Structural and Reduced-Form Credit Models

A casual walkthrough of structural vs. reduced-form credit models — just enough to nail the pros and cons without drowning in the math.

Haa… another rough one.

So what’s this model again? It’s a model about probability of default.

(And once you’ve got PD, you’re pretty much one step away from Expected Loss, so you could just as well call it a model about EL.)

Anyway — this one’s originally pretty heavy stuff.

You don’t really need to nail down all the gory mathematical foundations behind these two model types. What you DO need is a solid grip on the pros and cons of each.

Because in the CFA they basically just give you a taste and then move on… heh.

So let’s listen lightly and just make sure we nail the advantages and disadvantages!!

Structural Model

Structural Model of corporate credit risk are based on the structure of a company’s B/S and rely on insights provided by option pricing theory(Black-Scholes PDE)

Not the B/S you’d see in the accounting books — the B/S in Economic Value terms.

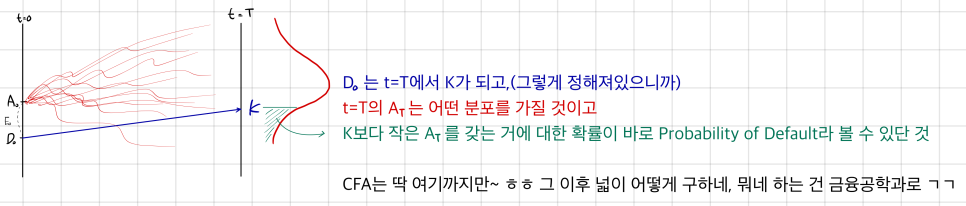

Say it looks like this at $t=0$:

And if we lay this company out on a timeline,

Since there’s no CF that has to go out anywhere in between up until $t=T$, there’s literally zero chance of default at any moment other than $t=T$.

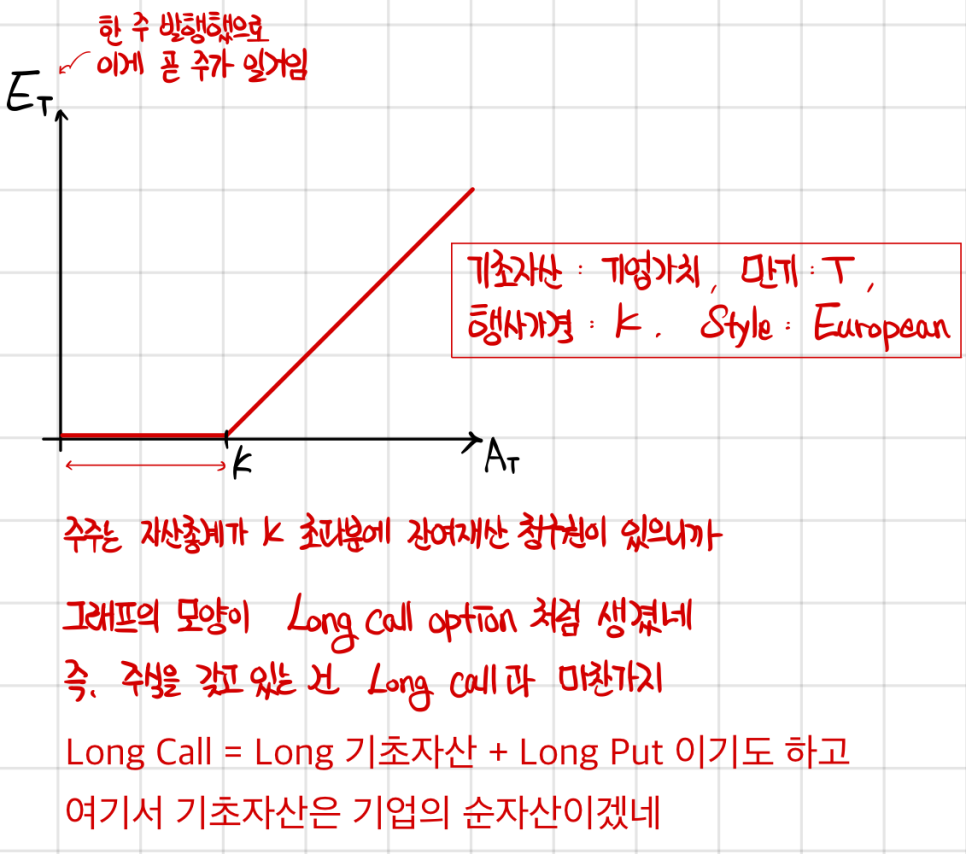

Now, depending on what the asset value $A_T$ ends up being at $t=T$ (given we started with $A_0$ at $t=0$), here’s how the bond value and equity value shake out:

So summing up, at time $T$ ($t=T$):

This is really just the pictures above, written out as equations. Nothing more.

Let me jot down a bit of the textbook content too… I’m getting anxious.

