Yield Curve Volatility and Term Premium

Finally wrapping up Chapter 1 — yield curve volatility, term premium, and how the curve twists with expansions, recessions, and flight-to-quality~

Last bit of Chapter 1!!!!!

FIGHTING!!!!!!!!

Level 1 content continues, again, just like before T_T T_T

OK, but in the Level 2 book, Modified Duration gets relabeled as Effective Duration,,

That’s the only thing that changed (and like — ED and Mod Dur are basically the same thing anyway~)

So — short-term bonds tend to have kinda big yield volatility and small Effective Duration,

while long-term bonds tend to have kinda small yield volatility and big Effective Duration.

And in particular, things with embedded options — callables, putables, that kind of thing — have an enormous influence on yield volatility.

Volatility at the long end is thought to be tied to uncertainty about the real economy and inflation, while volatility at the short end reflects monetary policy risk.

Notice that the drivers behind each volatility are totally different~

Bond Risk Premium

Bond risk premium (= term premium = duration premium) is the excess return over the one-year risk-free rate that investors earn for parking in long-term government bonds.

This thing is what’s called a term premium~ that’s literally it.

https://www.hani.co.kr/arti/economy/economy_general/1152373.html

Worst day for the stock market… 235 trillion won in market cap wiped out by ‘fear of R’ ( ☞ Subscribe to Hankyoreh newsletter H:730. Try typing ‘h:730’ in the search bar.) Fear of a US recession spread uncontrollably, causing the domestic stock market to collapse weakly. The KOSPI’s rate of decline was the highest since the 2008 global financial crisis, and the drop was the largest ever. The KOSDAQ index 700 www.hani.co.kr

The terrifying R!!!!!!!!!!

Expansions and recessions

When the economy is expanding, prices start ticking up, and to keep those prices in check, monetary policy gets pulled out,

and what they touch is usually the short-term rate — they crank it up — and at that point long-term rates tend to drift up too. But not by the same amount. And that shows up on the curve like this:

The other direction: when the economy looks a bit rough, rates get cut to give things a kick,

and again it’s the short-term rate that gets touched, and the long-term rate follows down too, but by less.

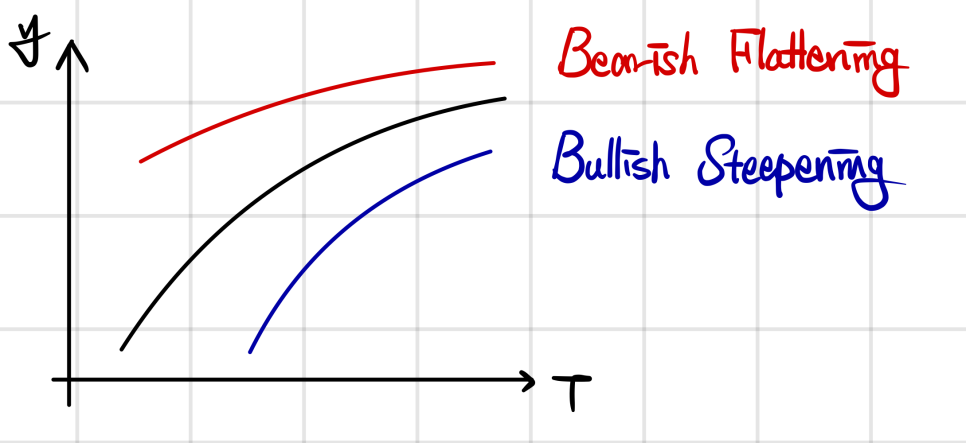

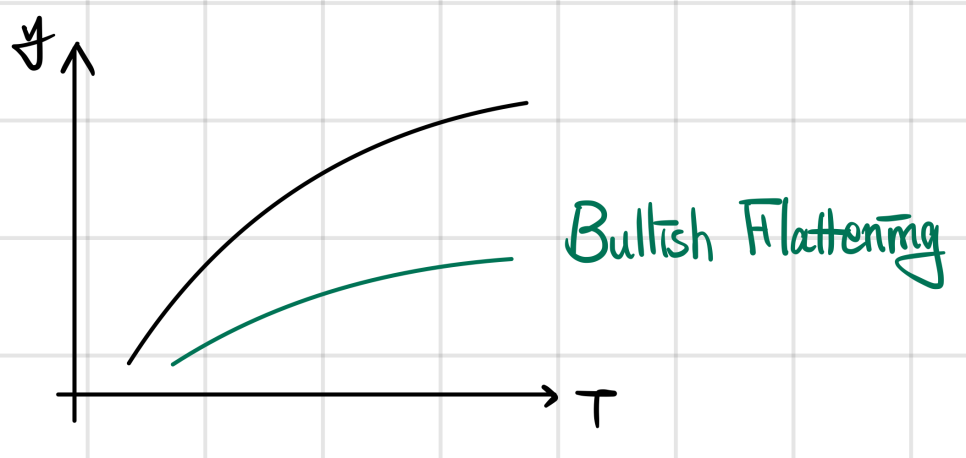

Then there are cases like this.

When companies across the board start looking risky and so on, you get this thing called flight-to-quality — a “safe-haven preference” — where

investors dump all their corporate bonds and pile into the government bond market. So government bond prices rise (and rates fall).

In this kind of situation, investors come in and park at the long end rather than the short end,

so long-term bond rates fall by more.

This kind of move is called Bullish flattening.

(Honestly, if you just memorize that the Bull/Bear label is glued onto the direction of bond prices, you’ll never get tripped up.)

And that’s all of Chapter 1.

Feels like this chapter was honestly more of a Level 1 review than actual Level 2 stuff..

From the next chapter on — the real hell begins!!!!!

Originally written in Korean on my Naver blog (2024-11). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.