Credit Default Swaps (CDS), Part 2

A casual breakdown of single-name vs. index CDS, how credit correlation drives pricing, and why expected loss is the number that really matters.

Single-Name CDS

A single-name CDS is exactly what it sounds like — there’s exactly one reference obligation.

Instead of just one, you can also bundle bonds from several different companies together like a basket — that’s called a multi-name CDS (Basket CDS). (“If even one out of the bunch defaults, pay me~”)

But CFA only deals with single-name CDS. (I’m liking CFA more lately heh)

The bond that becomes the reference obligation is usually a Senior Bond, and in that case it’s also called a Senior CDS.

Here’s the key thing — the CDS pays off not only when the reference entity defaults on the reference obligation, BUT ALSO when the reference entity defaults on any other issue.

So a payoff doesn’t only trigger when the specific bond I’m holding defaults. It also triggers if some other bond from that same company defaults.

(Apparently this kind of clause is buried in our regular loan agreements too.. we just never read them lol. It’s called the “acceleration of obligation” clause.)

So in the end, the credit event is determined based on the reference entity, not the reference obligation.

The CDS payoff is based on the market value of the cheapest-to-deliver (CTD) bond that has the same seniority as the reference obligation.

Settlement is on the CTD bond within that same seniority — and notice it only cares about seniority!

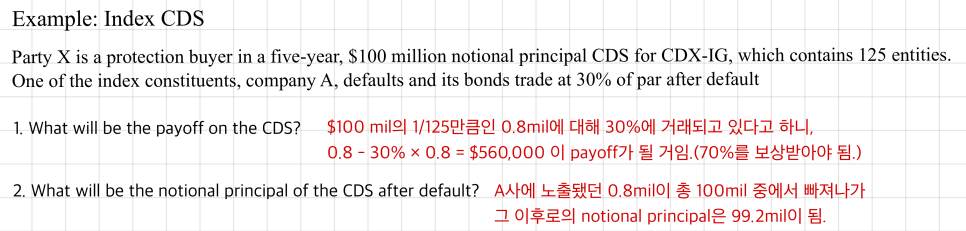

Index CDS

There’s also a thing where they bundle around 125 reference obligations together to create an index.

An index CDS covers multiple issuers, letting market participants take on credit-risk exposure to a whole bunch of companies at once.

The pricing of an index CDS depends on the correlation of default (credit correlation) among the entities in the index.

They say this is the most important point.

If it looks like all the companies in the index would go down together in one big sweep, the premium is high. If their defaults look independent of each other, the premium is small.. that kind of story!

Factors Affecting CDS Pricing

Computing the value of a swap is called swap valuation. So pricing and valuation — don’t mix them up.

OK so, CDS pricing — figuring out the appropriate premium is CDS pricing, and the things that feed into it are Probability of Default and Loss Given Default, that sort of stuff.

But the thing that combines both? That’s Expected Loss (EL), right?

That’s the amount you tack on as the spread!

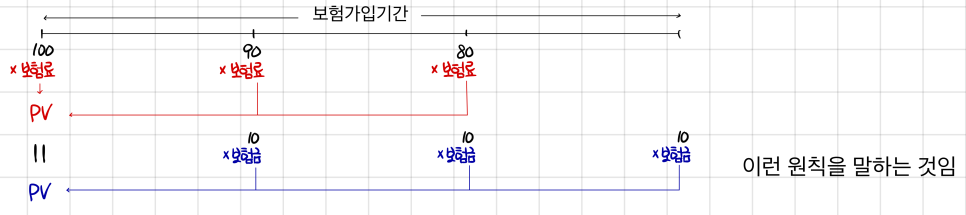

The basic principle behind pricing is

Simple example — 100 people want life insurance, and the insurance company expects 10 of them to die each year over 3 years.

For a single-period CDS, ignoring the time value of money, we can estimate the CDS premium as

Ignore time value, collect this much premium — that’s just the principle of equivalence really..

