Interest Rate Volatility, Rate Level, and Yield Curve Changes: Impact on Embedded-Option Bond Values

Here's the breakdown on how volatility, rate levels, and yield curve shape each hit the value of embedded options in callable and putable bonds — exam staples, all three.

The title here is way too long lol, so I shortened it as much as I could in Korean,

but the actual full title is this:

This stuff shows up on the exam all the time, so yeah — this part matters!

➀ Interest Rate Volatility

First things first — the value of an option moves in the same direction as volatility.

Volatility goes up → call or put, doesn’t matter, the value goes up.

Why? Because options aren’t really a bet on where the price lands — they’re a bet on how much it moves. Volatility is the whole game.

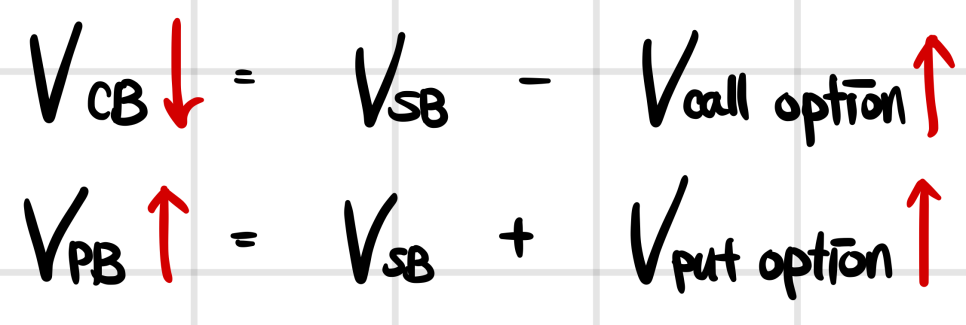

And — really important — don’t mix up the value of the option with the price of the bond that has the option embedded in it. Two different things.

When volatility goes up, any option’s value goes up.

But! The price of a callable bond falls, and the price of a putable bond rises.

(So: option value and callable bond price move in opposite directions / option value and putable bond price move in the same direction.)

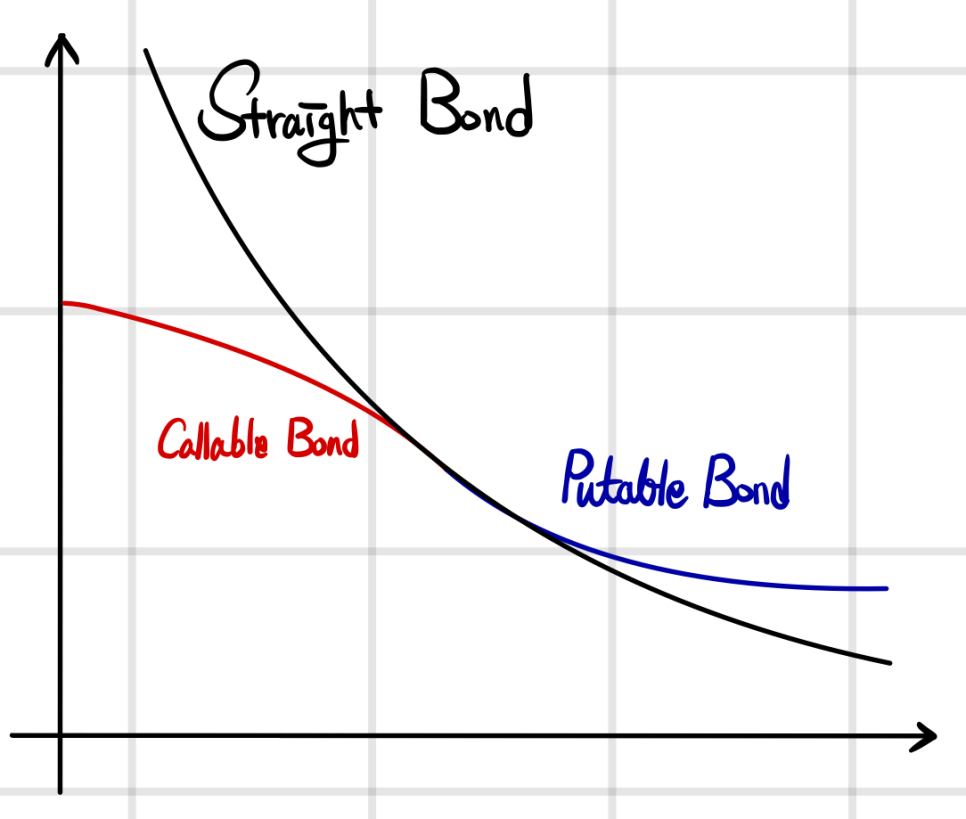

➁ Level of Interest Rate

OK, so what does the level of interest rates actually hit?

It hits the discount rate you use to value the straight bond. That’s it.

So yeah — it’s the same underlying bond, so of course the bond’s value is affected,

but fundamentally? Whether it’s a call or a put, the level of interest rates doesn’t really touch the option itself.

Of course — depending on which way the rate level moves, the size of the value swing can be bigger or smaller!!!

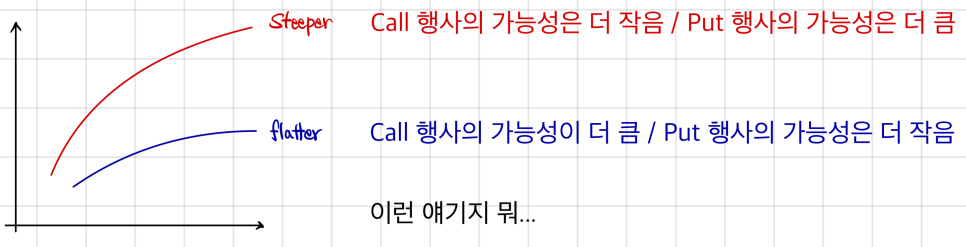

➂ Shape of the Yield Curve

For an upward-sloping yield curve, the slope itself can be… steep, or flat — and this part is about that distinction.

A steep yield curve means the market thinks rates are going to rise — and rise a lot more from here.

A flat one means the market still thinks rates will rise, but slowly, gently.

So — does the shape of the yield curve actually move the value of an option? Yep.

A higher-rate scenario caps the chance of the call option ending up in the money,

so the call option value is lower when the yield curve is upward-sloping.

As that upward-sloping curve flattens out, the call option value goes up.

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.