Credit Spread Analysis and Term Structure of Credit Spreads

VND, CVA, and why credit spreads have their own term structure — plus what credit quality, the economy, liquidity, and equity vol do to the curve shape.

We already know what a credit spread is.

$$\text{Credit Spread on a Risky Bond} = \text{YTM of Risky Bond} - \text{YTM of Benchmark}$$Right? Stuff we’ve already covered.

But here we pick up one more term — and conceptually it’s also stuff we’ve already seen. So just think of it as adding one new piece of vocabulary to the pile.

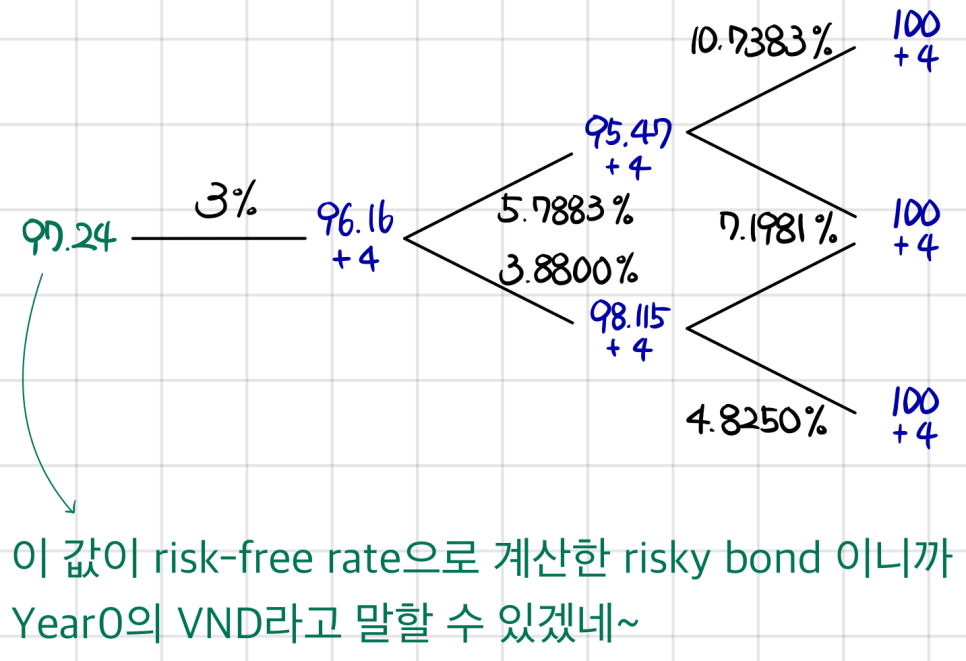

The value of a risky bond, assuming it doesn’t default, is its value given no default (VND).

VND values the risky bond using the risk-free rate. Remember when we did CVA earlier? We discounted the corporate bond at the risk-free rate, and then went “OK we still need to adjust this~” and subtracted CVA. That thing we discounted at the risk-free rate — that’s basically VND. heh

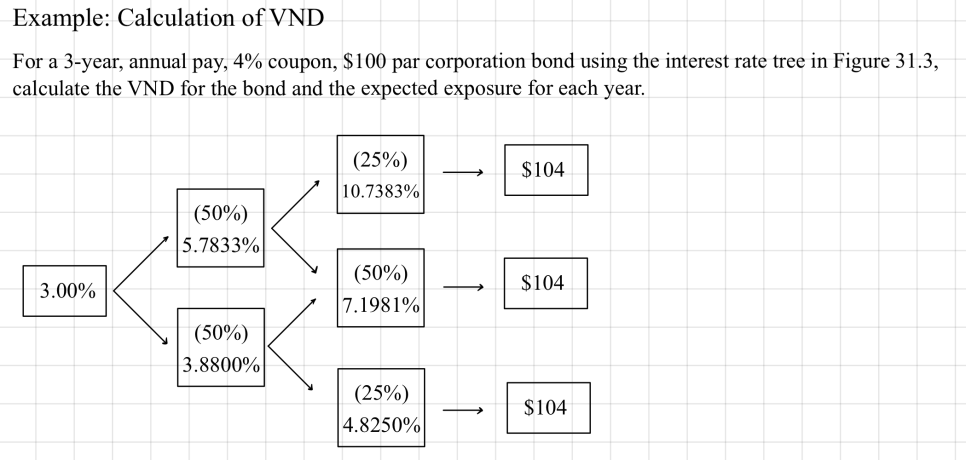

$$\text{Risky Bond Price} = \text{VND} - \text{CVA}$$Up till now, whenever we calculated CVA, we just pinned YTM at some value and discounted with it. We hadn’t been using a tree for this. But actually — you can do this just fine with a tree model. Let’s practice.

