’ve been beating this drum over and over, right?

Let me go through it one more time before we start this section.

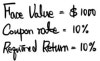

Say a bond is issued under these conditions.

Coupon rate equals the required rate of return here, so this would’ve been a par issue.

Let’s say maturity is 2 years.

So think about it with me.

For $1,000 to earn an average of 10% per year,

the principal would have to become $1,210 at the end — that’s what “10% per year on average” actually means. But

if you just hold the bond and do nothing — the red cash flows —

you come up short of 10% per year. The only way the average-10%-per-year math actually works is if interest on interest gets added in,

which is another way of saying: the bond price and the YTM you blindly calculate

are computed under the assumption that those intermediate cash flows keep getting reinvested at YTM —

the assumption that the money keeps rolling by being reinvested into the exact same bond over and over.

You feel it now, right????

So YTM — the ex-ante yield, the yield you measure before —

might not match the ex-post annualized holding period return you actually see in your account after maturity…..

that’s the whole point.

(Why do it this way? I’ve honestly never heard a clean explanation,

but my guess is…..

someone probably tried to write a formula that computes the real return with interest-on-interest stripped out, and it’s technically doable, but it got absurdly messy.

So I suspect this is just the simplest approach that keeps the whole thing tractable… heh)

OK OK OK OK OK.

So then —

what is price risk, and what is reinvestment risk?

It’s exactly the risk tied to the thing I was just ranting about.

It’s the risk that when you actually get one of those intermediate cash flows, there’s no bond out there giving you the same return anymore!!!

In other words, it’s the risk that rates drop hard in the middle of you holding a bond to maturity.

Huh? But if rates drop, doesn’t my bond price go up, so I make a capital gain?

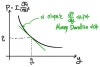

Ohhh ho, let’s visualize this tradeoff.

If market rates suddenly spike right after you buy a bond,

sure, you can take each coupon and reinvest it at the higher rate, so reinvestment income goes up —

but all the cash flows waaaay~~~ out in the future get discounted at that higher rate too, and the bond’s price takes a way bigger hit.

In this setup, if you sold at T=3,

the price-decline hit was larger,

so it more than wiped out the bump in reinvestment income.

But

if you’d held longer and sold later,

the reinvestment income effect dominates instead and it more than offsets the price decline…..

so one effect dominates on this side, the other dominates on that side,

and if you have an engineering brain, you immediately go:

“Right, so — at what point do they exactly cancel out?!!!”

That point is what’s called Macaulay duration.

(Honestly, this is such a good explanation. In undergrad I learned Macaulay duration as a “time average” concept,

but here it’s framed as the center of gravity, and I love that.

I’ll come back to the center-of-gravity picture in a sec.)

https://blog.naver.com/gdpresent/220718454071

Duration, Modified Duration [ My Study of Basic Investment Theory #16 ] People have been curious since ancient times, they say. “Hey!! Can people’s required return just be neatly the bank’s interest… blog.naver.com

(The duration I met back in undergrad.)

OK so now let’s actually get into duration.

Up there we saw Macaulay duration as “the holding period at which the changes from price risk and reinvestment risk become equal.”

If you visualize that, it turns out to be the center of gravity of the present values of the bond’s cash flows.

(Because duration is computed as a geometric probability — a weighted average of the intermediate cash flows against the total cash flow — go look at that undergrad-level duration material.)

(An “average” is a sum of weighted averages, and geometrically that’s just the center of gravity.)

This is exactly why the Macaulay duration of a zero-coupon bond equals its maturity, by the way.

When each PV shifts ever so slightly as $y$ nudges,

if your fulcrum sits at Macaulay duration, the whole thing stays balanced — it doesn’t tip around wildly even with those little movements.

But why only explain the concept without giving the actual formula?

Here you go!

The formula for Macaulay duration is this.

(Derivation is in the image above.)

But as everyone knows, duration isn’t just Macaulay duration —

there are a bunch of other flavors of duration, so I’ll walk through them one by one.

Let me rephrase the question:

“When the market’s $y$ moves a little, how much does the bond price change, in %?”

