Key Rate Duration (Partial Duration)

A casual walkthrough of duration — modified, effective, and key rate — and why assuming a parallel yield curve shift doesn't always cut it.

OK so the actual main topic for today is Key Rate Duration. That’s the goal.

But before we dive in… let me run through Duration one more time. Yeah, I know, it’s Level 1 stuff — but humor me.

Quick Level 1 refresher first.

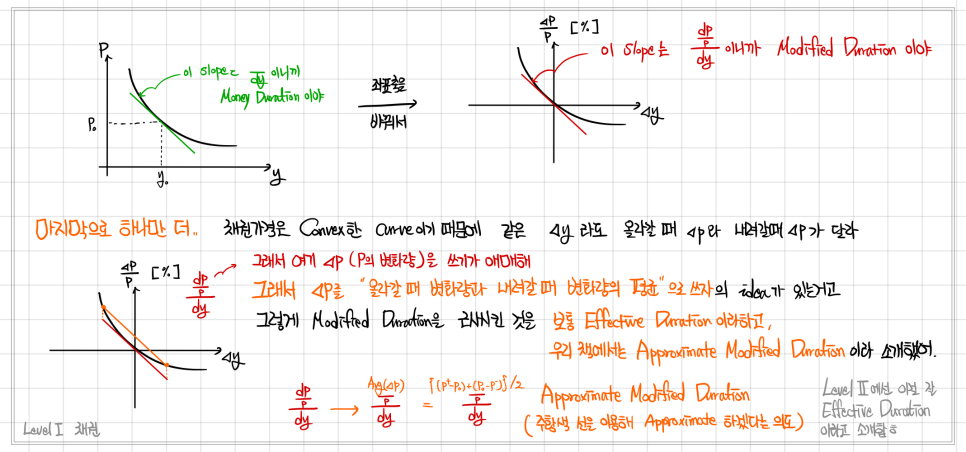

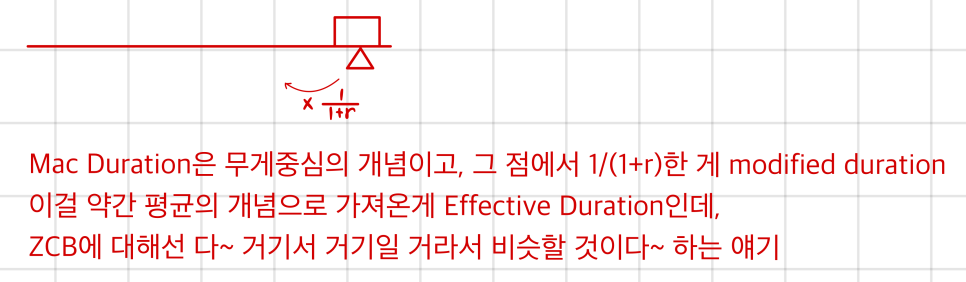

Modified duration: when the level of interest rates wiggles a bit, how sensitively does the bond price wiggle? That’s all it is.

But now that I’m doing Level 2, here’s what jumps out — modified duration straight up did not allow for the possibility that an interest rate change might also change the cash flows themselves. Nope. Cash flows are fixed. Period.

And one more thing — the thing they drilled into me until my ears bled back in Level 1 — it assumes a Parallel Shift of the Yield Curve!!!