They don’t explicitly say “this is a tree”, but since they’re asking us to find VND with it, it has to be the risk-free rate.

And honestly… there’s nothing new compared to before. If you stripped the term “VND” off, could you even tell whether this is a previous-chapter problem or a credit-spread problem?

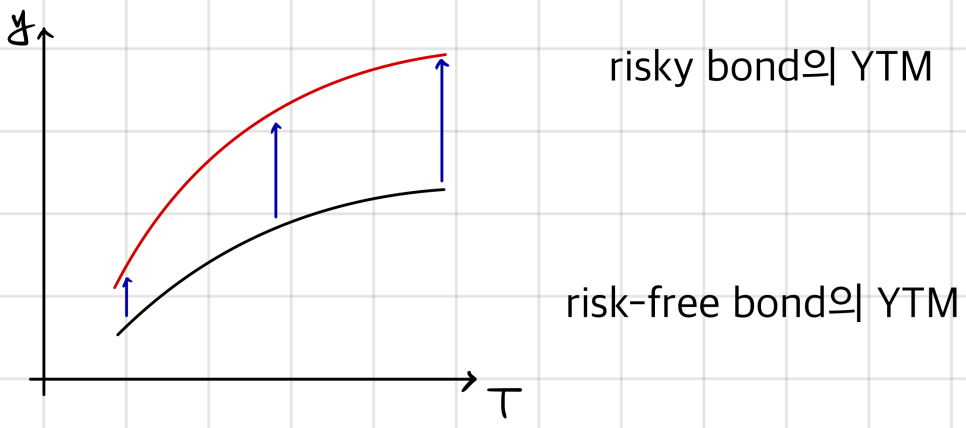

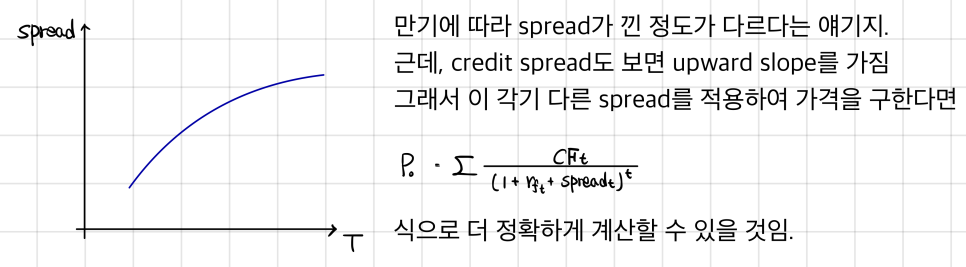

Credit spread has a term structure too.

Credit spread is inversely related to the recovery rate and positively related to the probability of default.

Makes sense — if the recovery rate is high, you don’t need to demand as much over the risk-free rate. And the higher the default probability, the more premium you’d want. That’s all it’s saying.

Determinants of the Term Structure of Credit Spread

Credit Quality. AAA term structures tend to be flat or slightly upward sloping. Lower-rated sectors tend to have steeper spread curves.

So: high credit ratings → flat-ish term structure. The more you slide toward junk, the steeper it gets.

Financial condition. Spreads narrow during economic expansion and widen during cyclical downturns.

The state of the economy matters too — and since everything moves together, we don’t talk in terms of flat/steep here, we talk in terms of widen/narrow!

Market Demand and Supply. Less liquid maturities show higher spreads.

Liquidity matters. And since liquidity is itself partly a function of when the bond was issued, this becomes a factor that can mess with the curve shape.

Newly issued bonds are generally more liquid, so when an issuer refinances a near-dated bond with a longer-term bond, the spread on the longer maturity can actually look narrower — sometimes giving you an inverted credit spread curve. So this is a factor that can keep the curve from sloping cleanly upward.

