Term Structure Theory

A quick rundown of the theories that explain why the yield curve slopes the way it does — and the sneaky exam traps hiding in each one.

In this section, we look at the theories that try to explain the slope of the spot curve.

It’s not long. It’s not hard.

But the exam questions on this stuff get sneaky, so you really need to nail down the keywords precisely. That kind of section.

i) Unbiased Expectation Theory (a.k.a. Pure Expectation Theory)

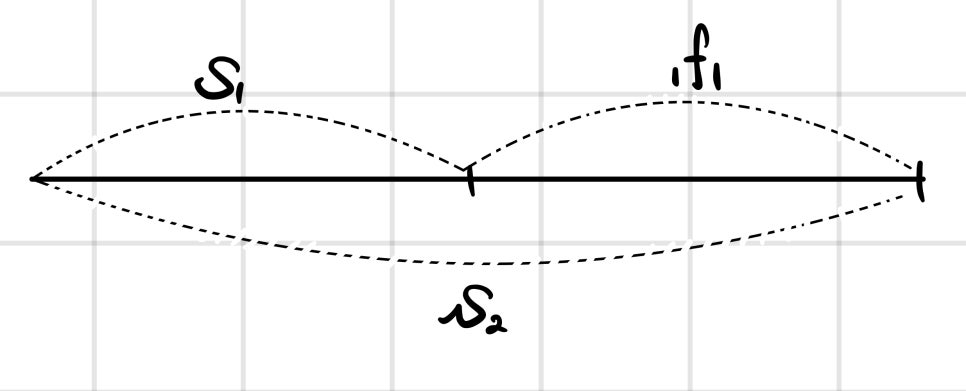

The reason we observe $s_1 < s_2$ in the market — according to this theory — is that people expect next year’s $s_1$ (call it $s_1'$) to equal $_1f_1$, and $_1f_1 > s_2 > s_1$.

That’s it. That’s the whole thing.

(And critically — there’s no premium being demanded in that expectation.)

So in the end: if people predict rates are going up, the curve slopes up. If they predict rates are going down, the curve slopes down.

That’s it. That’s all!

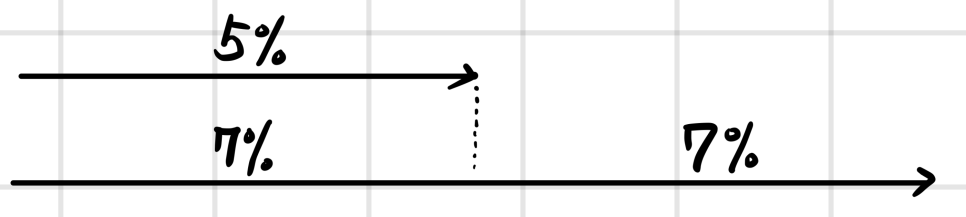

And Pure Expectation Theory assumes investors are Risk Neutral.

Meaning — to them, parking your money in a 1-year instrument at 5% and then rolling it into another 1-year at 9%, vs. locking in a 2-year at 7% twice — those two are completely indifferent. Same same.

ii) Liquidity Preference Theory (⭐️ Apparently this is the one held as the “established” theory)

This one says: nah, people are basically risk averse.

And the reason they demand higher returns over the long term is that locking your money up for 2 years exposes you to more potential interest rate shocks than locking it up for 1 year — so they want a fatter risk premium for going long.

So that’s what gives the curve its upward slope.

Downward sloping? That happens when liquidity preference is so strong it crushes short-term rates way down.

(Notice — under this theory, we don’t actually know whether people think future rates will rise or fall! It’s just: people prefer Liquidity, full stop.)

(* Apparently the exam loves to test you by pitting these two against each other — Pure Expectation vs. Liquidity Preference. Watch out.)

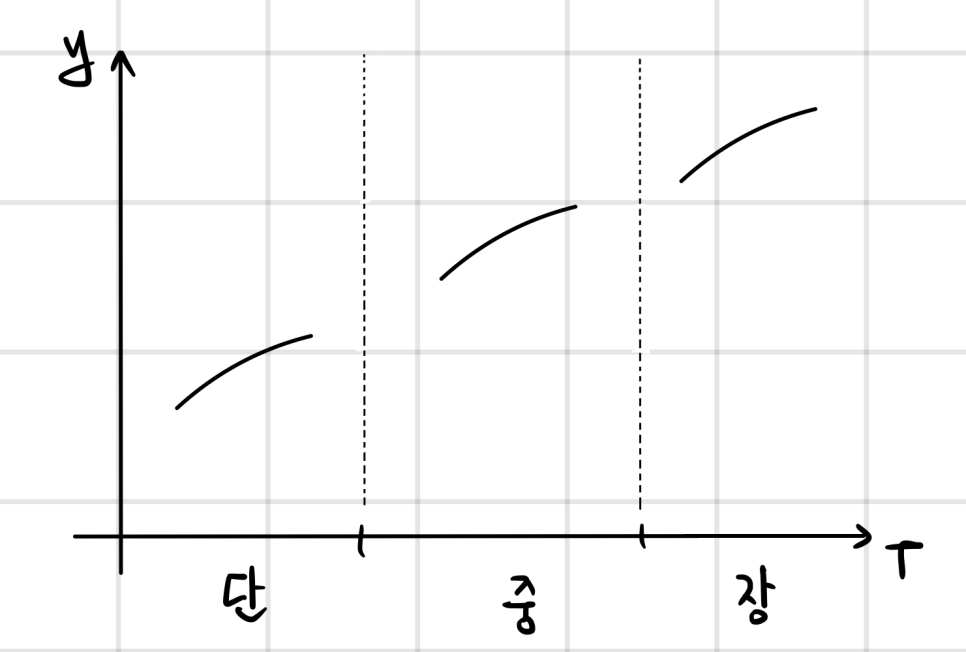

iii) Segmented Market Theory & Preferred Habitat Theory

Pension funds and insurance companies — they want long-term bonds. They don’t really need Liquidity.

