Credit Valuation Adjustment (CVA)

Diving into CVA — that shave-off amount on OTC derivative valuations that accounts for counterparty default risk, because zero-risk counterparties just don't exist.

Chapter 4. Credit Analysis Model.

The stuff up through chapter 3 wasn’t a walk in the park either, but…

…from here on out, chapter 4, things get harder, and harder, and harder, and harder. T_T

It didn’t get ranked the #1 hardest chapter for nothing lol.

So — it’s called Credit Analysis, which means we’re zooming in on the bonds that actually carry credit risk. Corporate bonds and friends. That’s the playground for this chapter.

Back in Level 1, I studied something called fundamental credit analysis.

Basically: to figure out if the company that issued the bond is gonna default, you rip apart the financial statements,

eyeball some Financial Ratios,

then rip apart the Indenture too, to see what conditions got attached at issuance…

That was pretty much the whole song.

But — financial statements aren’t real-time. They’re history. Past data.

And trying to predict default accurately from yesterday’s numbers… c’mon, there’s gotta be a limit to that, right?

Here’s the thing: whether this company is about to go belly-up — the market will tell us before the F/S ever does.

How does the market tell us? Through the stock price.

Starting with does the stock go up or down,

and then what does the volatility look like — couldn’t we read off the probability of default from signals like these..?

That’s the whole pitch. heh

And it’s not just stock price either.

The corporate bond price in the bond market,

and how much spread is baked into it — we can pull info out of those too,

and basically, let’s talk about default risk by reading the signals the market is already broadcasting at us!

That’s what this chapter is. Alright, follow the book!

