Swap Rate Curve

Breaking down what swap rates actually are, why the swap curve matters as a benchmark, and how it stacks up against government bond yield curves.

First things first — let’s nail down what “swap rate” actually means.

Oh wait, I’ve studied this before, so I already kinda know~

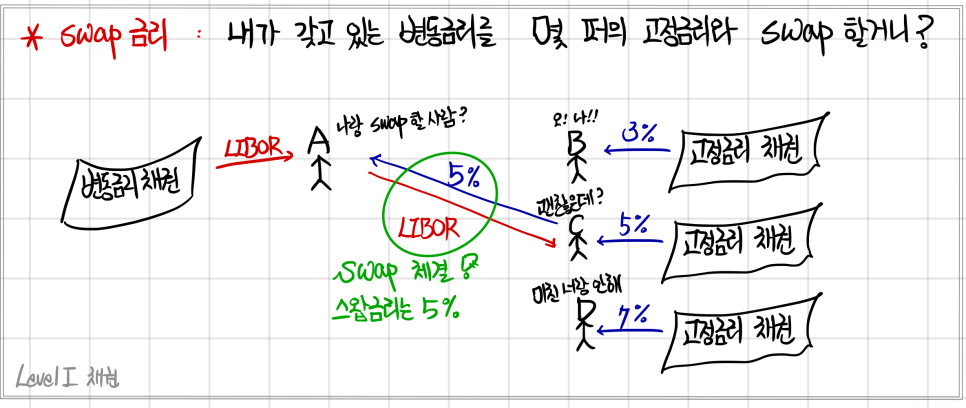

So when you swap a floating rate for a fixed rate, the fixed rate side — as in, “how much fixed rate do I have to pay in exchange for getting the floating rate?” — that number is the swap rate.

To be precise, the swap rate should really be called the swap fixed rate. And when the floating side is LIBOR, the whole thing has a name: a plain vanilla interest rate swap.

But hold on — interest rates are just %s. You can’t swap a percentage with a percentage. That alone makes no sense. To actually transact, you need money — a notional amount, a nominal principal. Now it makes sense: you’re exchanging the dollar amount that corresponds to X% fixed and the dollar amount that corresponds to Y% floating.

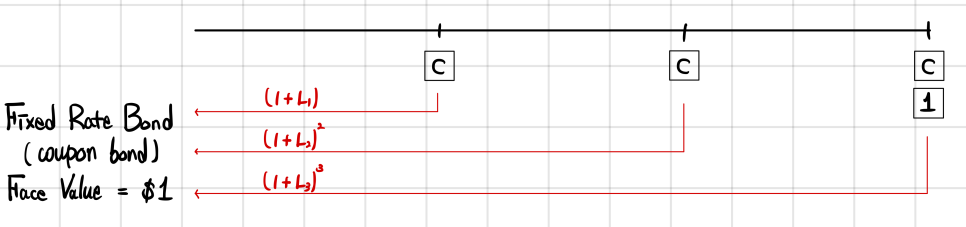

The simplest possible setup: two people each holding a 3-year bond, Annual Pay.

Person A is receiving a floating rate annually. Person B is holding a plain coupon bond (fixed rate), collecting coupons.

(Same face value, same credit quality on both bonds.)

Now if these two swap bonds — boom, the coupon rate IS the Swap Rate!! (the 3-year one)

But was that swap a fair exchange??

If it was fair, then the market price of the floating rate bond and the market price of the coupon bond had to be equal at the moment of the swap. (You handed over equally-priced securities — that’s literally what “fair” means here.)

OK, so now if we have a swap rate for each n-year maturity, we can plot them out. That’s the swap curve.

And the swap curve plays a huge role as a benchmark.

When you hear “benchmark,” the first thing that probably pops into your head is government bonds. But — government bonds are how a government raises money. That’s a government rate, not really a private-sector rate.

The risk-free rate that actually represents the private sector? That’s more appropriately the swap rate. And the collection of those across maturities is the swap curve!!!!

Why market participants prefer the swap rate curve over the government bond yield curve as a benchmark:

1. Swap rates reflect the credit risk of commercial banks, not the credit risk of governments.

2. The swap market isn’t regulated by any government, which makes swap rates across different countries more directly comparable. (Government bond curves bake in sovereign risk that’s unique to each country.)

3. The swap curve usually has quotes at lots of maturities, while the US Treasury curve only has on-the-run issues trading at a handful of maturities.

OK so — how do we actually compute this swap rate?

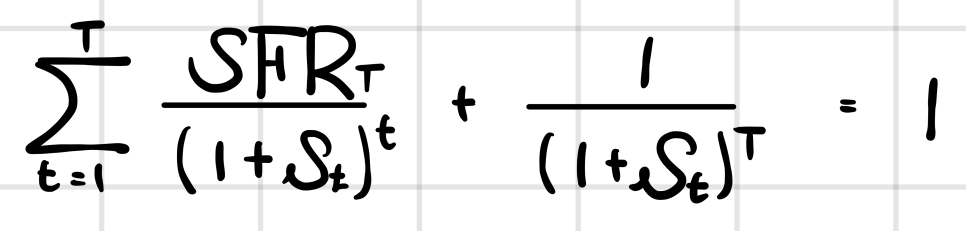

The book writes it like this, and we’re gonna derive what this formula actually means~

(Honestly, you do SFR a ton in Derivatives, so if you studied that first… you can probably skip ahead, heh.)

