Spread Measures

A been-here-done-this rundown of swap spread, I-spread (yes, with that annoying linear interpolation), and Z-spread — basically Level 1 déjà vu, but let's power through it.

Not boring at all, right? …uh, wait — it IS boring. T_T Because Chapter 1 is basically just a Level 1 rerun…

Let’s just power through a little. T_T

Even I’m bored writing this… just hanging on by a thread here…. T_T

This is stuff I studied back in Level 1, and here it comes again….

Whatever…

➀ Swap Spread:

the amount by which the swap rate exceeds the yield on a government bond of the same maturity.

And since the private-sector “risk-free” rate is going to be higher than the public-sector risk-free rate, this thing comes out positive~

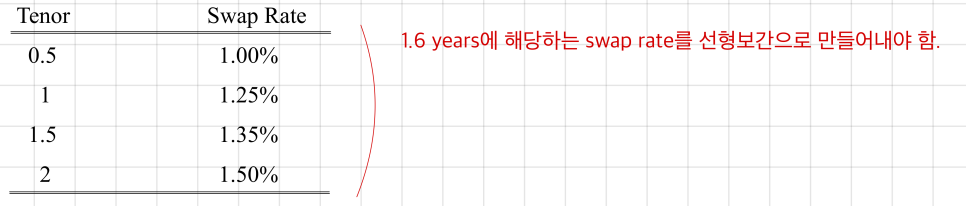

➁ I-Spread:

the I-spread for a credit risky bond is the amount by which the yield on the risky bond exceeds the swap rate for the same maturity.

So you can think of the I-spread as: how much riskier is this corporate bond compared to the swap rate?

Then why the “I” — as in linear interpolation?

It’s because in the swap market, maturities usually come standardized — 6 months, 12 months, that kind of thing.

But my bond? Its maturity probably doesn’t line up with any of those nice round numbers.

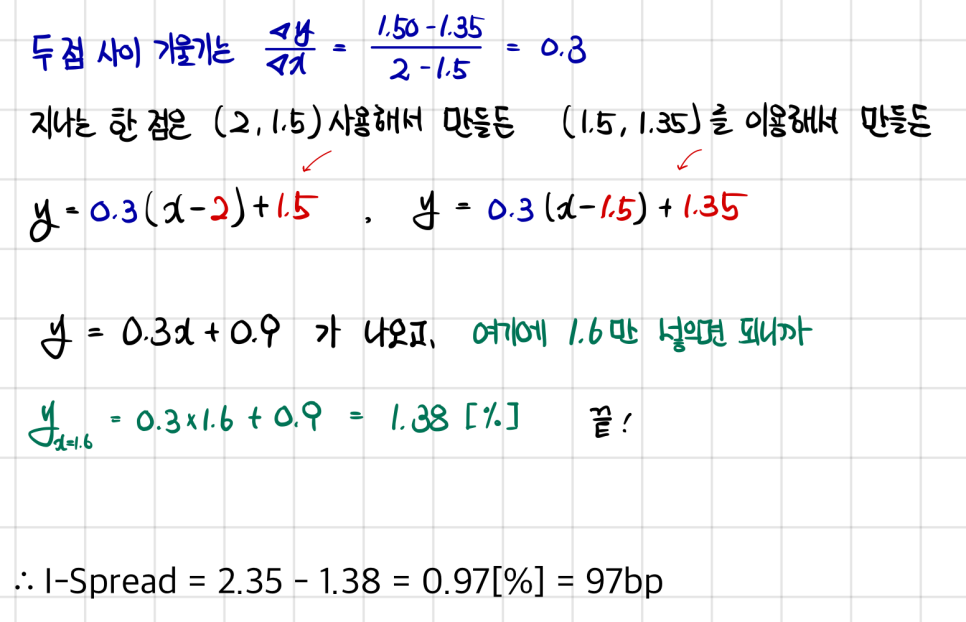

So at that point, you grab the swap rate by linear interpolation between the two nearest standard maturities.

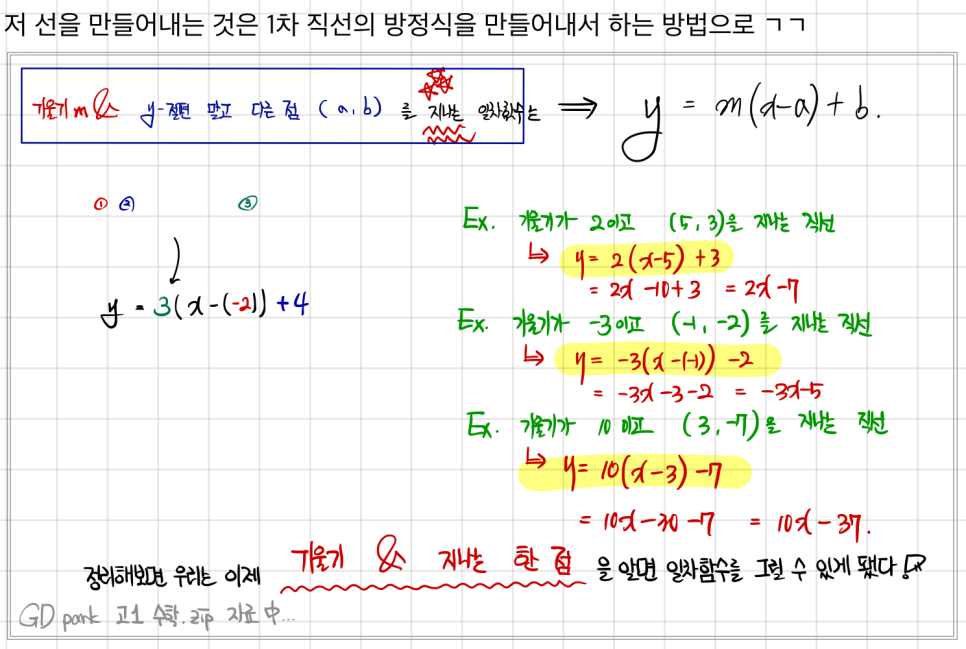

Now, how do you actually crank out that linear equation….