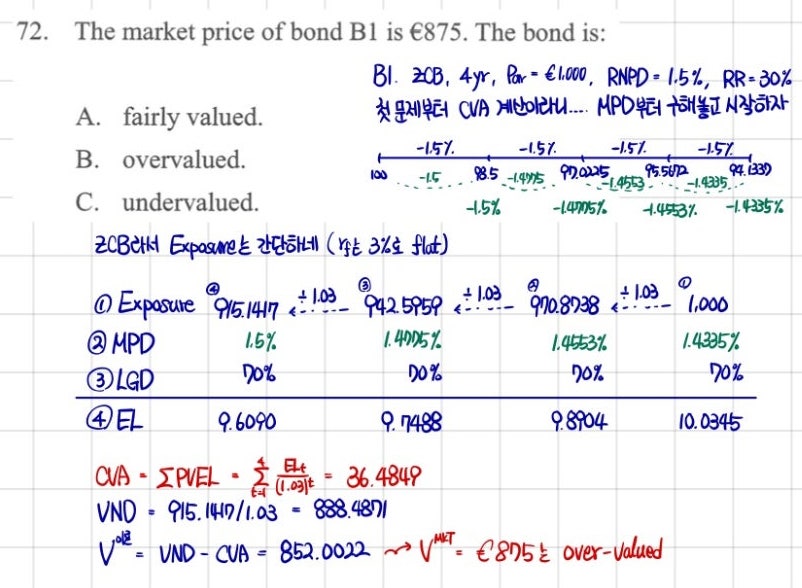

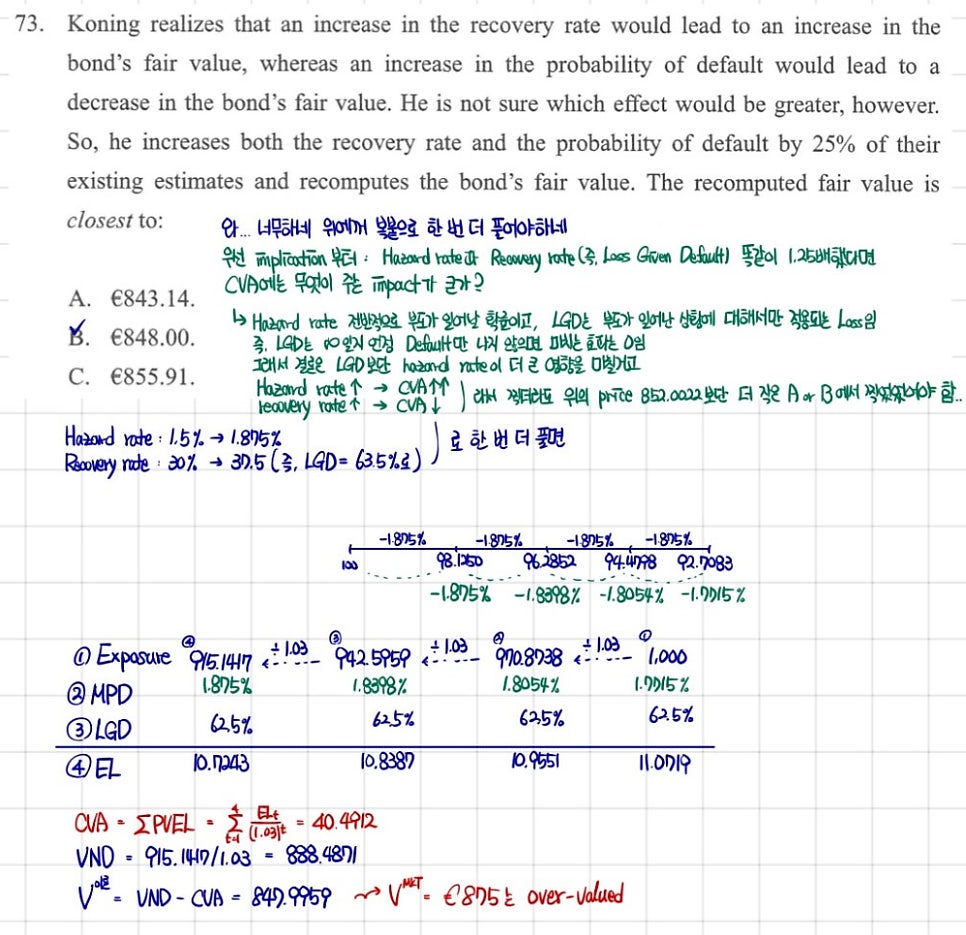

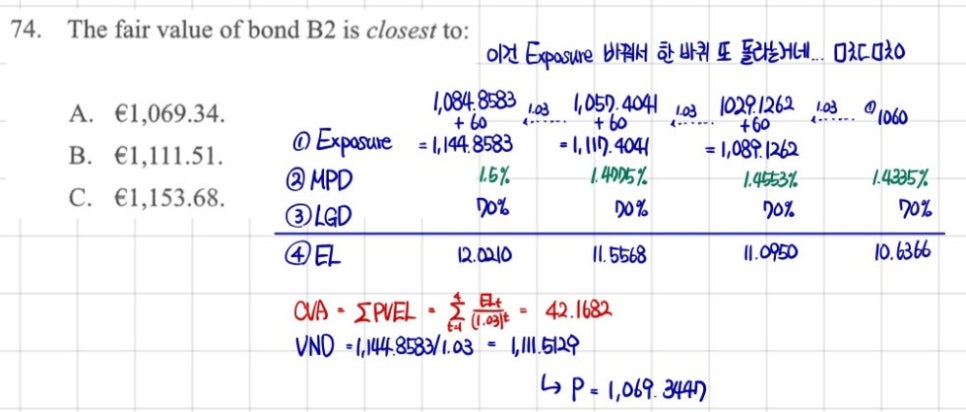

CVA (Credit Valuation Adjustment)

So the very first thing we hit is: what is CVA,

and honestly, from the few sentences of intro the book gives you, it does NOT click in one shot..

Just let it wash over you for now, and after you’ve trudged all the way to the end of the section,

then it kinda clicks — at least roughly — what this thing is.

But still, let’s at least get a vague feel for what CVA does before we dive in.

In Derivatives, you get questions where you have to value an OTC derivative — a swap, a forward, whatever —

and if you use the risk-free rate as your discount rate when you do that valuation,,

that’s the same as saying the counterparty has zero risk.

But… does it really make sense to claim the counterparty in an OTC derivative has zero risk?!?

Right? So the PV you got that way — we need to shave it down a bit more!!

⇒ And the amount we shave it down by? That’s exactly CVA.

That shave-off amount is built on the idea of “in the worst case (Default), how much money do we think we’d actually lose?"… and that’s about as far as we can go with it for now.

OK OK, before we go any further we gotta line up some terminology.

