Equity Method Accounting: Fundamentals

A breakdown of why associate stocks skip fair-value measurement and how the equity method pipes B's net income straight into A's books to close the dividend-manipulation loophole.

Investment in Associates — that’s associate stock. The case where significant influence exists.

Usually 20%–50%. But even below 20%, if some special right is in play, it can still count.

OK so. Remember the financial assets we looked at earlier? Pretty much all of them — except the Amortized Cost ones (AC financial assets) — got measured at FV.

The whole point of FV is: I’m planning to realize this thing in the market. So I’ll record it on my F/S at whatever value the market says.

But associate stocks? These are affiliate companies, literally. You’re not holding affiliates so you can flip them.

(And if you are holding them for an Exit, they don’t get classified as associate stocks in the first place.)

So — these don’t get measured at fair value. The accounting treatment we use here is the Equity Method.

Let’s get the logic of the equity method down first.

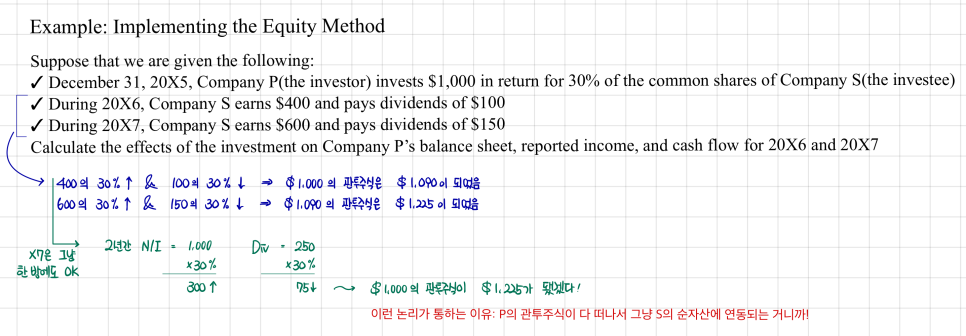

Say A buys a 30% stake in B for 150. On A’s B/S, Investment in Associates pops up at 150. Now if B’s performance that year comes in at Net Income of 200, an amount equal to A’s ownership share gets linked into A’s performance.

Now hold on — if this had been one of the regular financial assets we studied earlier, how would B’s performance have shown up on A? That 200 wouldn’t have flowed directly into A’s I/S. Instead, B’s good year would push B’s stock price up, and that’s how it would have moved A’s financial asset. And of course, if B paid a dividend, A would record it as dividend income on its I/S.

So why do we treat associates differently?

Because A is in a situation where it exercises significant influence over B. A can basically make up its mind and go for it — pull dividends out of B whenever A feels like it.

Which means A can absolutely manipulate its own Net Income. Our year is looking good? Hold off on B’s dividends. Our year is looking bad? Yank dividends out of B early.

So the accounting move here is basically: shut that loophole. It says, “Look — whatever’s accumulating inside B that belongs to your ownership share, recognize that as your performance, right now."

But wait — does actual money come into A right now?!?! → Nope nope nope nope. It’s purely accounting profit.

To get a closer feel for how this accounting profit ends up on the books,

The moment you invest in an associate, my straw goes straight into the net assets on the associate’s B/S.

If those net assets go up, Investment in Associates goes up. If they go down, mine goes down. That’s the equity method!!

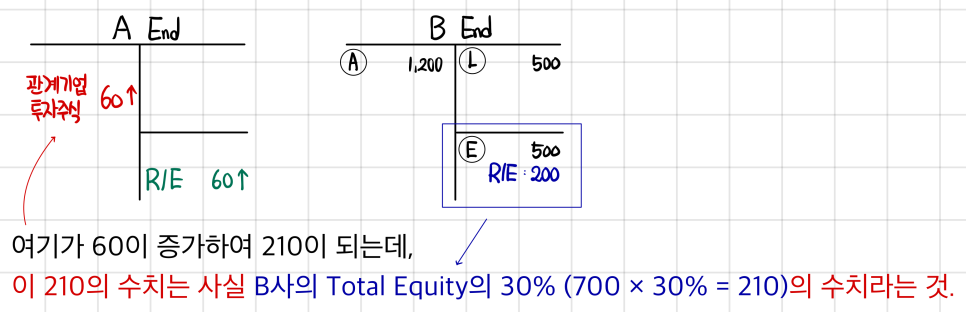

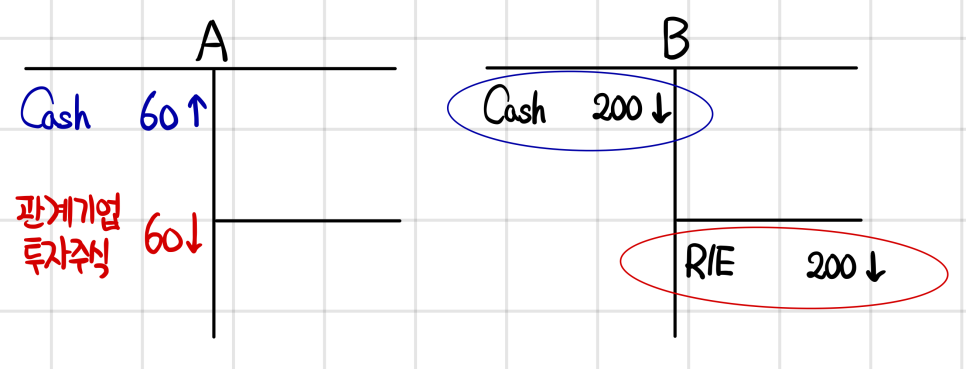

OK now let’s say next year, B pays out that whole 200 of Net Income as dividends.

