Investments in Financial Assets

A casual breakdown of the three types of intercorporate investments — financial assets, associates, and subsidiaries — and how to tell them apart on exams and in real life.

Chapter 1. Intercorporate Investments

So three flavors:

i) Investment in financial assets — you bought it purely to flip it. Pure exit play.

ii) Investment in associate — you bought in to get a seat at the table, exercise significant influence.

iii) Investment in subsidiary — you bought in to control the thing.

For ii) and iii) — at exactly what point does “significant influence” kick in, and at exactly what point are we calling it “control”??

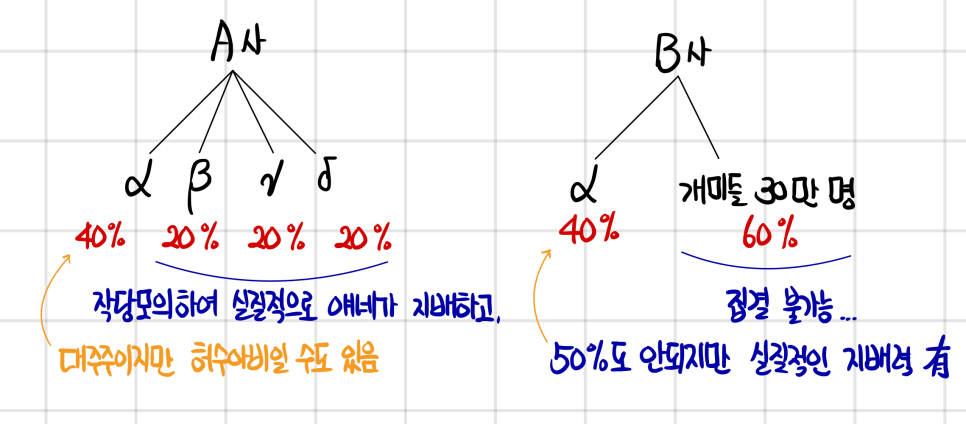

For exam purposes, unless the question tells you otherwise: 20%–50% voting rights = exercising significant influence (associate), above 50% = control (subsidiary). Let’s lock that in as the rule of thumb.

In real life though? Actual accounting standards don’t say “use these numerical cutoffs.” Quantitative judgment based on percentages is not the priority — qualitative judgment is.

→ Translation: the standard basically says “y’all figure it out” lol.

Take LG and SK. LG holds LG Electronics and LG Chem at around 30% and applies equity method as associates. SK holds SK Telecom at around 30% and consolidates it as a subsidiary. Same ballpark stake, totally different treatment.

Honestly, telling associate vs. subsidiary apart is supposedly really hard in practice. You’d have to look at governance, the average percentage of yes-votes that actually show up at the AGM, the trend over time… a whole pile of stuff to think about.

So on the exam, when you see something like “they only hold under 20%, but they have the right to appoint Board members” — that’s the question telling you “this isn’t a Fair Value problem, this is equity method, dummy~^^”. Apparently.

Let’s run through a few of those signals.

Significant influence can be evidenced by:

i) Board of directors representation ii) Involvement in policy making iii) Material intercompany transactions → e.g., I only own 10%, but if I cut off your raw materials, you’re cooked… iv) Interchange of managerial personnel v) Dependence on technology

There are also cases — among foreign listed corporations — where the exercisable stake is capped for foreigners. (Korea has this too. Defense and similar industries — can’t have foreigners practically running the show.)

So however much I invest, if there’s a hard cap on the voting rights I can actually exercise, neither control nor influence is on the table. Period.

In the US, dual-class voting shares are super common. So in terms of equity stake you might get 30% of profit distributions while exercising basically zero voting rights. Or the opposite.

(Jack Ma is the textbook example for this… voting rights → Jack Ma, profit distributions → SoftBank…)

Why does the dual-class voting system even exist, you might wonder?

The whole joint-stock company thing was probably set up so that when a company needs cash, it can blast out a rights offering to a bunch of unspecified shareholders and raise money fast. But — say my stake in my own company is 30%, and I need 100 billion for new-business CAPEX.

If I raise it through a regular rights offering?? My ownership gets nuked into the floor and management control could fly out the window..?

So am I supposed to just give up the new business…?

Nope — the dual-class voting system exists precisely so you can raise the capital and keep running your own company… heh.

