Bonds with Embedded Options

A quick rundown of callable vs. putable bonds — who holds the option, why callables are cheaper, and how to back out the embedded option value from the straight bond price.

From this chapter on, we’re basically living inside the interest rate binomial model. Think of it as: how do we actually value Callable / Putable bonds end-to-end? That’s the whole game now.

But before we dive in — yeah I know we already saw this in Level 1, but let’s lock down the terminology first.

Callable Bonds are bonds where the issuer (the side that took the money) gets the right to call the bond back.

The side holding the option is Long Call, and the side that wrote the option (the one who lent the money) is Short Call.

(So for a Callable bond, the issuer is Long Call, and the investor is Short Call.)

And the flavors:

European — one shot at exercise / American — exercise whenever you want / Bermuda — a handful of specific dates,

(apparently most of them get issued Bermuda-style in practice)

A Putable Bond, on the other hand, gives the investor the right to put the bond back at the exercise price.

(So for a putable, the investor is Long Put, and the issuer is Short Put.)

There’s also a cousin (sort of?) of the putable bond called an Extendible Bond. And what’s that…

it’s a bond where the maturity can be extended. And again, the right belongs to the investor!!

OK now think about it from the investor’s side. You’ve got bonds in front of you,

and some of them have callable attached, some have putable attached.

Callable = a clause that’s bad news for the investor. Putable = a clause that’s good news for the investor.

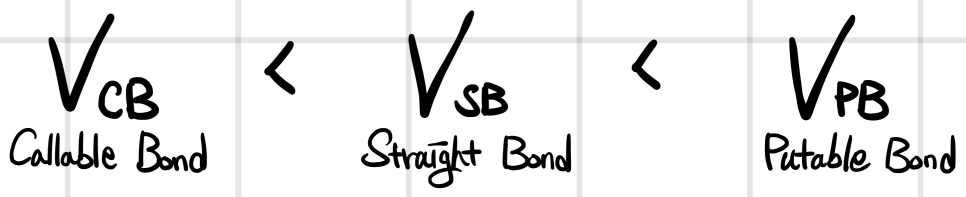

So it stands to reason — Callable should be cheaper, and Putable should be more expensive!!!

Which means we can back out the option’s value from the straight bond!

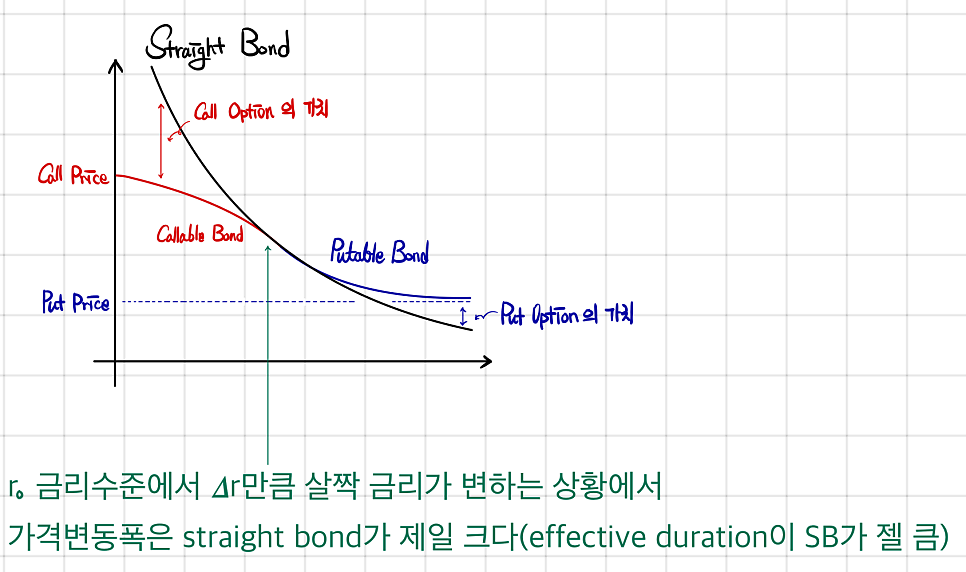

The call premium goes up when YTM goes down.

Because when rates drop and drop and drop, the issuer can just exercise the call, yank all the bonds back, and refinance at the lower rate.

That’s a real risk to the investor — so to compensate, investors demand a fat call premium!!

Honestly, since all of this was already baked into the Level 1 material, it’s pretty manageable~

OK — now let’s get into the actual Level 2 stuff~

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.