Credit Scores and Credit Ratings

A quick breakdown of how credit scores differ from credit ratings, why subordinated bonds get notched down, and what credit migration does to bond prices.

When you lend money to a person, what matters is their credit score.

For companies, though? Not a credit score — a credit rating.

And here’s where it splits in two:

One is the rating of the issuer (the company, the institution). The other is the rating of the bond itself.

But check this out — the issuer’s rating isn’t measured separately by some fancy standalone method. Nope. They just take the rating of the unsecured credit bond — the one propped up purely by that institution’s bare-naked creditworthiness — and call that the issuer’s rating.

OK now, a company can also issue subordinated bonds (subordinate),

but… would the rating actually differ much?

Like — same issuer, same everything, two flavors of bond: subordinate or not. If that company defaults, both bondholders are equally screwed, aren’t they?

⇒ The recovery rate at default is different. That’s why subordinated bonds get knocked down a Notch or two, apparently.

Notching accounts for LGD differences between different classes of debt by the same issuer

So what happens to a bond’s price when its credit rating changes (this is called credit migration)???

Credit rating is hooked directly to spread,

so the effect of a rating change on the spread ⇒ we can pin that down using duration.

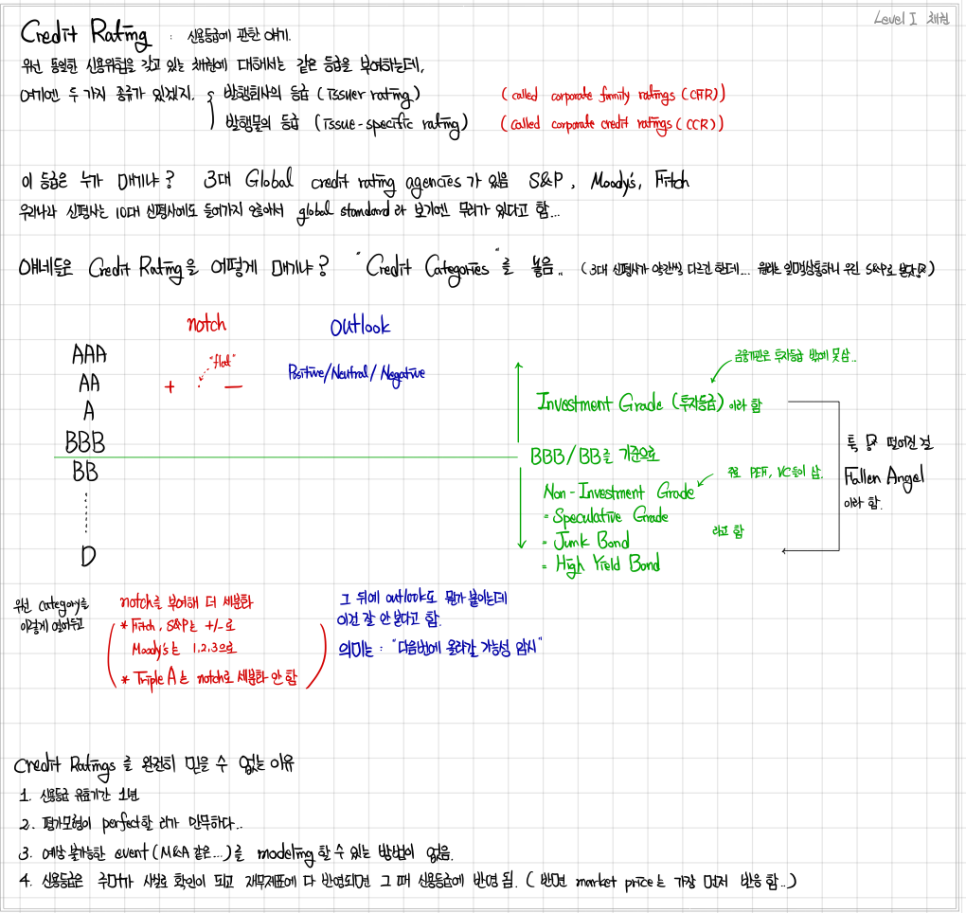

Just for reference — here’s the Credit Rating section from when I was grinding Level 1.

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.