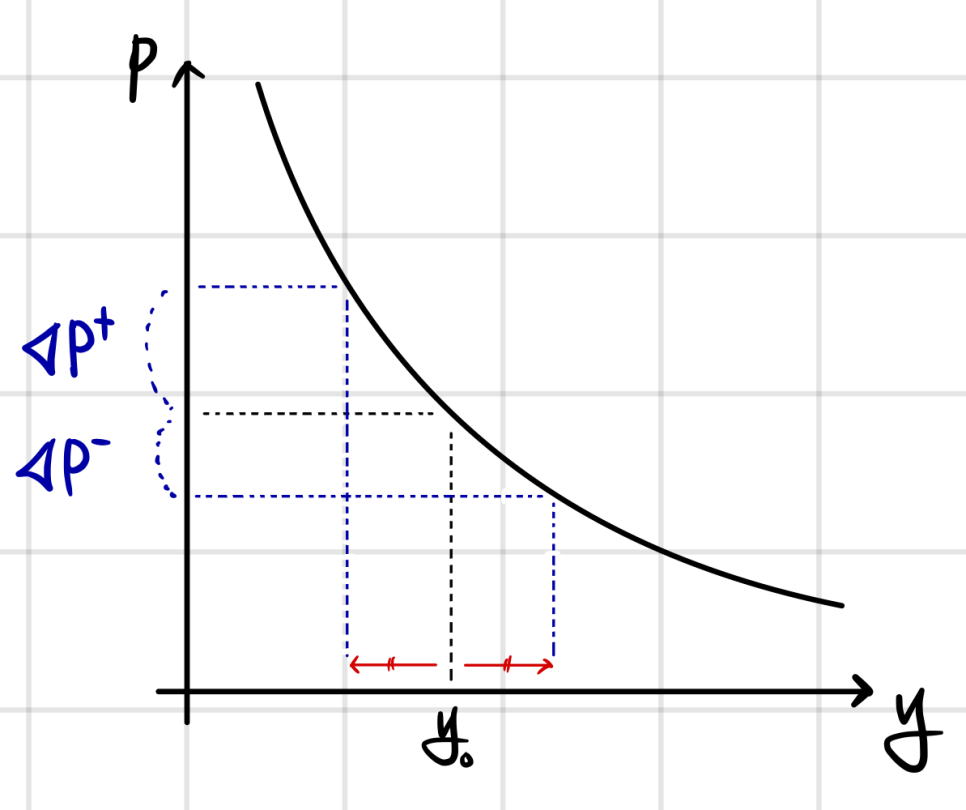

But here’s the thing: how much a bond’s price moves is different when rates go down vs. when rates go up. (Because price is convex in $y$.)

Modified duration kinda smears over that asymmetry. So if you compute duration separately in each direction — once for “rates go up”, once for “rates go down” — that’s called one-side duration. Upside duration / downside duration, broken out.

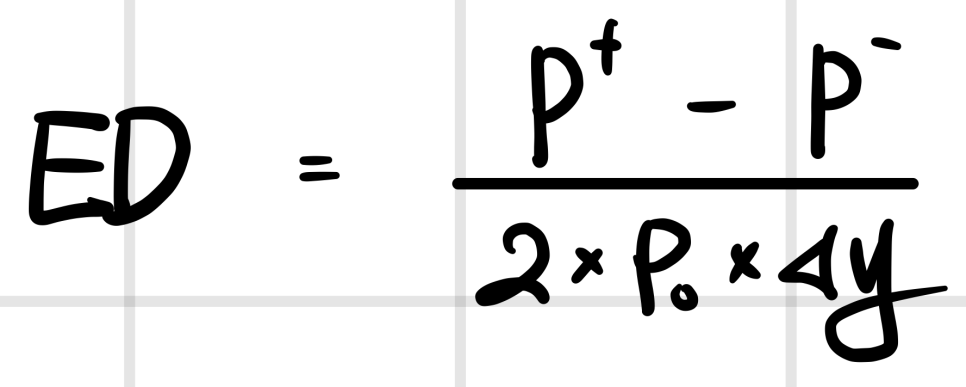

And as we also saw back in Level 1, Effective duration is

which is basically just averaging those one-side durations together.

OK so we’ve been studying sensitivity this whole time, and the core assumptions baked into Duration are:

➀ future cash flows don’t change ➁ the curve shifted in parallel

Now — what if we relax assumption ➀ and let cash flows change? How do we handle that?

Turns out there’s a pretty clean way.

