Capped and Floored Floaters

Capped floaters put a ceiling on the coupon (great for the issuer), floored floaters set a minimum (great for you), and you value both by tweaking a binomial tree and working backward.

A floater is just an FRN — a floating rate note (a variable rate bond).

A capped floater pays a floating coupon, but with an upper limit on the coupon rate. A floored one has a lower limit.

So a cap is good for the issuer.

A floor is good for the investor.

Which means a capped floater is going to be cheaper than one without a cap,

and a floored floater is going to be more expensive than one without a floor. Make sense?

$$\text{Value of a capped floater} = \text{value of a straight floater} - \text{value of the embedded cap}$$$$\text{Value of a floored floater} = \text{value of a straight floater} + \text{value of the embedded floor}$$OK so — how do we actually value these?!

→ Same trick as before. Draw a binomial tree, do Backward Induction. That’s it!!

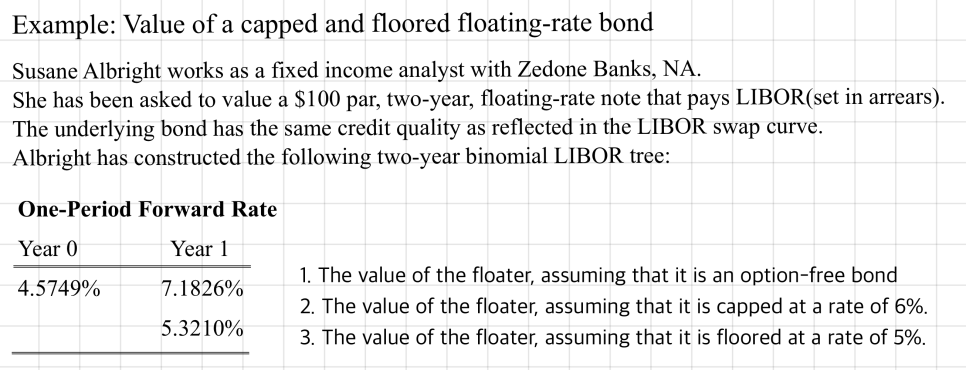

First, the option-free one is just an FRN, so it trades at par. Easy.

The capped floater — even when the rate jumps to 7.1826% in Year 1, the coupon is capped at 6%. That’s all it can pay. Doesn’t matter how high rates go.

The floored one has a lower limit, so when the rate is above that floor, nothing happens — it just pays the floating rate like normal. But when the rate dips below the floor, the coupon gets pulled up to the floor level.

So you tweak each node in the tree according to those rules, and then just Backward Induct from the end back to the front~

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.