(Wait, isn’t this already too interesting for lecture one??)

One more thing. Up above I made it sound like equity method only applies to associate investment shares — but there’s actually one more case → it’s called a Joint Venture.

(Hmm… if you’ve got joint control via a JV, then regardless of ownership percentage, you classify it as joint venture investment shares and apply equity method… T_T)

For this one, just take “equity method gets applied” and move on… that’s about the depth we need. One read-through and we’re good~

(Honestly, finishing off equity method and consolidation in a few hours of lectures is kind of a joke lol)

OK so the real content kicks off from here, and we’re not starting from ii) or iii) — we’re starting from i), financial assets!

Because before anything else, we need to know what to do when we just up and bought some stock!!!

Investment in Financial Asset

Now let’s walk through these one by one from here…

But — when you start studying for the CPA, you take Accounting Principles, then move on to Intermediate Accounting, and the content here — which is the first major boss fight in Intermediate Accounting (financial assets) — gets covered in the CFA book in like 2 sheets of A4. Wow.

Anyway, let’s go!

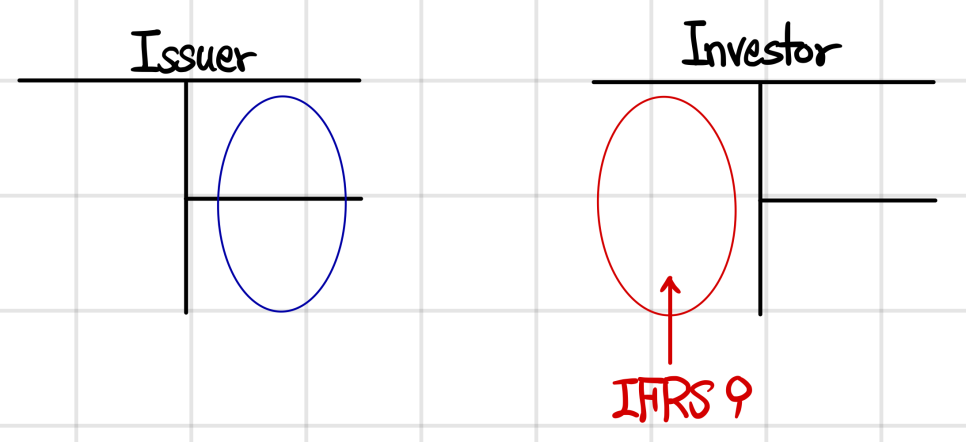

Ideally, the accounting on the side receiving the investment and the side making the investment would be symmetrical… and historically it kind of was. But the “financial assets” recorded on the Investor side got reworked and somewhat simplified in 2019 under the name IFRS 9, apparently.

Meanwhile, the revision to accounting on the Issuer side for the money raised? That one is supposedly running behind…

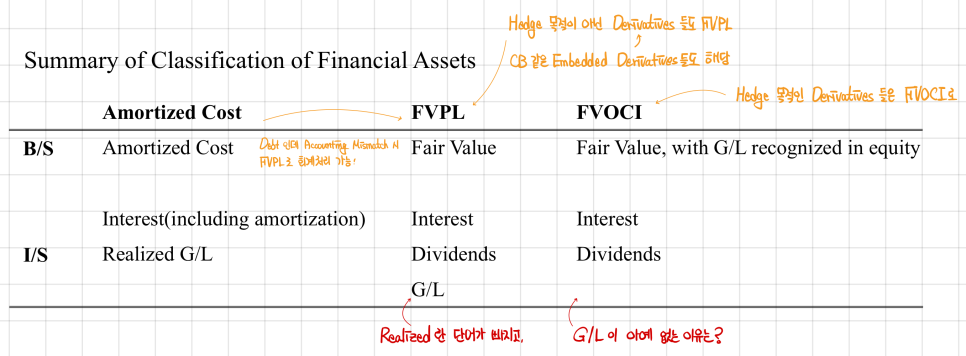

So what we’re studying here is the financial-asset accounting treatment under IFRS 9.