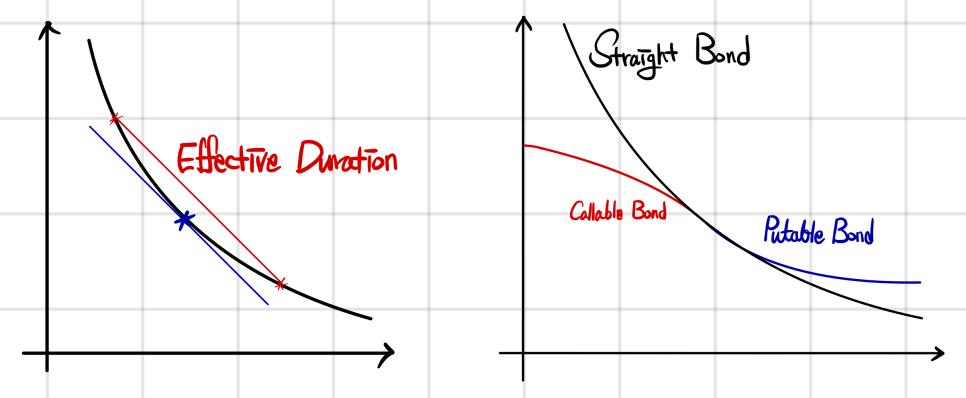

Whether the bond is Callable or Putable, we can price it with a Tree Model or Monte Carlo. And if you look at the formula above, you just plug the Callable/Putable price into $P_+, P_-$ — and boom, you get a Duration that does account for changing cash flows!

I think we can put it like this:

(Effective Duration is essentially “modified duration with assumption ➀ — unchanging cash flows — kinda relaxed”!!)

Honestly… this is also stuff we already saw back in Level 1 Fixed Income…

Because the curvature behavior coming from the cash flows changing has at least some of itself baked into the calculation…!

When you visualize Effective Duration, it looks like this — so whether callable or putable, Duration comes out smaller than for a straight bond!!!

Which is why the book writes it like this:

Both call and put options have the potential to reduce the life of a bond, so the duration of callable and putable bonds will be less than or equal to the duration of their straight counterparts.

- Effective Duration (callable) ≤ Effective Duration (straight) - Effective Duration (putable) ≤ Effective Duration (straight) - Effective Duration (zero-coupon) ≅ Maturity of the bond

- Effective Duration of fixed-rate coupon bond < Maturity of the bond Rule of thumb: scale it at roughly 75% of the maturity.

- Effective Duration of Floater ≅ Time (in years) to next reset Rule of thumb: “duration runs up to the next reset date~”, basically.

Key Rate Duration (Partial Duration)

Like I said, the assumptions baked into duration are: unchanging cash flows / parallel shift — two of them.

For Bonds with Embedded Options, I said Effective Duration is what you get when you sort of relax the unchanging-cash-flows assumption.

And Key Rate Duration, the thing we’re looking at right now, is what you get when you sort of relax the parallel-shift assumption (assumption ➁).

Key rate duration is used to identify the interest rate risk from changes in the shape of the yield curve (shaping risk).

Since the yield curve does not parallel shift, the first thing we need to figure out is — which year’s YTM change is my bond most sensitive to?

The most critical key rates for various types (straight/callable/putable/…) of bonds with different coupons?

OK so — how do we actually calculate it?

The process of computing key rate duration is similar to the process of computing effective duration described earlier, except that instead of shifting the entire benchmark yield curve, only one specific par rate (key rate) is shifted before the price impact is measured.

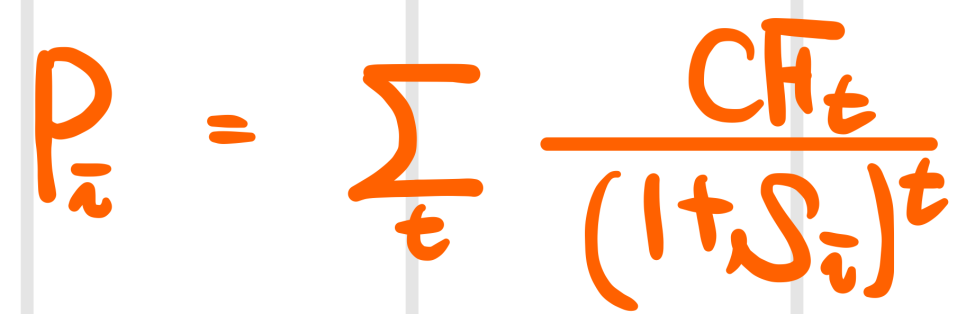

Say I’m running a bond portfolio with maturities 1Y, 2Y, 3Y. The portfolio value keeps moving — why? Because the individual bond values inside keep moving. And each individual bond keeps moving because the $y_i$ that determines each $P_i$ keeps changing.