How sensitively does the bond price react to changes in market rates?

The answer to that one is modified duration.

Let me throw the formula up first,

Wait — this expression is hiding inside Macaulay duration too???

Both are absolute values, so the sign is basically (+), more or less.

An engineer’s instinct is “just do $dp/dy$, why bother with $(dp/p)/dy$ and make it complicated?”

— I had the same thought — but the numerator is $(dp/p)$ because we’re asking about a percentage change.

When a 1,000-won item goes up by 100 won, $100/1000 = 10\%$,

we say it went up 10% — and in the same way, we actually use $\Delta x / x$ all the time in daily life too.

The % change in $x$ per tiny change in some other factor $y$ — written as a formula,

it’s (% change in $x$)/$\Delta y$,

and “change after taking the log” is this percentage change.

Using that relationship and writing it in terms of $\Delta$,

and this is also exactly why differentiating with respect to logs is so important.

Yeah yeah yeah enough with the % change stuff — what about just “how much does the bond price itself change?”

You can write a formula for that too!!!!

The duration built for people who want that is called money duration.

Too much landed on your head at once, right?!

Let me organize it with a picture.

The differentiation you’d happily accept from high school calculus — that’s money duration.

The one converted into % change — that’s modified duration.

So visually, it looks like this.

Strictly speaking it’s a little off, but I simplified a bit for intuition’s sake, cut me some slack :-)

One last thing —

because a bond’s price follows a convex curve,

$\Delta P$ on the way up and $\Delta P$ on the way down, for the same $\Delta y$, aren’t equal.

You can differentiate forward or backward (forward difference, backward difference),

and under the logic of “don’t just go forward, don’t just go backward — take the average of the two (central difference),”

we get one more: approximate modified duration.

What this book calls approximate modified duration

is what most places elsewhere call effective duration, but…..

so then what does this book mean by effective duration…

Looking at $\Delta P$ caused by $\Delta \text{YTM}$ works fine when you’re only dealing with straight bonds,

but once you stretch out to structured bonds — callables, ABS, etc. — thinking in $\Delta \text{YTM}$ gets weird,

and in that world it’s more meaningful to look at price sensitivity driven by $\Delta$ in the risk-free rate rather than YTM.

So the book defines $\Delta \text{risk-free rate} \to \Delta P / P$ as effective duration.

(Ugh, CFA, would it kill you to just go with the mainstream convention;;; annoying!!!!)

Anyway, the whole reason we bother computing approximate modified duration

is to shrink the gap between our estimate and the real number,

but even so, even so, there’s always going to be some gap between an estimate and reality, right?

But!!!!!

There is a case where approximate modified duration is genuinely meaningful.

Specifically, for a callable bond with a large assumed $\Delta \text{YTM}$ —

and the reason becomes obvious the instant you draw the price-yield curve of a callable.

This kind of thing feels like it’s gonna show up as an answer choice, doesn’t it?!?!?!?!

Feels like something we absolutely have to lock in before moving on!!! heh heh heh

Honestly, while writing all this I’ve been mixing $dx$ and $\Delta x$…..

because mathematically, $dx$ is the correct thing to write,

but in the real world, what the heck would $dx$ even mean….. it’s not a real thing, so really we should be writing everything with $\Delta x$.

In the real world, finance moves discretely in bp!

So there’s always going to be a gap between the formula and reality.

And exams love to bait you with exactly that gap.

“The bond price — if you estimate it using modified duration, you always under-price relative to the true price” ☞ correct!

“The change in bond price — if you estimate it using modified duration, you always over-estimate relative to the true change” ☞ wrong!

Easy to see once you look at the graph.

(✓Careful! The y-axis unit is %! It’s a rate of change, a rate!)

The modified-duration estimate is the red arrow, the actual rate of change is the blue arrow, and just eyeballing it, the estimate

And the formula for making that estimate is

One more term to pick up before we move on.

There’s a thing called PVBP — price value of a basis point.

Just file this as: it’s the $\Delta P$ you get when you pin $\Delta y$ at exactly 1bp!