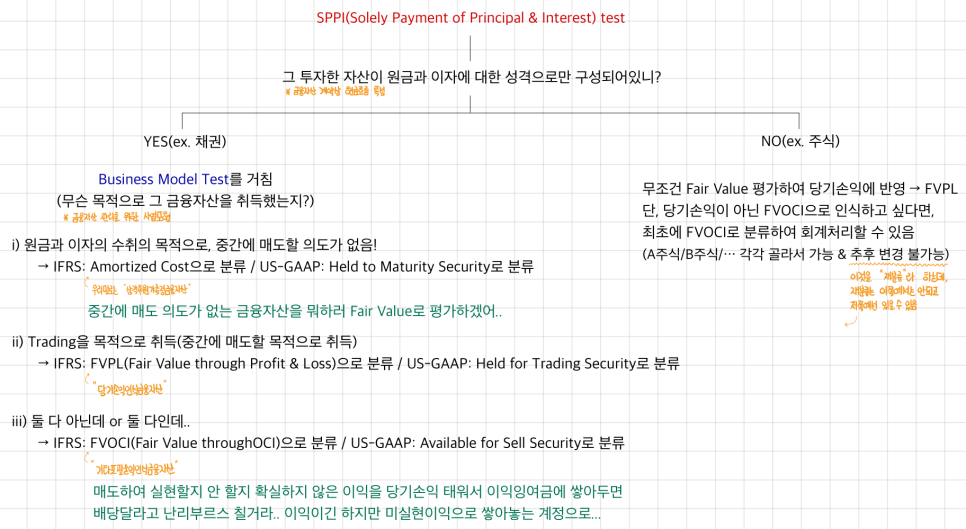

Setup: the Investor invested in the Issuer, but there’s no influence and no control — that’s when financial-asset accounting kicks in. And even within financial-asset accounting, there are subdistinctions.

How those distinctions get drawn — this came up back at Level 1 as the SPPI test (Solely Payment of Principal & Interest test).

No need to dredge up how you studied it back then. We’ll go deeper here!

This is the investor side. The issuer side would have a pile of classifications — corporate bond, common stock, CB, etc. — but none of that is what we’re covering here, right?

Investor side got simple. Issuer side is staying complicated.

So how does a CB investor record it?!

→ SPPI test: “there’s principal and interest, and also a conversion right.”

Then it’s not solely principal and interest, so go to the right! That’s how it works… heh.

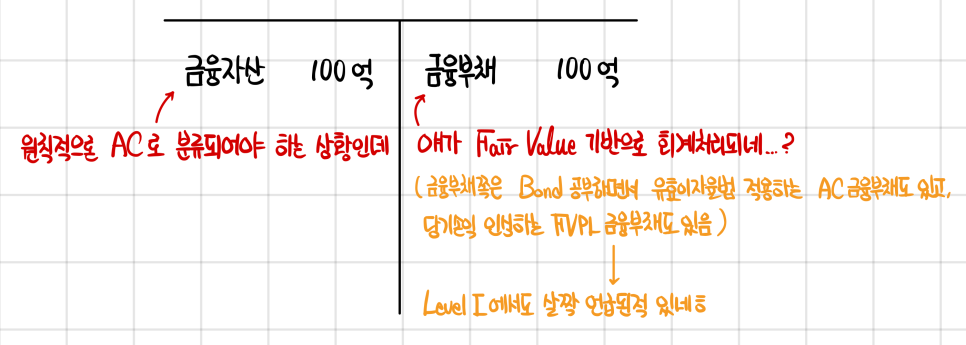

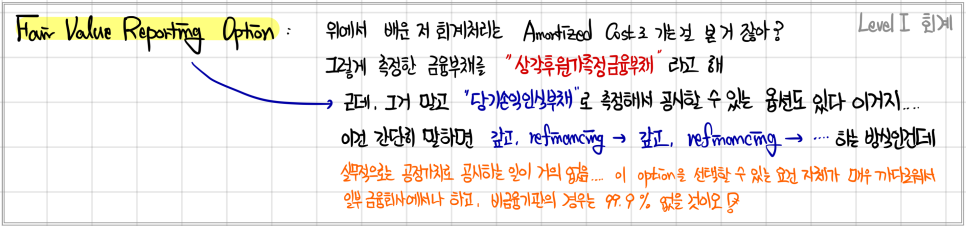

The “accounting mismatch” topic comes up… honestly, all you actually need is “when accounting mismatch happens, AC can be designated as FVPL”… heh.

The situation’s like this — say I borrow 10 billion from a bank (financial liability) and use that to buy 10 billion in bonds.