B’s retained earnings drop by 200. Oh! B’s net assets just shrank — so A’s Investment in Associates has to come down right along with it. But 30% of the 200 in dividends comes in to me as cash dividends, so cash goes up by 60.

So the equity method income of 60 that already got recorded — it wasn’t recorded at the moment the dividend was paid. It was recorded ahead of time, back when B first generated the profit that would later be available for dividends.

If this had been a regular financial asset instead of an associate, that 60 would only have hit the books when the dividend got paid.

In other words, what equity method income produces is something like “unrealized gains/losses” on A’s side.

Which is why that R/E that just bumped up by 60 doesn’t make it into distributable retained earnings.

The Commercial Act explicitly blocks equity method income from being paid out as dividends.

So what happens if B falls into capital impairment and its net assets go negative..?

Let’s say B didn’t post Net Income of 200 — instead, B posted a loss of 600. Then 30% of (600) = (180), which should flow into A too?! But here’s the problem. Investment in Associates is 150. Apply (180), and you’d be recording an Asset of (30)..

Can you record an Asset (an asset!) as negative in accounting..? No no no no no no. Negative assets are not a thing in accounting. The reason is, in accounting an asset is defined as “a present economic resource controlled by the entity as a result of past events” (this is stuff I studied on the CPA side, so I’m graying it out..) Where economic resource means “a right that has the potential to produce economic benefits” — and if you write that right as a negative, the logic spirals into “shareholders have to spit something back out,” which breaks the limited liability of a corporation. So accounting just doesn’t define negative assets.

So the conclusion is: Investment in Associates only reflects equity method losses down to 0.

Wait so — there could be cases where the actual loss is like negative 100 billion, but only negative 1 billion shows up on the financial statements?? Yeah. Which is why for Accumulated Loss, you absolutely, absolutely, absolutely have to disclose it in the notes. There’s a real chance of hidden deficits sitting underneath..heh

If the investee’s losses reduce the investment account to zero, the investor usually discontinues use of the equity method.

The equity method is reduced once the proportionate share of the investee’s earnings exceed the share of losses

that were not recognized during the suspension period.

Fair Value Option

US-GAAP allows equity method investments to be recorded at fair value.

Under IFRS, the fair value option is only available to venture capital firms, mutual funds, and similar entities.

For investment companies, even if they pick up 20%–50% of someone’s shares, that’s for Exit purposes anyway, right? So for those kinds of entities, they’re allowed to apply equity method treatment at Fair Value. But it only gets granted to a really narrow set of industries, so it’s probably fine to just go “huh, that’s a thing” and move on.

(Side note: sometimes when you flip through a quant investing book, you’ll see them filter all holding companies out of the universe — and the reason is that even though a holding company’s financial statements look similar to other companies’, it’s a stretch to compare them apples-to-apples.. that’s why they do that kind of thing.)

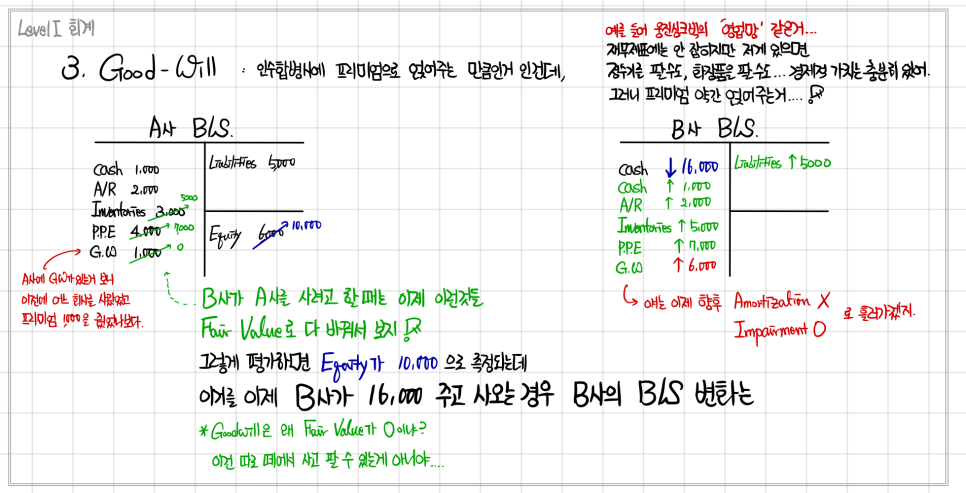

So from here on, instead of A buying 30% of B’s 500 in net assets for 150,

we’re going to look at cases where A pays more on top of that.. cases where a premium is tacked on. I had a brief run-in with the account name Goodwill back in Level 1 — let’s quickly look at how it showed up there, and then move on to the next one!

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.