Banks — they want short-term bonds. Because for banks, Liquidity is life.

So under this theory, the rate at each maturity is just set by supply and demand within that maturity’s own little market!

Which means, according to this theory, you can totally get a weird-looking rate structure like this and it’s fine.

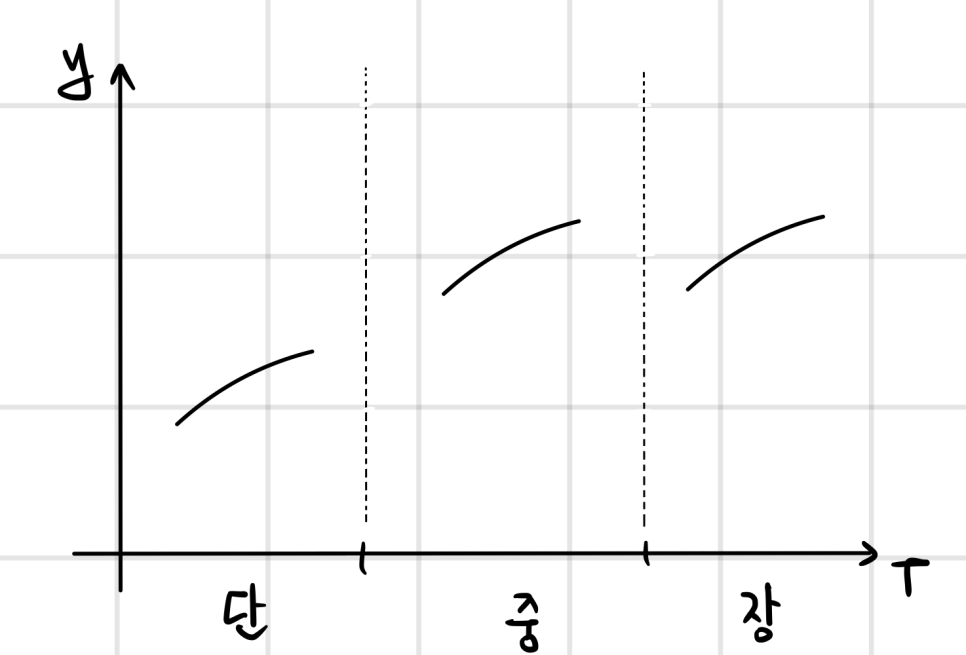

Now if you allow movement between the markets, you get Preferred Habitat Theory — people have their preferred maturity, sure, but if you offer them a juicy enough Premium to abandon ship and migrate to another maturity, they’ll do it. And that migration is what smooths out the Yield Curve.

iv) Local Expectation Theory

This one… isn’t really well-supported. The theoretical foundation is shaky and the whole thing kinda feels like a hodgepodge mashup of the other theories…

Local expectation theory preserves the risk-neutrality assumption only for short holding periods.

Translation: it’s Pure Expectation Theory for the short term, but for long-term bonds, people do demand a Liquidity premium… so… yeah.

Just register that it exists and move on.

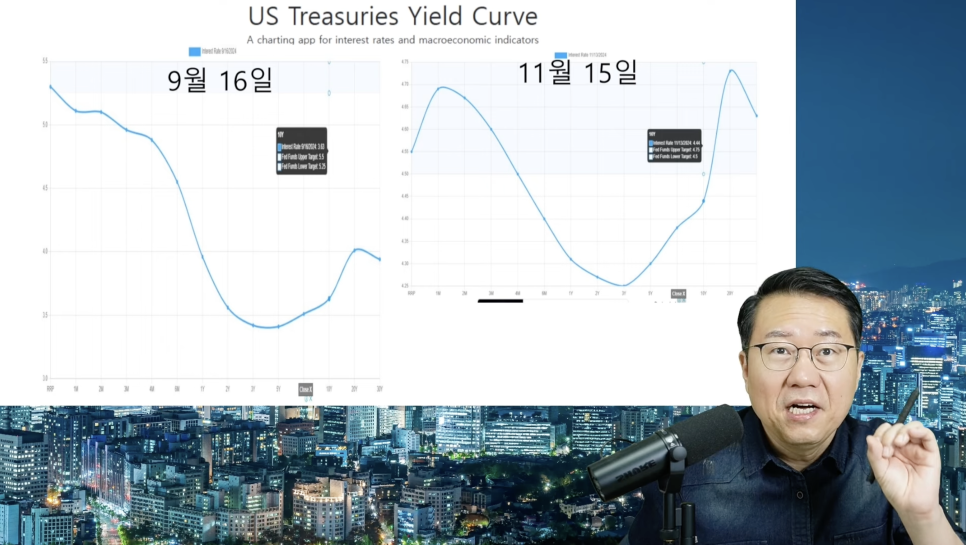

Wait a sec —

As of 2024,

the actual yield curve looks like this hot mess — like what are you even supposed to do with that~~~~

lol lol lol lol lol lol lol lol lol lol lol lol lol

Even when the benchmark rate gets cut, market rates just completely ignore it and march upward — like what are you even supposed to do~~~~

lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol lol

Originally written in Korean on my Naver blog (2024-11). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.