The two are linked, but on the liability side it runs through current P&L based on FV, while on the asset side it has nothing to do with FV. That’s what “accounting mismatch” is, and in those cases:

“In a situation where forcibly designating a financial asset that should in principle be classified as AC or FVOCI as an FVPL financial asset would eliminate or significantly reduce the accounting mismatch”

— in that kind of situation, you can designate the financial asset as FVPL!

(But: you can only designate at initial recognition, and once designated FVPL, reclassification is absolutely off the table.)

* The gray text — feel free to read it with squinted eyes! You don’t need to lock in on it.

The “Summary” bit too… too long to explain, but you can’t get the summary wrong either, so by deleting the word “realized” and stripping G/L entirely — he dodged making his own mistake…

But this part isn’t tested either, so just read it once for the gist and move on.

“The story of FVOCI that can / can’t be reclassified”

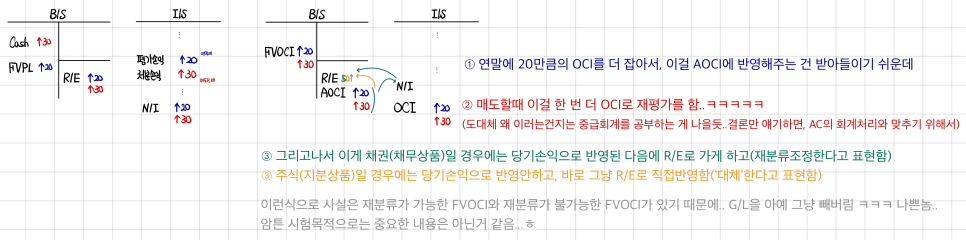

Say you bought a financial asset and decided to apply FVPL accounting, and what you bought at 100 became 120 at year-end, and then the next year you sold at 150.

Since it’s FVPL, you mark to Fair Value at year-end and bump it up to 120, and at that point the 20 runs through current P&L and gets reflected in R/E (even though it’s not actually Realized, it goes through the I/S~).

Then when you sell at 150 next year, the 30 gets booked as disposal gain/loss, also runs through current P&L and ends up in R/E.

End result: bought at 100, sold at 150 — all 50 went through current P&L and all 50 landed in R/E. Correct! Self-evident.

But when it’s FVOCI, here’s what happens:

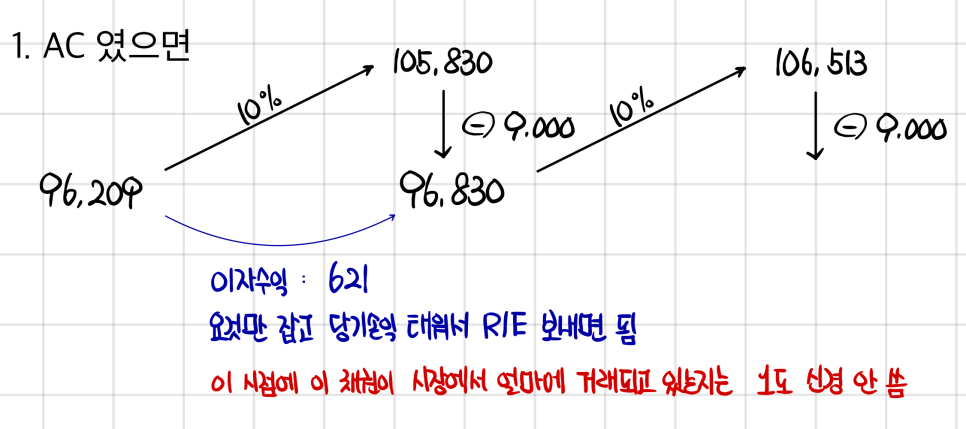

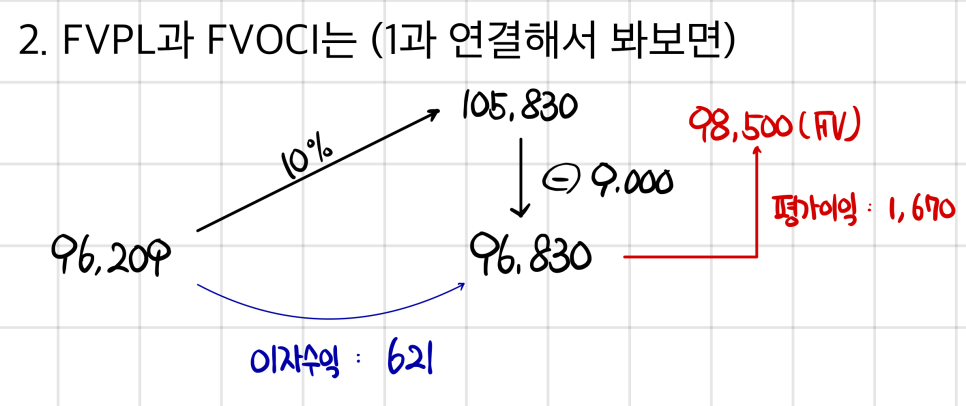

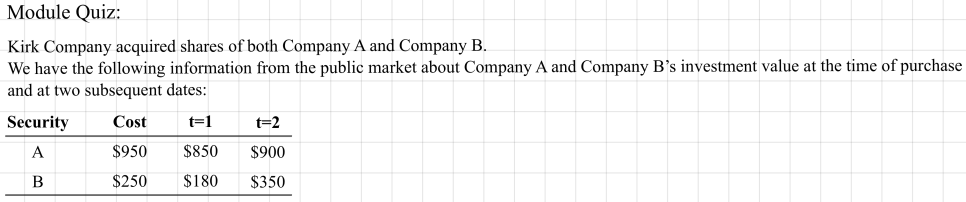

Let’s do an example.

Just plow through it with effective interest rate method treatment and that’s it.

For FVPL — both the 621 and the 1,670 run through the I/S and get reflected all the way to R/E.

(Technically the effective interest income isn’t recognized — it shows up as coupon interest — but the effect is the same either way.)

For FVOCI — the 621 in interest has to go through current P&L, and the unrealized-feeling valuation gain goes through OCI and lands in AOCI…

Reclassification Under IFRS 9

For investment shares, we said you can elect FVOCI right at the start, and once you commit to FVOCI you absolutely cannot switch to the other option, FVPL.

But for investment bonds — reclassification is allowed, limited to the case where the Business Model changes!

Just take that fact and move on…

Going any deeper… way too much volume, and it’s beyond exam scope!!

Loan Impairment Under IFRS 9

Zero chance of this on the exam, so just skim the keywords mentioned here and move on, that’s it…

A key feature of IFRS 9 was that the incurred-loss model for loan impairment got replaced by the expected-credit-loss model.

The new criteria result in earlier recognition of impairment.

Before, only what had actually been incurred got booked. IFRS 9 saying “you also have to book expected” hit financial institutions especially hard, apparently.

Situations where estimated future cash flows shrink include: the issuer experiencing significant financial difficulty / contract violations like default or delinquency / increased likelihood of borrower bankruptcy / …

In those cases, you bring the decreased cash flows to present value compared to the originally estimated cash flows, run impairment loss through the I/S, and on the B/S you record a loss allowance as a contra account to the financial asset so the net amount shrinks… that’s the “credit-impaired financial assets” content.

Originally, up until around 2011, expected credit loss was being used. Then around 2011 it flipped to Incurred loss. Then in 2019 it flipped again.

The interesting thing is — back in 2011, suddenly stripping out “expected” and saying “only book incurred as loss allowance” caused Assets to suddenly jump way up.

When that flipped back, the reversal amount would have piled into R/E. Because of this, financial institutions’ financial structures suddenly improved drastically.

But the FSS (Financial Supervisory Service) said:

“We are concerned that the banks’ financial structures may weaken because the loan-loss-provisioning method has changed from the concept of expected loss to the concept of incurred loss.”

What?!!? What does that mean?!?!

The actual context: “we’re concerned that suddenly huge dividends are about to fly out.”

(Because at the end of the day, the bonds are still sitting there and only cash would be whooshing out the door.)

So to keep that R/E bump from being paid out as dividends, instead of letting it pile into undistributed retained earnings, they stacked it into an account called “loan loss reserve.”

So when you’re picking apart a B/S and you spot an account called loan loss reserve — please don’t get too flustered~ that’s why it’s there~~

(Side convention thing: the account that impairs/reduces financial assets is normally “impairment loss / loss allowance.” But specifically for receivables (trade receivables, accrued receivables, loans, etc.), the accounts “bad debt expense / allowance for doubtful accounts” get used instead. There’s no rule saying it has to be that way — it’s just convention… (cf. trade receivables are also a type of AC financial asset.))

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.