When you compute each $P_i$, you use the corresponding $y_i$ — i.e., a change in $\text{Par rate}_i$, i.e., a change in $\text{YTM}_i$, is what makes each bond price move!!! (Yeah, super obvious… heh.)

* Apparently this is the only textbook that explains it using par rates — most other books say prices are quoted using spot rates and approach key rates via spots.

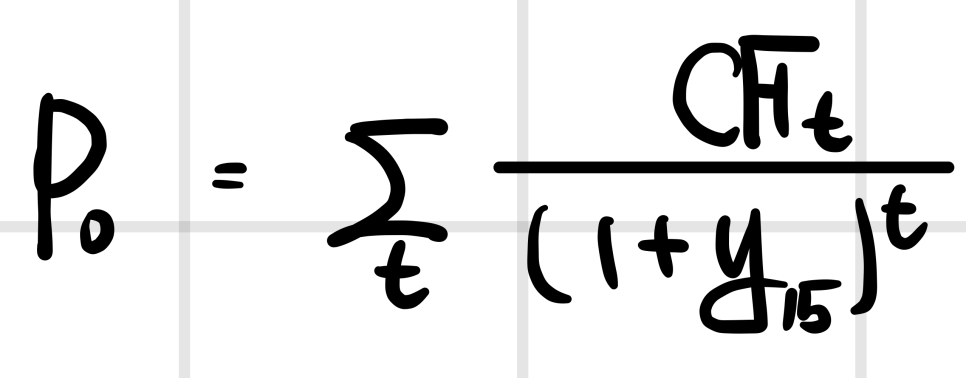

OK~ the point is: bond prices are determined by YTM.

So suppose the market’s required yield right now is 3%, and we’ve got a 15-year bond with coupon rate = 3%, trading at par at $100. The *only* thing driving that $100 price is the 15-year YTM!

That’s the setup. Now let’s look at this.

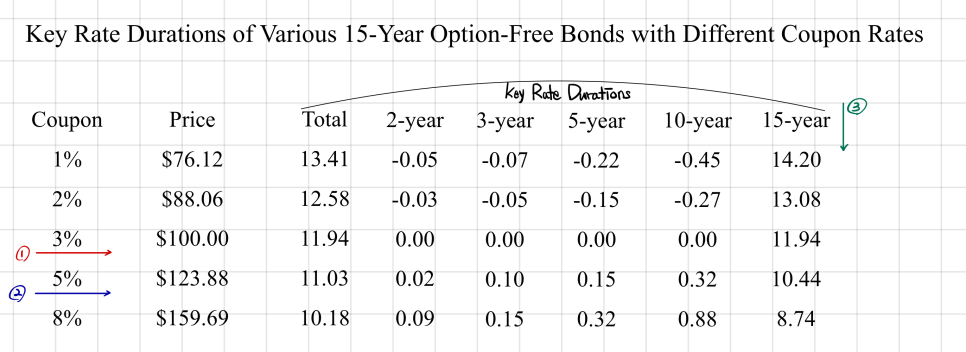

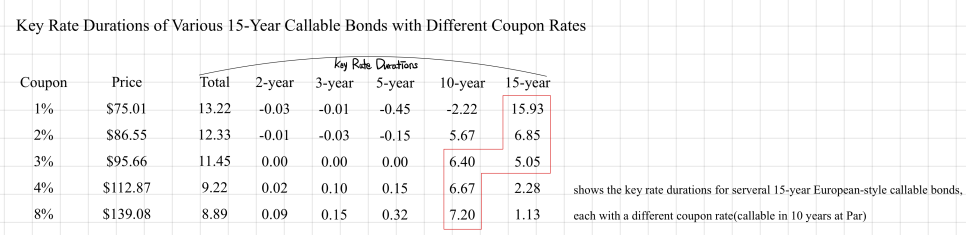

This first table shows: when the world’s required yield is 3%, what prices do 15-year bonds trade at if we vary their coupon rate?