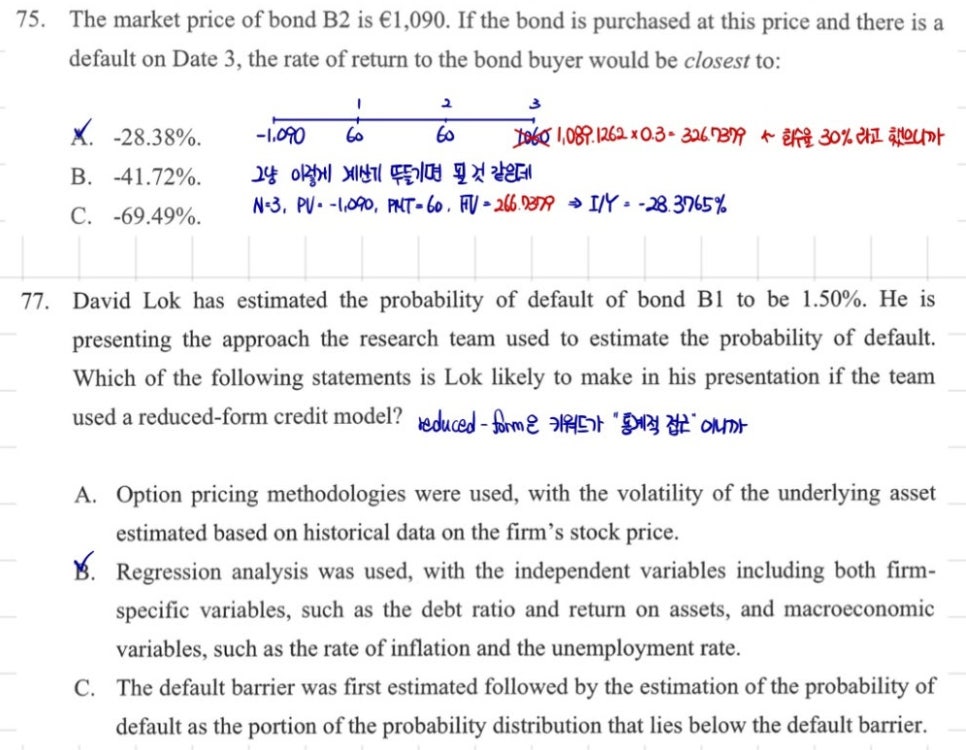

Expected Exposure (Exposure at Default): is the amount of money a bond investor in a credit risky bond stands to lose at a point in time before any recovery is factored in

If default actually happens — for someone holding a credit risky bond, before you account for the recovery rate — how much do they stand to lose, baseline?

Recovery Rate: is the percentage recovered in the event of a default

If default happens, how much can you actually claw back → expressed as what % of Exposure you recover.

Loss Given Default: is equal to loss severity multiplied by exposure

This is just 1 − recovery rate,

so basically, it’s the actual % loss you eat at default, after taking the recovery rate into account.

Probability of Default: is the likelihood of default occurring in a given year

So you’ve got a PD for year 1 / year 2 / … / year n. Like that.

Hazard Rate: is the conditional probability of default given that has previously not occurred

It’s a conditional probability, and the condition is: “given that default has not happened before this point.”

Technically, in a continuous model the continuous default probability is the hazard rate, but since CFA doesn’t go all the way to the continuous version, apparently they just explain HR up to about this level..

Probability of survival: is 1 − probability of default

OK rough terminology dump — done.

We’ve got the gist, so now let’s sort out how all these things actually relate to each other.

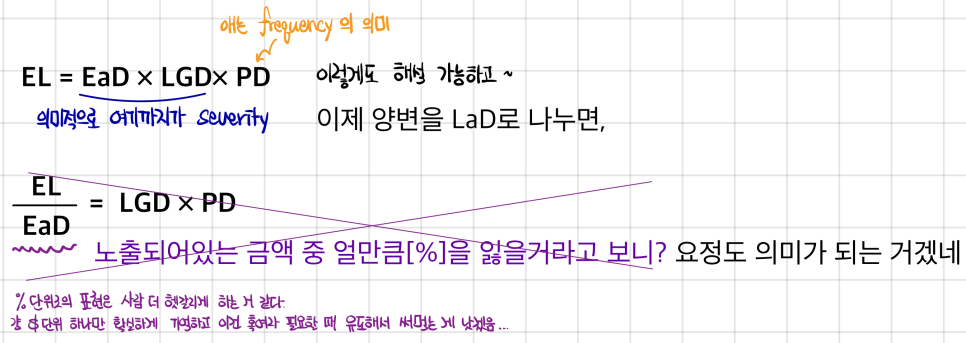

OK OK — Expected Losses — the unit is money, as the name suggests,

and it’s not a present-value amount, it’s a money amount at some future point in time.