Equity Market Volatility. If equity markets get jittery and vol picks up, then — per the Structural Model — the probability of default reacts, and the spread widens.

Honestly this feels like the kind of thing I’d nail if it came up as a multiple-choice option… heh heh. But by the time I’m deep into another subject, this content will have completely evaporated from my brain… lol. Seriously… lol.

Credit Analysis of Securitized Debt

This is the securitized-bonds bit, but… there’s nothing wild here.

Securitized debt is usually financed via a bankruptcy-remote SPE. This isolation of securitized assets allows for higher leverage and lower cost to the issuer.

So: securitized debt is normally issued through a bankruptcy-remote SPE, and this SPE is a paper company that exists only to issue bonds and raise funds. So it’s totally insulated from the bankruptcy of the financial institution.

And investors in ABS get their cash flows from the underlying asset pool — flows from the pool — which gives them a kind of diversification effect. So the premium you collect relative to the risk taken is pretty high.

Components of Credit Analysis of Securitized Debt

OK so when you’re sizing up securitized debt, what do you actually look at?

① Collateral Pool. First you’ve gotta see where this bond is sticking its straw. When you look at the pool, two things to check: homogeneity and granularity.

Homogeneity of a pool = similarity of the assets inside the collateral pool. You want to see whether things with similar risk profiles are properly bundled together.

Granularity = transparency of the assets inside the pool. “Granular” — think baby formula powder, ground crazy fine. You want to see whether the pool is finely diced across many companies. Should look nothing like a single lump-sum bet.

② Servicer Quality. The servicer is something like a bank. If we’re talking MBS, you’d want to look at which bank the mortgage loans inside were originally purchased from, that kind of thing. Were they bought from a bank that does strict loan screening, or not? And what’s the bank like at managing customers post-sale, so delinquencies don’t pile up when they’re collecting principal and interest? Stuff like that.

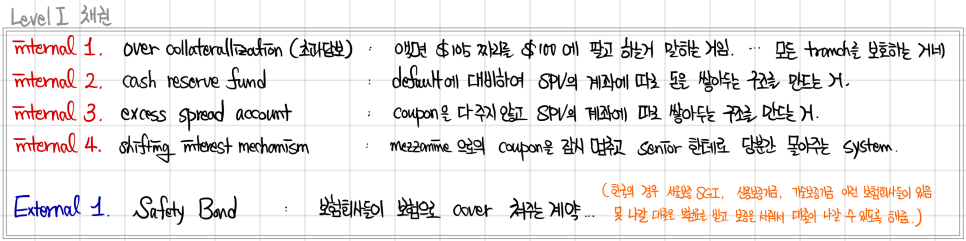

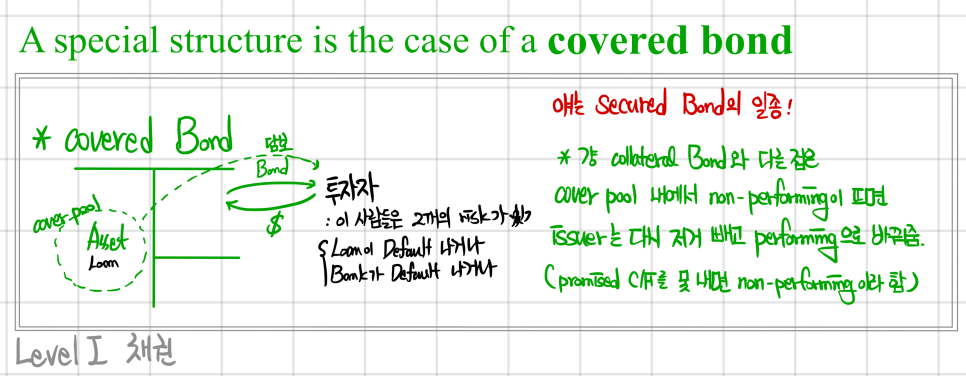

③ Structure. Back in Level 1 we studied this thing called a tranche, and yeah — we need to look at how the tranche structure is set up. First, obviously, is ours Senior / Mezzanine / Equity? And what kinds of credit enhancement are baked in?

Back in Level 1 we got the rough tour of how credit enhancements can be applied internally vs. externally, right?

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.