Option-Adjusted Spread (OAS)

OAS is the constant spread you add to every node of a risk-free binomial tree until your callable bond price matches the market — and spoiler: it has nothing to do with options.

Up to this point, every binomial tree we built and every bond we valued has been risk-free.

Meaning: government bonds.

So what happens when the thing we need to value isn’t a government bond — it’s a corporate bond??

We can’t just reuse the discount rate from the gov-bond tree. We’d need to bump it up juuust a tiny bit, right?

Bump it up to the market price. Bump it up uniformly — every node by the same amount.

What exactly are we bumping up?!?! Don’t get this confused!! We’re bumping up the Risk-free Callable until it hits the market price!!!!

If you mix this up right here, everything below turns into a total mess!!!

And how far do we bump it…

“Until it matches the price that corporate bond is actually trading at!” — that’s how far.

That amount? That’s the Option-Adjusted Spread.

This is apparently super important content, so let’s just transcribe it once before moving on.

So far our backward induction process has relied on the risk-free binomial interest rate tree;

our valuation assumed that the underlying bond was risk-free.

If risk-free rates are used to discount cash flows of a credit risky corporate bond, the calculated value will be too high.

To correct for this, a constant spread must be added to all one-period rates in the tree such that the calculated value equals the market price of the risky bond.

This constant spread is called the Option Adjusted Spread.

In the earlier example,

$$V_{CB} = V_{SB} - V_{CallOption} = \$102.238$$the binomial tree we used to land on that number was risk-free,

so that callable bond price is the Risk-free Callable Bond Price.

If the Risky Callable Bond is lower than $102.238 — say, somewhere around $99 —

we have to add a constant spread to the binomial tree so the result comes out to $99,

and that constant spread that makes everything line up exactly — that’s what we call the OAS.

Now here’s where it gets kinda funny.

The risks embedded in the Option-Adjusted Spread contain literally zero things related to options……

The risks baked into the spread between these two can really only be two things — Default Risk and Liquidity Risk.

(Call risk? Already gone. Stripped out.)

So then why do we even bother talking about OAS…

There’s a whole zoo of risky callable bonds out there.

Say we’ve narrowed it down to ten-or-so risky callables, all under the same conditions.

From the OAS perspective — which one should we buy???

Same conditions across the board, but this one ate up way more OAS than the others??? → That’s the one to buy!!!

Something like that. I think the right way to frame it is: OAS is for comparing corporate bonds against each other.

The OAS computed using the above methodology is the spread implied by the current market price and hence assumes that the bond is priced correctly.

Note that the actual estimation of OAS is largely an iterative process and is beyond the scope of the exam.

OAS is used by analysts in relative valuation; bonds with similar credit risk should have the same OAS.

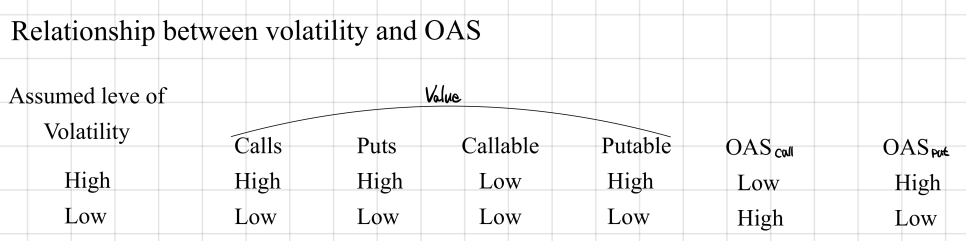

How does interest rate volatility affect OAS?

Spoiler: it affects it enormously!!

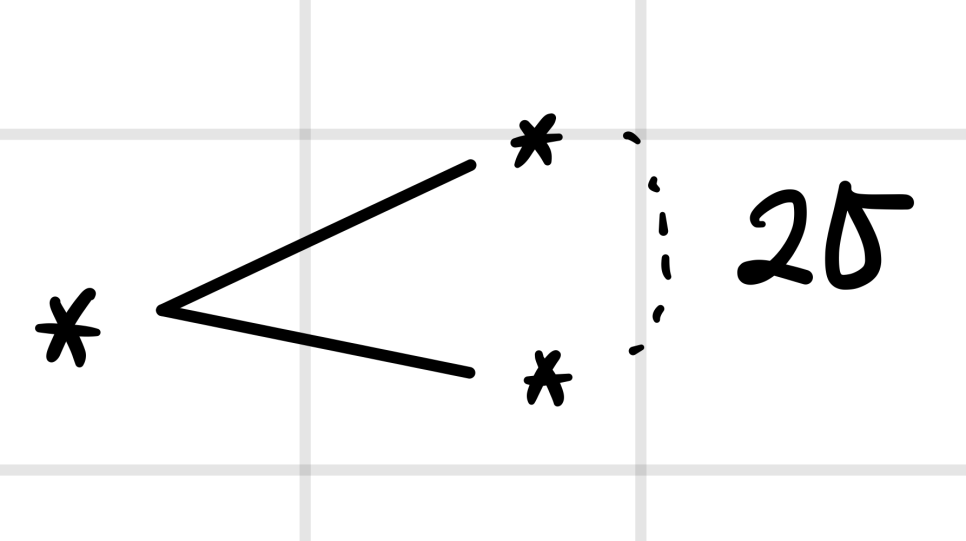

But first — in the binomial tree, interest rate volatility…

…was represented by the angle between the two edges, remember?

So the flow was: design a tree like this → valuate a straight bond → swap in cash flows with the call/put rule applied → valuate the risk-free callable/putable → compare it against the price of the actual credit risky callable bond → there’s a gap (the OAS), and we adjust by exactly that gap until the gap disappears. That’s what we did, yeah?

So somewhere inside this whole process, where is it that we assume interest rate volatility????

It’s right at the start — when we built the tree to calculate the risk-free callable bond, we baked in our own assumed volatility as the angle between the edges.

And from what we covered earlier,

interest rate volatility affected the option value, right?!?!?

Higher volatility → option value goes up → callable bond price gets pushed down!

Which means: higher σ↑ → the OAS of the callable acts in the direction of getting ↓ smaller.

(The risk-free callable price comes down, so the OAS we need in order to match it to the market price also shrinks.)

(Flip it for a putable: bake high volatility into the tree and the (risk-free putable) price goes up,

so the OAS we need to reach the market price gets bigger!!)

Apparently this one shows up on the exam a lot, so lock it in!

One more summary, just to keep the wires from crossing!!

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.