(Which means the value of a CDS contract at $t=0$ is 0!!)

And then, depending on which way default probability moves, the value drifts in the (+) or (−) direction.

A derivative contract is zero-sum, so if I’m (+), the counterparty is (−).

From the Protection Buyer’s side, a widening spread is a gain. From the seller’s side, a narrowing spread is a gain.

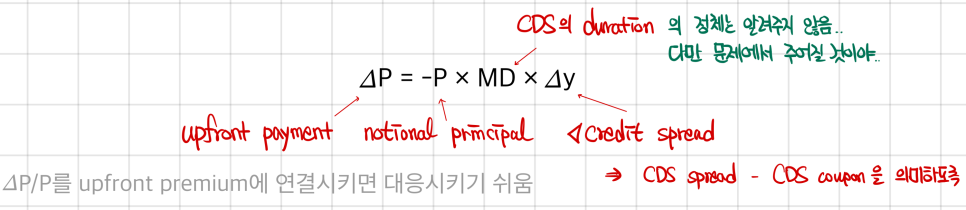

One last thing.. sometimes the first-order sensitivity formula for CDS is written as

What on earth does this even mean…

Remember this one? $\Delta P = -P \times MD \times \Delta y$

That’s the formula saying as $y$ moves up or down, the bond price moves with sensitivity proportional to duration.

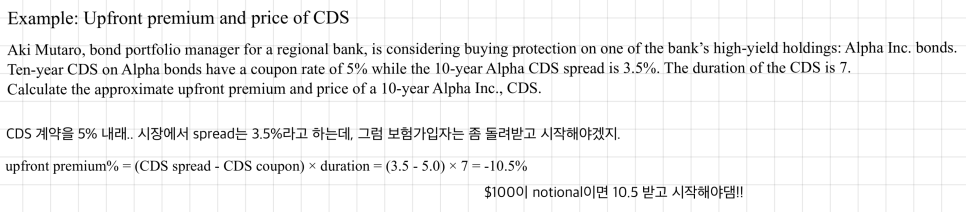

If you treat that movement as the credit spread, then the difference between the credit spread and the CDS coupon is what has to be paid as an upfront payment.

Price of CDS (per $100 notional) = $100 − upfront premium [$]

Normally a CDS price is quoted as a percentage of Notional Principal, but there’s also this way of expressing it like a bond.

CDS Usage

How people use CDS… here’s a quick tour of ways to actually make money with this thing.

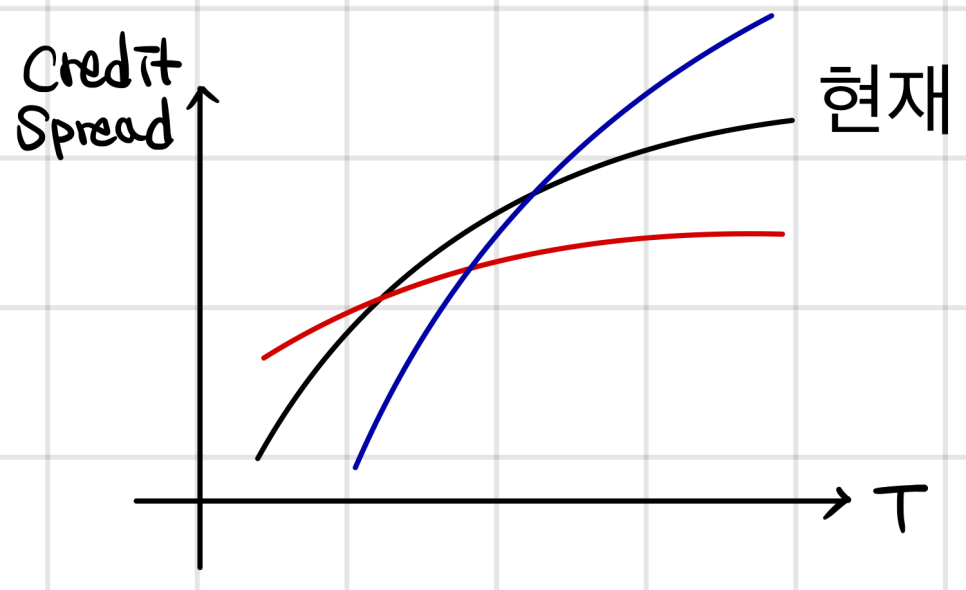

The credit curve is the relationship between credit spreads on different bonds issued by the same entity.