An alternate, but related interpretation considers equity investors as long the net assets of the company and long a put option,

allowing them to sell the assets at an exercise price of K. Default is then synonymous to exercising the put option

So holding equity is the same as taking a position of “Long net assets of the company AND Long a put option.”

Whether you think about it via put-call parity, or just sketch it out and stare at it for a sec — it’s the kind of thing you can nod along to pretty easily.

Saying: holding equity can also be viewed this way. It’s basically just put-call parity in disguise… hehh.

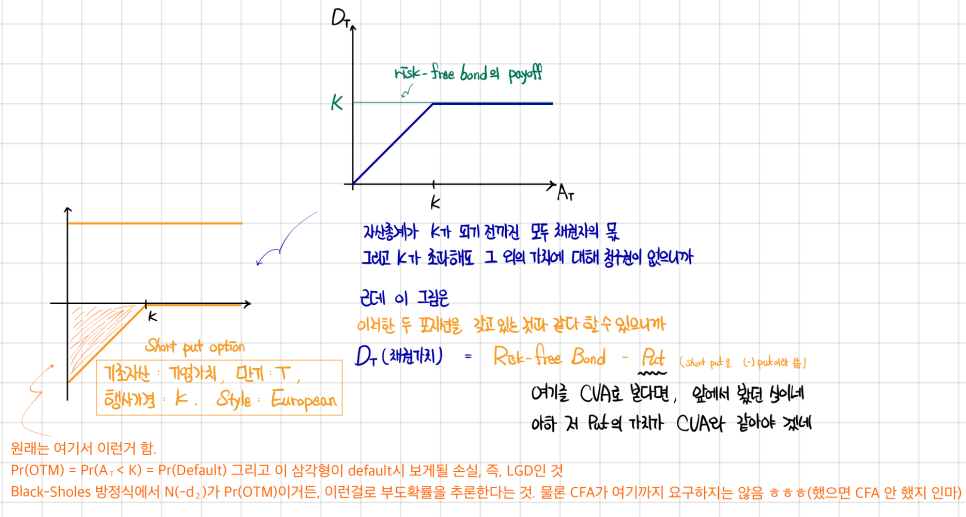

Under the put option analogy, the investors in risky debt can be construed to have a long position in risk-free debt and a short position in that put option.

Value of risky debt = value of risk-free debt - value of put option → recall that, value of risky debt = value of risk-free debt - CVA

Therefore, the value of the put option = CVA

Distribution of Asset Value at time T

OK, now the part that actually matters for the exam — pros and cons!

Advantage of Structural Model:

➀ It explains why default happens. (If $A_T < K$, default.)

➁ Since it leans on the Black-Scholes equation, it’s got serious theoretical muscle.

Disadvantage of Structural Model:

➀ In real life, no actual company is going to issue exactly one ZCB and call it a day. The real B/S is going to be way messier — and a messy B/S just can’t be modeled cleanly. (Plus, “Economic B/S”? Come on. That’s already a stretch;;)

➁ To actually satisfy the Black-Scholes assumptions, you have to assume the Asset trades continuously in the market. But to make that work, you’d be saying the company’s underlying assets are being traded out there… which isn’t even observable. Makes zero sense.

Reduced Form Model

do not rely on the structure of a company’s balance sheet and therefore do not assume that the assets of the company trade.

Unlike the structural model, reduced form models do not explain why default occurs.

Instead, they statistically model when default occurs.

Default under the RF(reduced form) model is a randomly occurring exogenous variable.

This guy doesn’t sit there staring at the B/S. It’s a model that statistically asks: when does default happen.

If we run with the default-as-dying analogy — everyone dies once. And instead of asking why they die, you’re asking when they die.

A key input into the RF model is the default intensity, which is the probability of default over the next (small) time period

Picture dominoes:

Whether 100 dominoes go down inside one minute comes down to how fast they’re falling — fast enough or not. And there’s a thing called Default Intensity — basically the speed at which default happens — and that’s the key input that goes into this model.

And this default intensity? It gets estimated via regression modeling. That’s why people call this a statistical approach.

When you run that regression, you’re feeding in stuff like the company’s leverage / beta / interest coverage ratio. So default intensity is estimated from inputs like those.

Advantage of Reduced Form Model:

➀ You don’t need that crazy assumption that the company’s Assets have to trade in the market.

➁ Default intensity is allowed to vary as company fundamental changes, as well as when the state of the economy changes

When you’re estimating the key input — default intensity — you’re throwing in fundamentals, macro indicators, all kinds of stuff. Makes it pretty persuasive.

Disadvantage of Reduced Form Model:

➀ It can’t explain why default happens.

➁ Default’s treated as a random event, but in reality? Calling default “random” is a stretch. Most of the time it’s at least somewhat anticipated — like when a company’s credit rating keeps sliding down and down.

Anyway — for the exam, compare the two models side by side and lock in those advantages and disadvantages!

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.