Risk-Neutral Probability of Default

Risk-neutral (aka implied) default probability is just the PD that calibrates you to market prices — so you can discount everything at the risk-free rate, no guesswork needed.

In the example before, we used default probabilities based on each year’s expected likelihood of default.

But that’s the view from “I’m using my own estimates and I don’t really trust the market price.”

When you instead back out π (the hazard rate) so that it’s calibrated to the market price,

the default probability you get is what we call the “risk-neutral probability."

In the previous example, we used a probability of default based on the expected likelihood of default in any given year.

In practice though, we use the “risk-neutral probability of default” — the default probability that’s implied by the current market price.

OK so first — what does “risk-neutral” even mean????

Punchline first: it’s “the probability that lets you discount everything at the risk-free rate.”

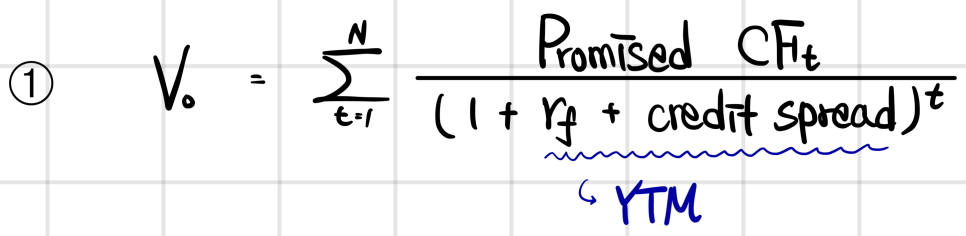

A bond has cash flows that are promised and locked in from the get-go,

and when you go to value something like that,

we do it like this. That’s the most traditional way — there are others, but this one’s the classic.

You take the promised cash flows of a risky bond and rewrite them as if they were equivalent to risk-free cash flows — like, “how much would that be?” — and restate them that way.

And there’s another approach where you tweak the numerator instead, and then just use the risk-free rate in the denominator.

This kind of approach is what people call “Risk-Neutral Valuation.”

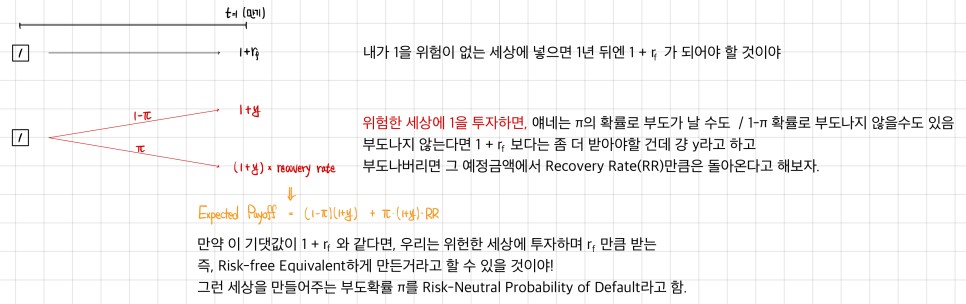

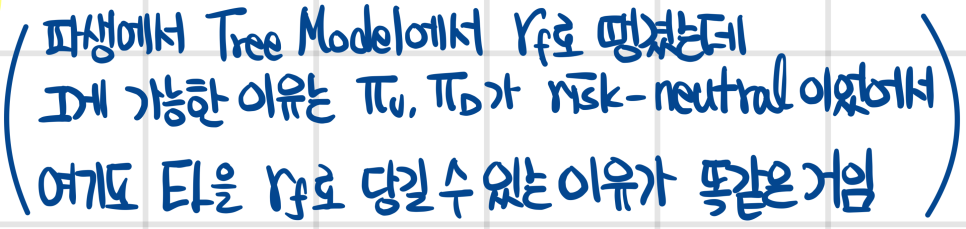

Now, as for how you convert to a Risk-Free Equivalent Cash Flow —

you take the risk-neutral probability and build an expectation out of it,

So Risk-Neutral Default Probability is also called “Implied Default Probability,"

and why is that?

The fact that they slap the prefix “implied” on it — that meant “based on info coming from the market,” right?

And the CVA here is, in fact, also built from market info.

If you’ve got the price of the risky bond currently trading in the market, and you’ve also got all the spot info you need,

→ you can take that risky bond and discount it at the risk-free rate to construct the risk-free version of its price.

The difference between that hypothetically-constructed risk-free price

and the price of the risky bond actually trading in the market — that’s exactly the CVA. ← boom, you’ve already got the answer.

What you’re really doing is finding the PD that fits that CVA — the answer you already have.

So: it’s the probability that calibrates you to a risk-free world → it’s risk-neutral.

And it’s what the market price is telling you → it’s also Implied.

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.