So:

required yield = coupon rate → par bond required yield > coupon rate → discount bond required yield < coupon rate → premium bond

That’s what the table is showing.

Looking in direction ➀ first, it shows the Duration with respect to each of $y_2, y_3, y_5, y_{10}, y_{15}$ — and the Duration for every $y_i$ other than $y_{15}$ is 0.

Why why why why?!?!

Because the other YTMs don’t touch this bond’s price!! So the rate of change of price (sensitivity) with respect to any $y_i$ that isn’t $y_{15}$ is just 0.

Now in direction ➁, right — I get that this one’s trading at a premium because the coupon is above the world’s required yield. But still, the only thing different from the bond we just looked at is its CF. This bond should also not have any $y_i$ other than $y_{15}$ affecting its price, right?

Then why isn’t the duration 0???

What was the whole point of studying Key Rate Duration in the first place?

“The critical key rates for various types of bonds with different coupons?”

Right — so a coupon bond, taken as a whole, does have some sensitivity to $y_i$s other than the one matching its maturity~ That’s roughly the level we can see it at!

And in direction ➂, the influence of $\Delta y_{15}$ on the Total Duration of each bond is overwhelming!!!

Whatever coupon rate it’s paying, the key rate is $y_{15}$!! Because the maturity is 15 years!!!

Let’s pin this down:

For an Option-Free (Straight) Bond, the Key Rate is $y_T$ matching the maturity, regardless of the coupon rate!!

Now let’s look at bonds with embedded options.

First, the price — compared to the Straight Bond from before, it’s a bit cheaper. Reason being: a Callable Bond = Straight Bond − Call Value.

And between a high-coupon bond and a low-coupon bond, which one is the issuer more likely to call?

→ Obviously the high-coupon one. Higher probability of getting called.

If rates are low at the 10-year call date, the issuer just calls it and refinances at the lower rate. So — low coupon → likely held a long time / high coupon → very likely to die at year 10..

OK so now looking at the table —

For a discount bond with a low coupon, the key rate looks like it should be the 15-year. Among all the key rate durations, the one at 15-year is overwhelming.

But for a bond with a high coupon (above the market required yield), the rate corresponding to the 10-year callable point looks like the key rate.

That’s the stuff highlighted in red in the table!

To summarize, the Key Rate Duration of a Callable Bond, based on the required yield, is:

- if coupon rate is low → corresponds to maturity (because it’ll probably go to maturity?) - if coupon rate is high → the call-possible point

- if coupon rate is in between → roughly the same either way

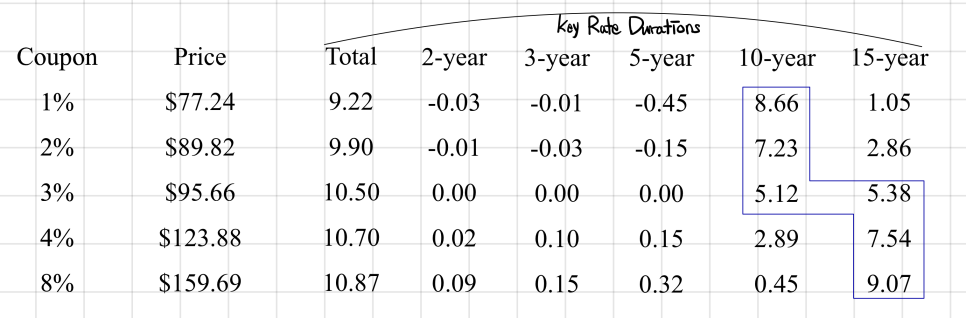

We should also look at Putable, but honestly… it’s just the mirror image of callable. Let’s just flag it in the table and move on~

(The numbers printed in the book are wrong, by the way. Since it’s a put, it should normally be more expensive than the SB, but it isn’t..)

Anyway — the key point of this Key Rate Duration section is not that you need to know how to calculate each of those individually. It’s whether you can read this table.

So put more weight on interpreting the table than on the numbers!

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.