A company has issued bonds, and if you plot the credit spread the market demands across maturities, that’s the credit curve.

Normally, longer maturity → wider spread, so the curve slopes upward.

(Though in something like a financial crisis, the short end can actually blow out wider than the long end.)

Let me list the situations briefly first, then walk through them one by one.

➀ CDS can be used to manage credit exposures of a bond portfolio

➁ A curve trade is a type of long/short trade where the investor is buying and selling protection on the same reference entity but with different maturity

➂ A basis trade is an attempt to exploit the difference in credit spread between bond market and the CDS market

➃ In a leveraged buyout (LBO), the firm will issue a great amount of debt in order to repurchase all of the company’s publicly traded equity

➄ In the case of an Index CDS, the value of the index should be equal to the sum of the values of the index components

➅ Collateralized Debt Obligation (CDO) are claims against a portfolio of debt securities.

➀ In anticipation of declining (increasing) credit spreads,

a manager may increase (decrease) credit exposure in the portfolio by being a protection seller (buyer)

⇒ If it looks like premiums in the market are going to shrink, you become the insurance company so the premium keeps rolling in! That sort of move.

And since a CDS contract can be set up without even owning the underlying asset (naked CDS), basically anything goes! heh

In a Long/Short trade, an investor buys protection on one reference entity while simultaneously selling protection on another (often related) reference entity.

➁ What’s a Curve trade?

Under normal conditions, the spread curve slopes upward, like I said.

If you’re expecting it to flatten —

(meaning: “if it gets through the short term in one piece, the long term should be fine~”)

then you buy CDS on the short end and sell protection on the long end.

If your expectation plays out, you close the position by selling short-term protection and buying long-term protection.

⇒ Curve Flatten Trading

Expecting a steepener? Just do the opposite… heh ⇒ Curve Steepen Trading

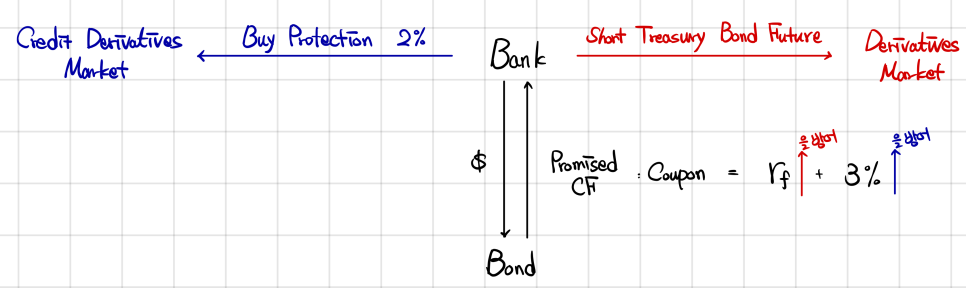

➂ What’s a Basis Trade!

For any given bond, there’s both a bond market and a CDS market.

Say a bank picks up a bond, and in the bond market that bond pays a fixed coupon at risk-free + 3% spread.

The bond price could fall because the risk-free rate rises, so you can hop over to the derivatives market and short government bonds to hedge that piece.

The spread might also widen and pull the bond price down — so to defend against that, you head over to the credit derivatives market to buy protection… and you find they’re only asking 2%?? Oh interesting.

If you put this position on, the risk-free rate is fully offset by the short, and out of the 3% you’re collecting, you only hand 2% to the insurance company (dealer). Clean 1% profit — that’s an arbitrage position. (Of course, in an efficient market the CDS would have demanded 3%.)

