Convertible Bonds

A casual breakdown of convertible bond terminology — conversion ratio, conversion price, conversion value, straight value, and why CBs trade above their theoretical floor.

OK first things first — let’s nail down the terminology for convertible bonds.

Price, premium, whatever — do NOT get these mixed up. Each one points at a very specific thing!

We saw this stuff back in Level 1 too!

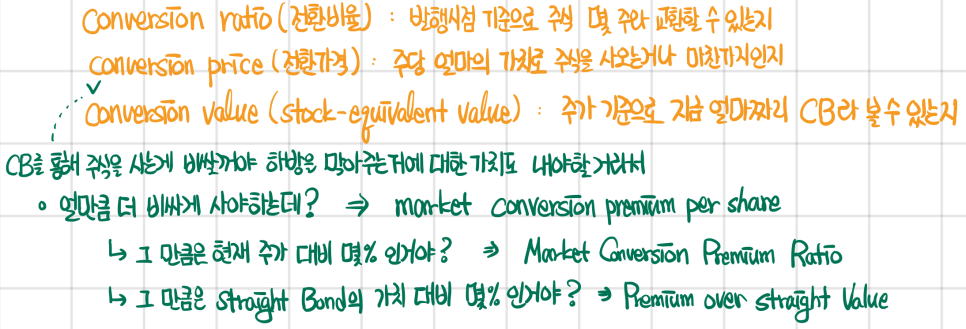

So this thing is a CB, which means there’s gonna be some clause like “one bond can be exchanged for X shares of stock,”

and if that number of shares you can convert into is, say, 5 shares,

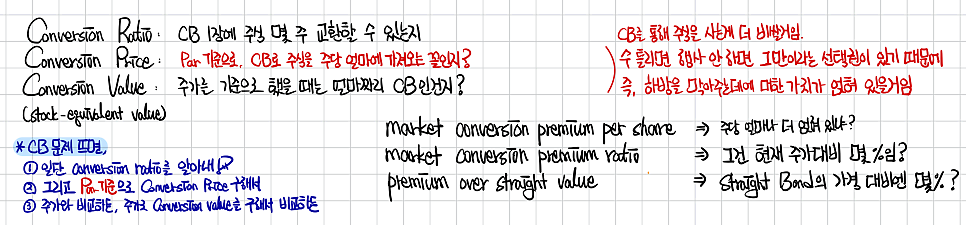

we call that the conversion ratio.

OK now say I bought the bond at face value — $1,000.

Asking to swap it for 5 shares is basically the same as asking the company to issue me new shares at $200 a pop,

and that price is what we call the conversion price.

So — the conversion price is locked in at issuance!

Now let’s say that stock is trading out there in the market.

Market price right now: $300.

I’m holding one bond,

but if you squint at it, I’m basically holding 5 shares of stock.

Looked at that way, I’m sitting on $1,500 of value,

and this number — conversion ratio × market price ⇒ is called the conversion value,

which also goes by stock-equivalent value.

Thinking in value terms, a CB is basically

the value of a straight bond ⨁ plus the value of the conversion option tacked on top.

CBs usually pay a smaller coupon than they would if issued as a plain straight bond (often something like 1%-ish).

And the value when you look at JUST the straight-bond side of it is called the straight value.