I’ve still got materials lying around from when I was teaching middle/high school math lol

You can just solve it with that.

So when you plug it in,

(

By the way — I’ve got friends who actually manage bonds for a living, and whenever we grab a coffee and chat,

they tell me this interpolation thing is a complete headache.

You have to interpolate, sure, but not in some lazy linear way like this…….

The moment you start digging into interpolation methods, apparently there are just so, so many approaches…..

Anyway lol the on-the-run issue always has to be the benchmark, but since it doesn’t cover every single maturity neatly in a row,

it gets really tricky, they say. heh heh heh

)

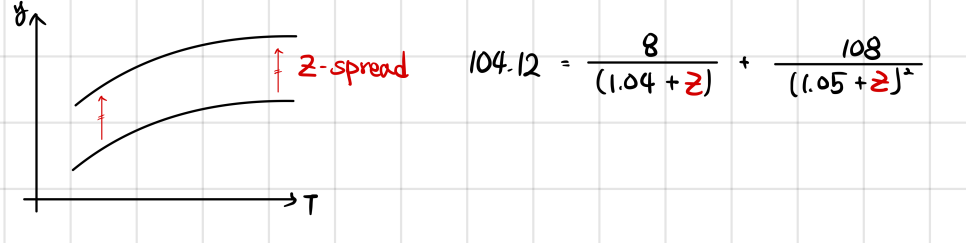

➂ Z-Spread: the spread that,

when added to every spot rate on the default-free spot curve,

makes the present value of a bond’s cash flows equal to the bond’s market price.

The “zero volatility” in Z-spread? It’s referring to the assumption of zero interest rate volatility. (because, you know, it assumes zero volatility.)

So the Z-spread is not appropriate for valuing bonds with embedded options;

without any interest rate volatility, options are meaningless.

Anyway, what’s actually going on here —

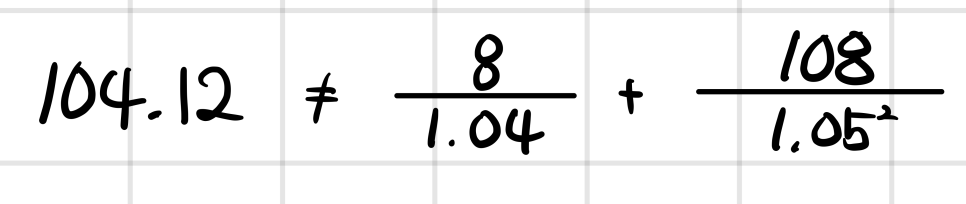

the current spot curve is $s_1 = 4\%$, $s_2 = 5\%$,

and some corporate bond with $c = 8\%$ (2Y, Par = 100) is trading at 104.12.

But the thing is — the price it’s actually trading at doesn’t come out to that.

How much do we have to shift the current spot curve in parallel so the price lines up with that corporate bond?

That shift amount — that’s the Z-spread!

Now, the actual spot curve, in real life, those spot rates fluctuate by some amount.

They do move, and long-term bonds fluctuate more than short-term ones.

It’s called the Zero Volatility Spread because we’re assuming that volatility is flat-out zero!

But here’s the thing — an option isn’t a product that bets on the level of price, it’s a product that bets on the level of volatility.

Volatility is the lifeblood of an option. So evaluating a bond with an embedded option using Z-spread, which assumes that to be zero? → Yeah, there was a note saying remember that this is kinda a problem~

➃ TED Spread:

conceptually, the TED spread is the amount by which the interest rate on loans between banks

(formally, three-month LIBOR) exceeds the interest rate on short-term US government debt (three-month T-bill).

The T in TED is the T from T-bill, and ED is apparently the ticker for Eurodollar futures.

The Eurodollar interest rate, you can basically just think of as LIBOR,

because it’s the rate banks use when they lend dollars to each other — so LIBOR is what gets plugged in.

* Eurodollar: dollars deposited in Western Europe (especially London, Zurich)

And what’s the gap between the interbank rate and the country’s risk-free rate actually telling you? Simply put: the “(credit) Risk of the Banking Industry.”

So a widening TED spread means the Banking Industry just got riskier~

➄ LIBOR-OIS Spread:

the amount by which the LIBOR rate (which carries some credit risk) exceeds the OIS rate (which carries only minimal credit risk).

* OIS (Overnight Indexed Swap): represents interest rate on unsecured over-night lending between banks

OIS is the rate for borrowing money for one day. And honestly, the risk of a bank going under in a single day is basically nothing —

so rather than credit risk, this spread is really telling you about liquidity risk.

(A short-term liquidity risk indicator for the dollar funding market.)

Originally written in Korean on my Naver blog (2024-11). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.