I was thinking of cutting it off here, but let’s just push through….. this post is long….. heh anyway, keep going!

So up to this point we’ve walked through a bunch of flavors of duration,

but the truth is, duration is only really appropriate as a bond-price-risk tool under the premise that the yield curve moves in a parallel shift……

That’s the baseline assumption: “what if all YTMs rise by 1% uniformly?????” — that one.

But come on, nobody running a portfolio holds only bonds with one single remaining maturity.

They’re holding bonds with many, many different remaining maturities in the same portfolio…..

And inside that portfolio, the YTM movements of 1Y, 2Y, 3Y,….. are all different from each other.

Which means the sensitivity is all different depending on the remaining maturity.

So… the duration of a bond portfolio……

what on earth do you do about this………….

For this kind of situation, we use something called key rate duration.

At our level, just understand it loosely as: “when any one rate moves, how does my bond portfolio respond?” and move on.

(The rule for which rate counts as a key rate for your portfolio is Level 2 stuff.)

So at our current level, the limitation of portfolio duration can probably be summed up like this.

Say there’s a portfolio made of 2 bonds,

OK OK, real last bit now!

- When all other conditions are equal between two bonds,

there are 3 arguments of a bond that affect interest rate risk.

What we learned above: we use modified duration as the measure of interest rate risk,

and now we’re going to summarize what affects modified duration — 3 things.

If maturity is long, the window over which rate risk can play out is naturally longer, so exposure to risk goes up — that’s the idea.

If a lot of coupon is being paid out, cash is drip drip dripping into your hands, so principal recovery happens fast. That’s the angle.

Just look at the price-yield curve — at low $y$, the slope is absurdly steep, right???? That’s what this one is saying.

And if you jam all of that into a single picture, it was this picture, remember?!?!

Picture the interest rate shock as kicking the base of that tree — BANG!!! — once,

and ask: “which tree (which bond with which promised cash flow) sways harder (has the bigger modified duration)?”

But if an engineering person sees this, they’re going to go:

Hey man, you’re saying duration like it’s some grand thing, but isn’t that just

a first-order derivative?

So you could differentiate twice and look at the rate of change of that slope itself, and three times, four times, and on and on, right?

Why stop at the once-differentiated “duration”?

Wouldn’t you at least differentiate twice?????

And that’s exactly what convexity is.

Convexity is affected by the exact same things as duration, so let me just lump everything together, tabulate it, and move on.

So in fact, computing the change in bond price using only the first derivative —

— versus using up to the second derivative —

— but… this is literally just the Taylor-series-expanded approximation pushed out one more layer to second order, isn’t it…..?

It’s just plugging that straight in…. feels like a waste to explain the whole thing again….

So let’s leave it at this level and move on!!!!!!!!!!!!! heh heh heh heh heh heh

When convexity shows up on a problem, let’s just make a pact not to fat-finger the formula! heh heh heh

We said a convex price-yield curve is a shape that favors the investor, right?

Because price goes up steeply / and goes down gently?

So if a put feature is tacked on — which layers even more favorability onto the investor — does that favorability show up in the convexity too??????

Since we’re here, let’s also get straight what happens to duration when a call or put is attached.

Not a hard concept, honestly. A callable has a ceiling on price appreciation, rigged in favor of the issuer,

and a putable has essentially a floor on price, rigged in favor of the investor,

so

Two more small things and then we’re out of here.

Yield volatility

This whole section has been about estimating the rate of price change —

in the end we’ve been leaning on exactly this formula,

but there’s volatility lurking in there too…

The thing is…. there’s actually a term structure in the volatility of rate changes as well… what we call the base rate refers to the 7-day repo rate, and when you touch the base rate, the rate shock generally propagates short-term ⇒ medium-term ⇒ long-term. In other words, the shorter the maturity, the larger the yield volatility, apparently.

One more picture to remember before we move on!

Duration gap: the difference between a bond’s Macaulay duration and the investor’s investment horizon is called the duration gap, and how you set this gap is what tells you whether you’re playing defense / or offense.

Originally written in Korean on my Naver blog (2022-01). Translated to English for gdpark.blog.