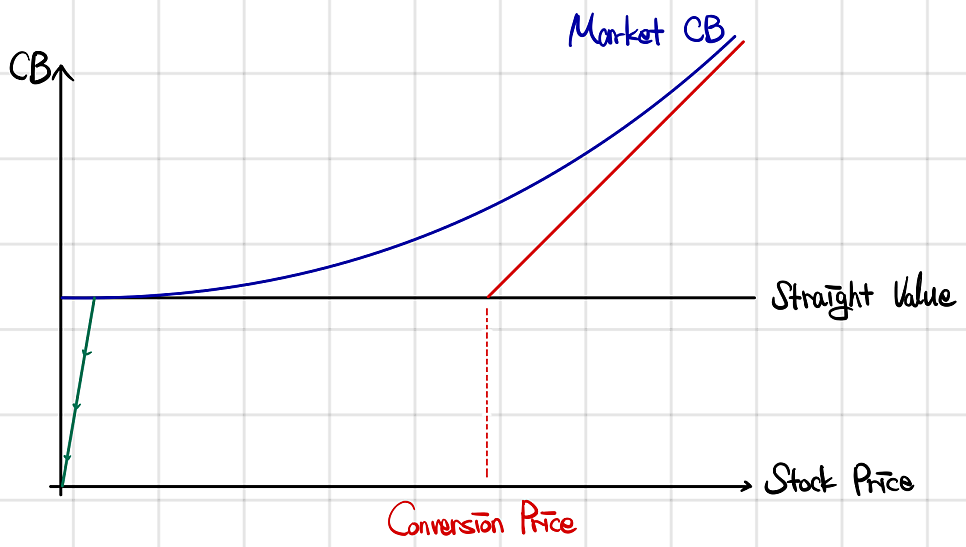

OK now let’s see what the relationship between the CB and the stock price actually looks like on a chart.

Even if the stock price drops to 0, the SB part of the CB still has bond value sitting there, so the whole thing has a floor under it.

And once the stock price climbs above the conversion price — that’s the moment bondholders go “yep, time to convert."

But in the real market, CBs tend to trade a little above these theoretical values.

i.e. CB value > Max(straight value, conversion value).

Sure, if the stock price collapses toward 0, the company’s basically one bad week away from bankruptcy,

so the CB price nosedives with it (this is called a busted convertible),

but obviously that’s not something we need to sweat for CFA exam purposes.. heh

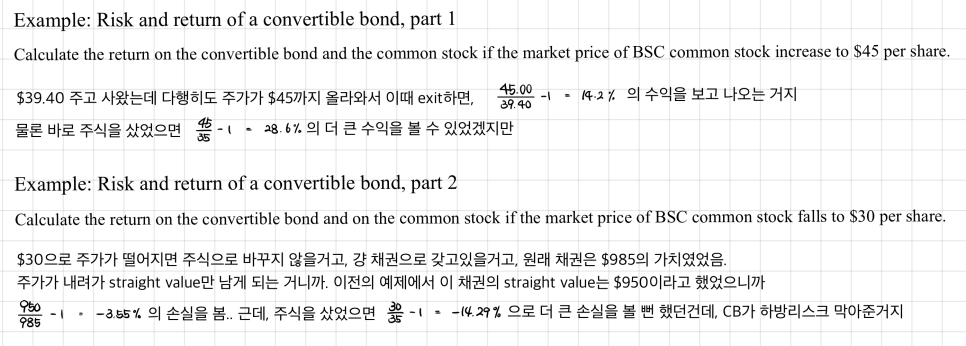

We said straight value = $950,

and conversion value = 25 × $35 = $875,

so we can say this bond has at least $950 of value!

Now a few more terms coming at you here…

Hold these tight and don’t get them mixed up (T_T)!!!

To buy this bond right now, you’d have to fork over $985,

and if you buy it at $985 and then convert it into 25 shares at $35 each,

how much are you actually paying per share?

Same as buying at $985/25 = $39.40 a share, right??

→ That’s the market conversion price!!!!

The CB is more expensive?! Yeah, obviously — the CB protects your downside,

so you could say it’s the price you pay for that downside protection…

→ that’s called the market conversion premium!!

market conversion premium per share = market conversion price - stock’s market price

You can also flip this and say it like “there’s an X% premium over the current stock price~”

→ that’s the market conversion premium ratio..

And then there’s another version that says “there’s this much extra over the straight value~"… (T_T) Premium over straight value

Summary

A little extra from the net summary material.

Callable Convertible Bonds

* Keep in mind a single bond can have multiple options stapled to it; treat this as one example of that.

Holding one CB is the same position as holding one SB

⨁ while simultaneously holding a conversion option,

* (conversion option: this has the same character as being long a call option on the stock)

So — if the volatility of the stock goes up → the call option’s value goes up → the value of the Convertible Bond goes up!!

OK then what about a Callable Convertible Bond…

Here “Callable” means the issuer can call the Convertible Bond itself back!!

Same logic, just extended:

Callable Convertible Bond = SB + conversion option - call option (on CB)

*conversion option ≅ call option on stock

If stock price volatility goes up, CCB value goes up,

and if interest rate volatility goes up, CCB value goes down!

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.