Credit Default Swaps (CDS) and CDS Premium

CDS isn't your typical derivative — it's basically bond insurance, and this post breaks down the structure, settlement types, and why you don't even need to own the bond.

OK so CDS is technically a derivative…

But it’s a different beast from the derivatives we covered earlier in the Derivatives section. Those are what we call market derivatives — you fix an underlying asset and bet on which way it goes. The underlying (stock price, interest rate, FX rate, whatever) moves around in the market, we can’t control it, so we study market derivatives as a way to hedge against those moves.

CDS isn’t that. CDS is a credit derivative.

And credit derivatives actually come in a bunch of flavors — Total Return Swap, Credit Spread Option, Credit Spread Forward, all sorts. But apparently in the CFA we only touch CDS, and even then just a tiny sliver of it. heh (Thanks, CFA~)

Credit Default Swap (CDS)

A CDS is basically an insurance contract.

Like, literally — it’s insurance. “Hey, if the value of my asset tanks, please cover the loss for me.” That’s a CDS.

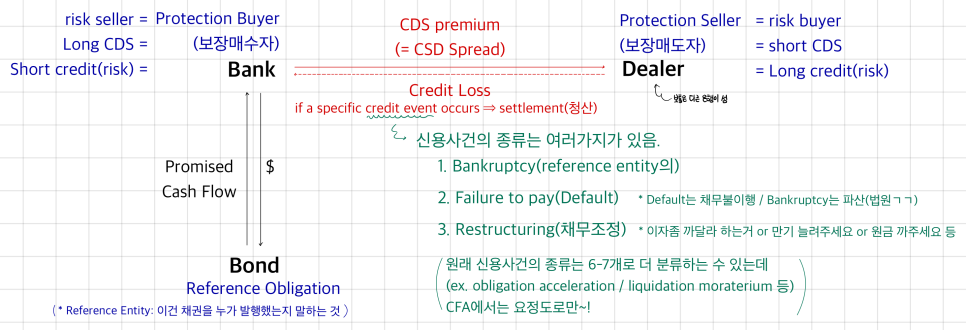

So what does the structure actually look like? We saw a version back in Level 1, but this chapter goes deeper, so let’s redraw the CDS structure, Level 2 style.

The biggest CDS counterparties are banks. So picture this: a bank buys a bond, but it’s a risky bond — default is on the table. So the bank goes to a dealer and says, “I’ll pay you a premium, and if a credit event hits this bond, you cover the credit loss.” That contract is the CDS.

Settlement protocol:

The instant a credit event happens, the dealer and the bank have to settle up. In other words — the “insurance company” has to actually pay out the insurance money! That settling-up process is called settlement, and how you do the settlement has to be decided in advance. Apparently it’s spelled out in the contract.

- Hand the defaulted bond to the dealer, dealer wires the principal to the bank → Physical Delivery

- Just transfer cash equal to the bond’s drop in value and call it done → Cash Settlement

How much cash, though?

It’s Face Value − Recovery.

Recovery can be ambiguous, so:

i) you can lock it in from the start as RR = 40%, or ii) you can agree to do a market poll — literally ask the market.

There are more variations, but in CFA it stops about there! lol

Anyway — first thing’s first, nail the terminology!!!!

Now here’s where CDS differs from regular insurance. Say you want to buy fire insurance and you tell them, “If that building across the street from my house burns down, pay me out.” They won’t sell it to you. There’s no insurable interest — insurance only works on stuff you own.

But CDS? Nope. You don’t have to own the bond to write a CDS on it. It’s not like only a bank holding the bond can enter a CDS contract.

Which means some pretty interesting stuff can happen.

You think Company A’s bond is gonna blow up. You don’t hold it, but you go ahead and write a CDS with physical delivery. And boom — you were right! Company A’s bond crashes and you hit the jackpot.

But wait — to get paid, you have to buy that bond and deliver it. And when you go to buy it, the price has shot up, so your jackpot shrinks. That kind of thing can happen.

(Literally the same setup as a short squeeze. heh)

How is the CDS premium determined?

It tracks the creditworthiness of whatever’s being insured. High credit quality → small premium. Low credit quality → big premium.

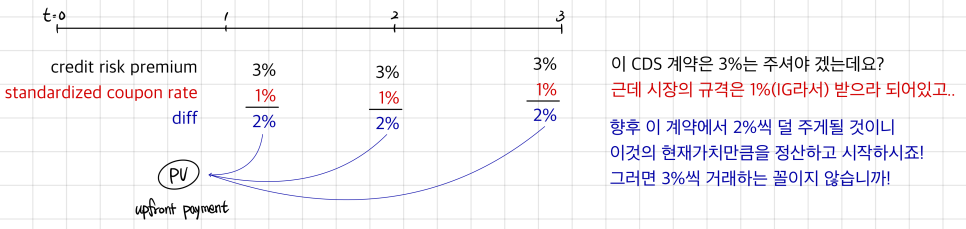

But if you had to recompute every premium from scratch for every contract, you’d never get a deal done fast enough. So apparently this gets somewhat standardized —

Even though the CDS spread should be based on the underlying credit risk of the reference obligation, standardization in the market has led to a fixed coupon on CDS products: 1% for investment-grade securities and 5% for high-yield securities.

It’s NOT that every IG name trades at 1% and every HY name at 5%. Obviously — within IG alone, a AAA and a BBB should look totally different.

The present value of the difference between the standardized coupon rate and the credit spread on the reference obligation is paid upfront by one of the parties to the contract.

So they patch the gap with an upfront payment, and the snippet above tells you how that amount is set.

What that’s saying is —

Paying that gap in advance, to make the values match — that’s the upfront payment.

(It’s the same idea as those car rental / leasing contracts. lol No free lunch in this world~)

The protection buyer (the bank) is kind of like being long a put option. Not exactly — the bond price isn’t just falling on its own, it’s hedging the price drop from a credit event, so… yeah yeah, you get the gist.

International Swaps and Derivatives Association (ISDA): the international derivatives association.

They publish standardized contract terms and conventions in the ISDA Master Agreement. Apparently they’ve put together a standardized contract template, and people customize it from there to actually trade.

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.