(In reality, market spread reflects more than just default risk — liquidity risk, etc. — so they’re not exactly the same thing.)

Anyway, doing arbitrage like this is called a Basis Trade!!

➃ An LBO is when you acquire a company by borrowing money using that company’s own assets as collateral, and using that borrowed money to do the acquisition.

The firm will issue a great amount of debt in order to repurchase all of the company’s publicly traded equity.

A company issuing bonds to buy back its own shares is essentially a recapitalization.. it’s restructuring the capital structure.

When the news drops, this extra debt will push the CDS spread wider because default is now more likely.

Leverage shoots up, default risk creeps closer — but the share price climbs on the back of the buyback.

So, if you see this scenario coming, what do you do?

Slap on a buy-protection position and also buy the stock. Make money on both sides.

* This move where stocks and CDS work hand-in-hand is called an equity-versus-credit trade.

➄ The price of the bundled thing should equal the sum of the prices of the parts.

So if the index traded as a whole and the sum of its individual components don’t line up, an arbitrage opportunity has popped up somewhere.

It’s introduced pretty briefly — just as a concept that exists.

An arbitrage transaction is possible if the credit risk of the index constituents is priced differently than the index CDS spread.

(In practice there’s a lot more to actually pulling this off and it gets messy.. but since the material doesn’t go there.. let’s just leave it at this.)

ex) When you trade A–Z individually through CDS, nobody says “Oh? Buying all of A through Z? Then the protection price has to be tweaked a bit for correlation…” But with an index, the premium for insurance on the whole bundle does bake in the correlation across the names inside it..

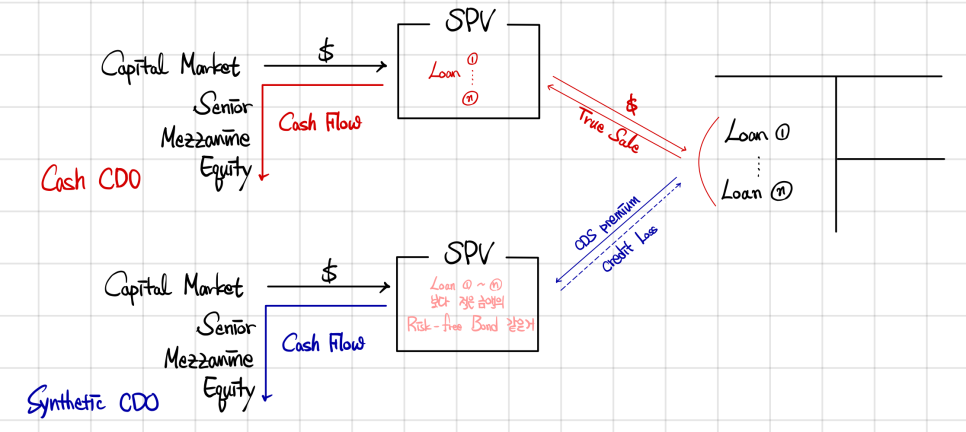

➅ There are two flavors of CDOs — Cash CDO and Synthetic CDO — we saw these back in Level 1.

A synthetic CDO has similar credit risk exposure to a cash CDO, but it’s assembled using CDS instead of debt securities.

If the synthetic CDO can be put together at a lower cost than the cash CDO, investors can buy the synthetic and sell the cash CDO — profitable arbitrage.

A Cash CDO actually holds the loans, while a Synthetic CDO is built out of derivative contracts — but the risk both are taking on is the same.

It’s just that building the trade is cheaper with the synthetic.

Because you don’t have to actually buy everything.

So thanks to that price gap between the two,

Buy the relatively cheaper Synthetic / Sell the Cash CDO

and you’ve captured an arbitrage opportunity.. that’s about the level of understanding we need here.

(You stack insurance on top so you make money regardless of credit risk~)

Originally written in Korean on my Naver blog (2024-12). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.