Forward Pricing

A casual walkthrough of forward pricing for zero coupon bonds — showing how today's spot rates imply a locked-in future price, and why realized rates rarely match what we expected.

Feels like I’m basically re-running the Implied forward rate stuff I already covered before… honestly I wanted to just skip this whole part.

But it’s in the book, so — let’s (once again) take a quick peek.

At the current point $T=0$, all kinds of zero coupon rates are floating around out there in the market.

And I mentioned that the forward rate you compute from those spot rates is what we call the implied forward rate.

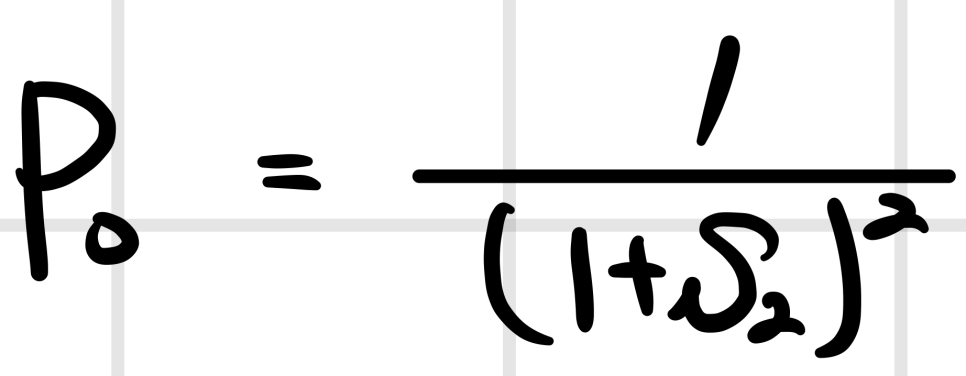

So at $T=0$, a 2-year zero coupon bond with $1 face value is going for

That’s the price it’s trading at, right?

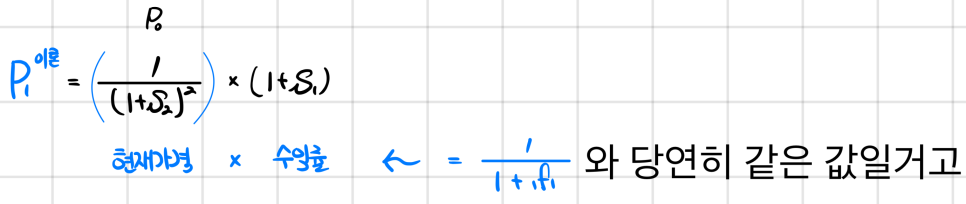

Now if you promise today to sell that same bond one year from now — what price would be the rational one to lock in?

The price below is exactly that rational locked-in number — the Market Fair Value.

And honestly… that’s the entire Forward Pricing chapter.

But OK — when $T=1$ actually rolls around, is the 1-year yield as of $T=1$ —

let’s call it $s_1'$ — going to match the $_1f_1$ we expected (computed) back in the past??

Obviously not. Market rates don’t sit still.

There’d be trades happening between people who think $s_1'$ will end up higher than the $_1f_1$ implied at $t=0$, and people betting it’ll come in lower.

Now let’s look at the same thing but just stretch the timeline a bit:

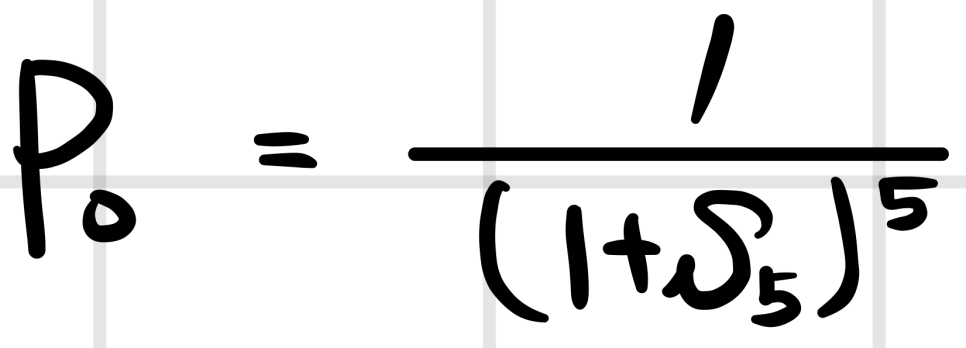

At the current point $T=0$, a zero coupon bond with a 5-year maturity

is trading at this price.

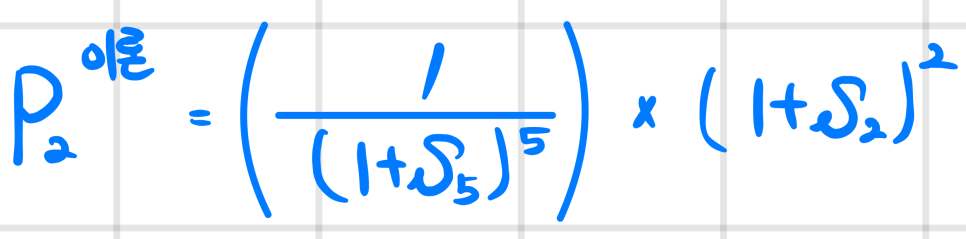

If you enter a contract (forward) to buy/sell this bond at $T=2$,

the Market Fair Value comes out to

That’s all it’s saying.

Forward Pricing has, like… genuinely nothing to it. T_T

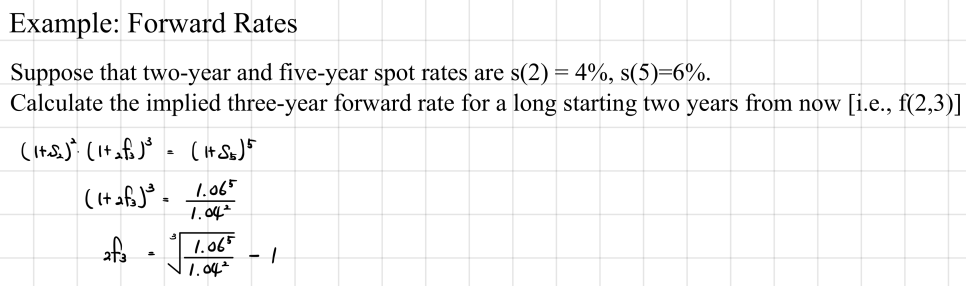

The Forward Rate Model

OK, this time — instead of the Forward Pricing we just did, we’re talking about measuring the “Rate” itself.

And in the book it’s written out with this kind of formula:

But if we just slap it on a timeline and rewrite it in our own notation,

Wait — it’s literally the same thing! The only difference is we’re writing it in terms of yield instead of price. Done!

Originally written in Korean on my Naver blog (2024-11). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.