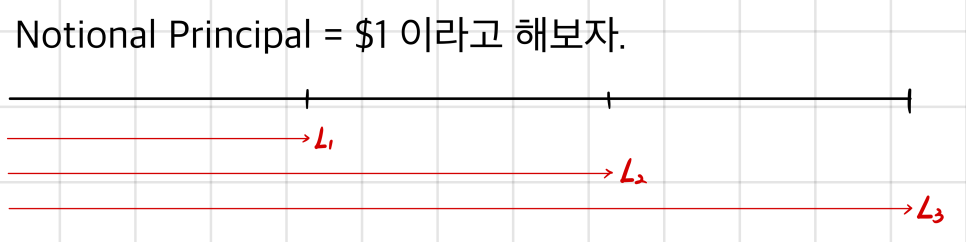

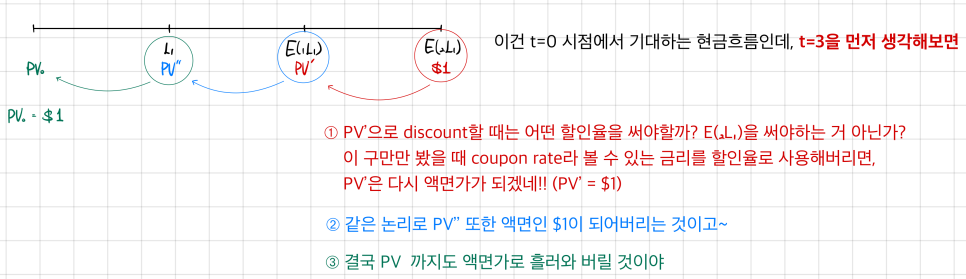

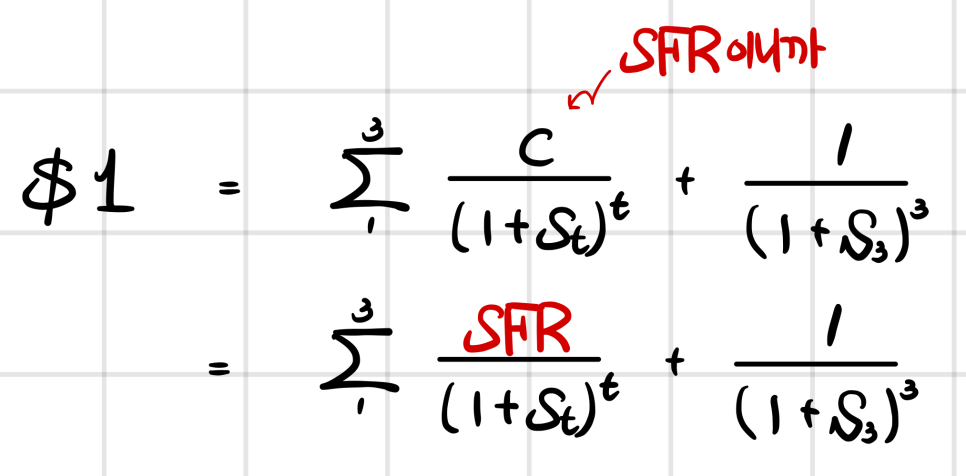

Say the LIBOR spot rates at $t=0$ look like this. Under these conditions, suppose you pick up a 3-year LIBOR floating rate bond at $t=0$. Then~

So: “when the reset date of a floating rate bond rolls around, the price of the bond $\Rightarrow$ exactly equals face value!”

Yeah, that checks out.

Now, a swap is exchanging a floating rate bond like that for a fixed rate bond. And for the trade to be fair, the prices of the two bonds themselves have to match — like we said.

Assume the coupon bond on the other side of the swap has the same credit quality as the floating rate bond. What discount rate do we use to drag those cash flows back to $t=0$ and get the PV?

We just use the LIBOR spot rates, right~?

OK, so given that, what coupon rate does this fixed rate bond need so that it can be swapped fairly with the floating rate bond?

Phrased that way, the question is basically: “given today’s LIBOR spot, what’s the appropriate coupon rate for the swap??”

And the coupon rate that drops out is exactly the number we’ll use as the swap rate — which, again, is what we called the swap fixed rate (SFR)~

So in this example:

The SFR that makes this equation hold IS the appropriate swap rate given the current LIBOR spot!

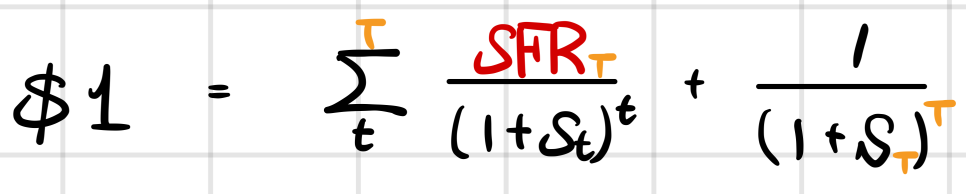

This example used 3 years, but since we can write the SFR for any maturity in that same form, for a $T$-year maturity:

We can pull out the general formula for $\text{SFR}_T$ — the $T$-year SFR!

You can clean this up further, and in problems where LIBOR spot is just handed to you as 3%, 4%, 5%, … in a row, it’s actually faster to just rewrite everything on the right side as present value factors and crunch it that way.

Anyway, this exact content shows up again in Derivatives, and we’ll dig into it more there — so it’s totally fine to aim for full understanding when we hit it the second time! heh

Originally written in Korean on my Naver blog (2024-11). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.