Valuing Bonds with Embedded Options, Part 1

We finally put the Binomial Tree Framework to work pricing callable and putable bonds, walking through how cash flows shift at every node as rates move.

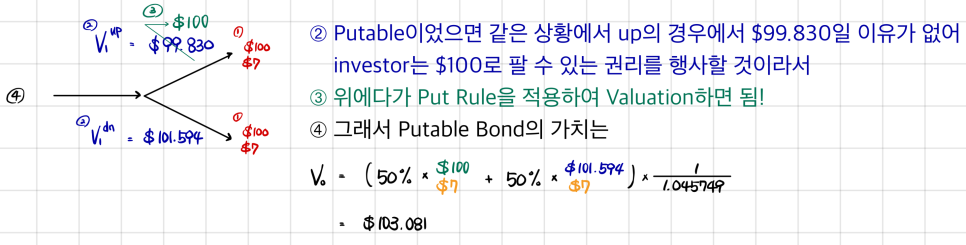

Alright — now we finally get to use the Binomial Tree Framework for the thing we actually built it for:

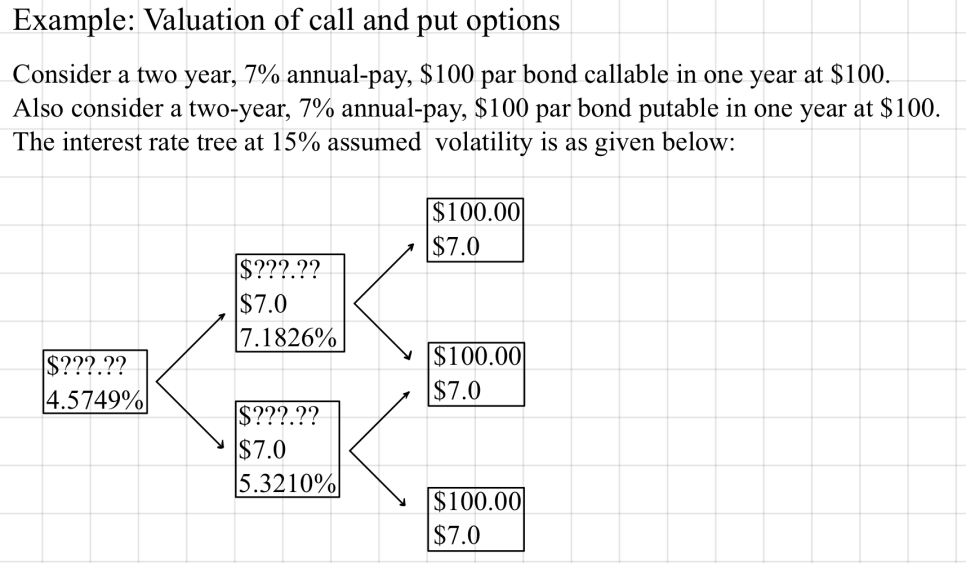

pricing callable and putable bonds!

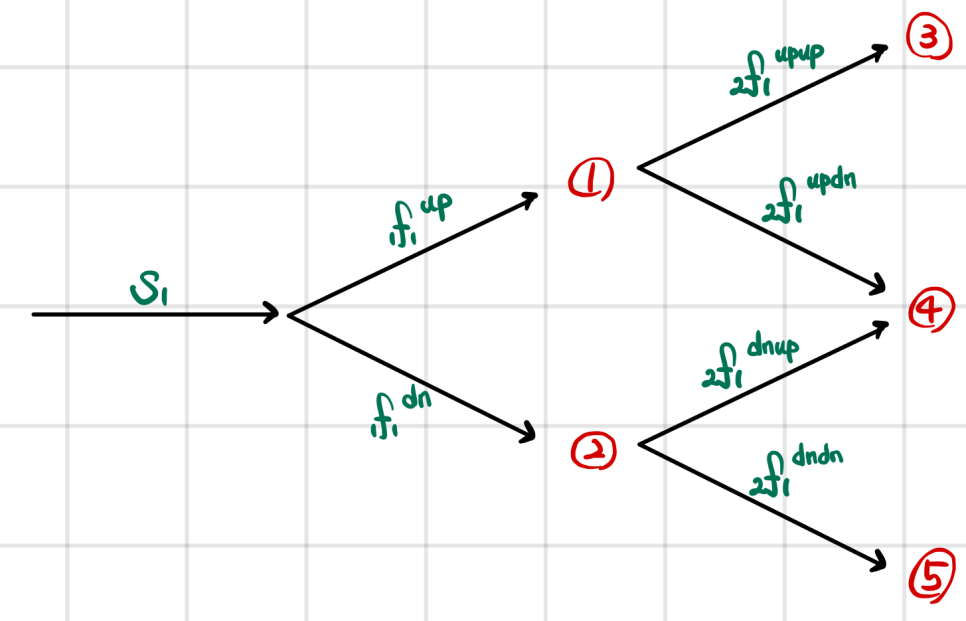

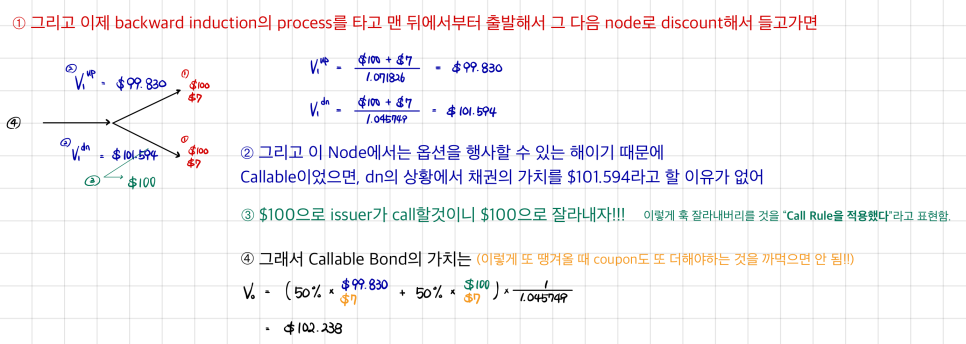

The whole idea is to do the valuation while baking in whether the call/put actually gets exercised as interest rates jiggle up and down in the future.

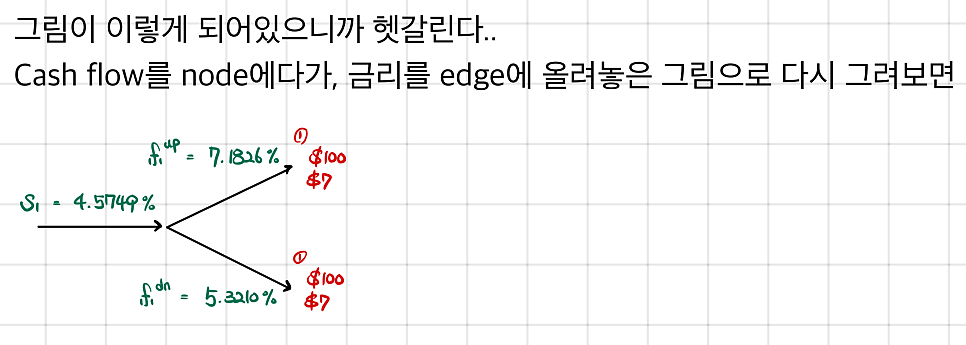

Since the cash flow ends up being different at every node, let’s walk through how the numbers get plugged in.

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.