(later we’ll also work through dragging that ‘future-point money amount’ back to present value)

So now, computing EL for each period and dragging it back to present value,

and stacking the whole thing up — that’s the recipe for CVA.

But there’s still a bit more to look at,

so let’s sort out a couple more concepts before we get into CVA proper.

There are two things you really need to nail down before moving on.

Hazard rate / Probability of Default — you’ve gotta know exactly what each one is saying. Let’s hit them one by one!

First, Hazard Rate — we summarized it as

“the conditional probability conditional on default not having happened just before,”

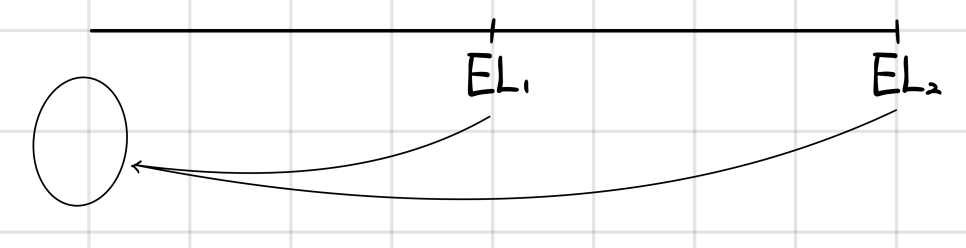

and what that’s really saying is “of the ones still alive, what % die” —

⭐️ At the end, if you just count up the dead, it’s 10 / 18,

and if you take the starting value as your base,

10% / 18%

⇒ PD computed without slapping a condition on top like this — that’s called unconditional probability of default.

The book calls this Marginal Probability of Default.

So now let’s say the insurance company is expecting 10 deaths in year 1 / 18 deaths in year 2, that kind of thing.

The company will be expecting an insurance payout loss in each year,

And when you drag it back like this — that’s what becomes the Credit Valuation Adjustment.

The amount we need to shave off!!!

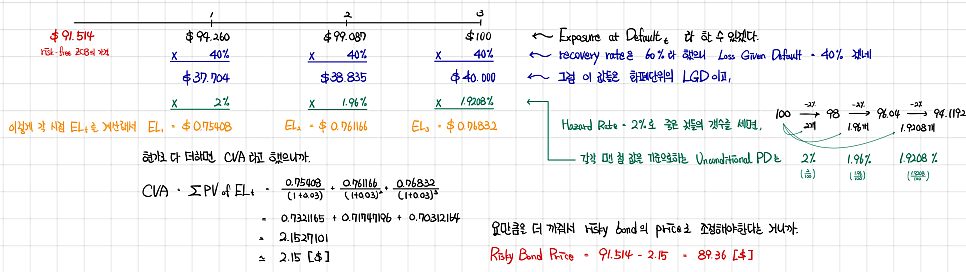

Credit Valuation Adjustment (CVA): is the sum of the present value of the expected loss for each period CVA = price of risk-free bond − price of risky bond

The price gap is exactly that much — that’s the whole concept~

Phew… terminology, done… heh.

We don’t know what form the terms are gonna show up in on the exam,

so you really do need to understand and memorize them. Let me do one last pass…

What the book calls Hazard Rate = Conditional Probability of Default,

and what the book calls Marginal Probability of Default = Unconditional Probability of Default.

And for Cumulative Survival Probability:

Having gotten this far, CVA doesn’t really feel like that terrible a concept..?

It’s just that on the way here, the terminology overlaps with this thing and overlaps with that thing,

and the fact that the same idea gets called this or called that is the only part that makes it confusing.

But honestly, all it really is is: take the bond valuation you did with the risk-free rate,

and shave it down by the present value of the money you could realistically lose. That’s it? heh heh heh

(This wasn’t a big deal in the old days, but starting with the 2008 Global Crisis, once we saw that even huge financial institutions could default, and realized that the counterparty in an OTC derivative could also default~ (to even play in OTC derivatives, your credit rating has to be pretty solid) — from then on, apparently CVA became a big-deal topic.)

CVA was a part I really struggled with at first,

but it kinda gets demolished automatically once you grind through a few practice problems,

so I’m gonna dig up some CVA problems from my problem-solving stash and toss them in here too!!!!!

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.