Equity Method Accounting: Advanced Topics

Real-life equity-method: BV ≠ FV, a control premium gets stapled on top, and you've gotta reconstruct income from an FV lens — exactly what the CFA exam tests.

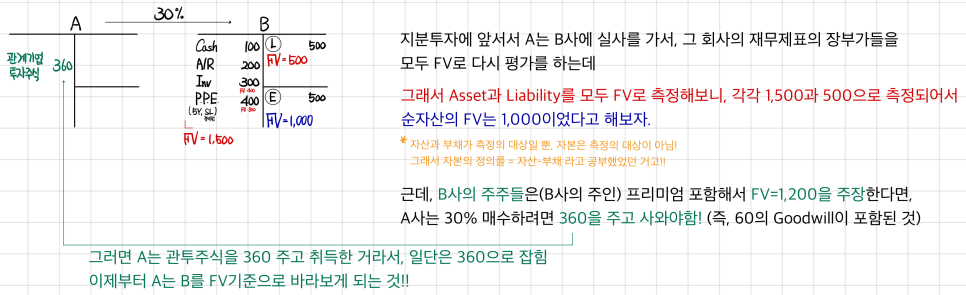

OK so the case we just saw assumed Book Value = Fair Value for Company B. But come on — in real life, when Company A buys Company B, the basis isn’t BV. It’s the FV at the moment of acquisition!!!

And here’s the thing: when you’re not just nibbling on a small stake but actually swallowing a big chunk of the company, the seller is going to want more on top of FV.

The vibe of the conversation: “Ohhh my~ the fact that you’re buying that much means you’re planning to step into management here too, riiight? Sounds like you’ll need to pay a little extra for that management-participation slice.. we good?”

In basically every transaction that looks like this, a control premium gets stapled on.

So let’s look at this kind of case (and obviously — this is the only kind of case that’s ever going to show up on the exam).

Two steps are getting smushed together here. ➀ From here on, BV≠FV is fair game, and the basis has to be FV. ➁ Whatever you paid on top of that FV gets booked as Goodwill in character!!

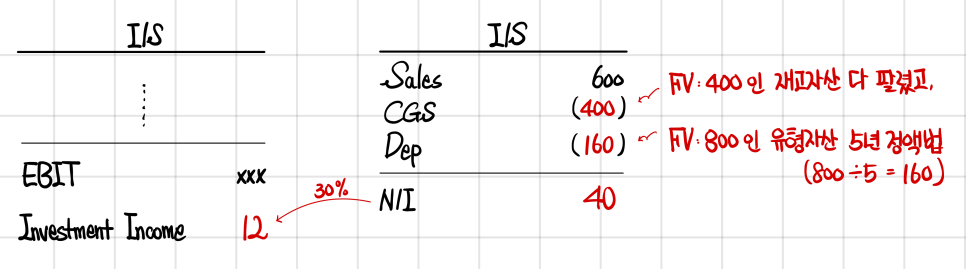

And let’s say B’s performance comes in like this — all inventory sold, cash revenue 600, no other expenses except depreciation — and Net Income shakes out to 220. Cool. But hold on. You cannot turn around and use that 220 to compute equity-method income!!! Because A isn’t looking at B on a BV basis. A is looking on an FV basis. So you’ve gotta reconstruct the I/S from that FV lens.

I really didn’t want to get into this section, but now that I’m down in the consolidation chapter.. I had to scroll all the way back up here to write it (sobbing) (real talk: I was writing the consolidation part in gray text and bounced back up here lol).

Originally, when you study equity-method accounting, there are 3 things to keep in your head total. If I sort which parts of those 3 actually matter for CFA studying, it shakes out like this..

➀ BV≠FV: the part that gets distorted because of over/understatement of net assets ← Heavily tested in the CFA curriculum ➁ The part paid on top of FV: Goodwill ← Heavily tested in the CFA curriculum ➂ Intercompany transactions with associates (up-stream & down-stream) ← NOT really tested in the CFA curriculum

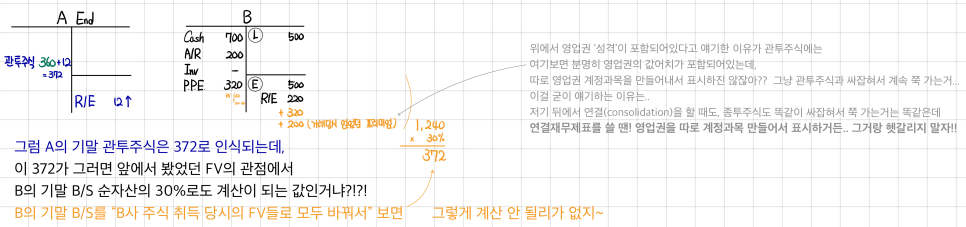

For A, yeah — Goodwill is $5,000 and so on. Easy enough.

From B onward is where it actually gets real, but before we dive in for real, keep this stuck in your head.

(I really should switch to Gothic font lol. Naver doesn’t have Gothic font;;)

The equity method, at the end of the day, is just 2 things:

➀ Whatever profit the associate posted — my share of it is mine! ➁ When a dividend gets paid, it offsets!!

That’s it. The whole thing. Two bullets.

BUT — when you recognize income → it has to be income from my perspective, i.e. through the FV-at-acquisition lens!!!

That’s the whole game.

OK first, let me work out the income from what I (Red) actually see. Blue’s out here saying its Net Income is $100,000, but yeah.. that’s what you think.

From where I’m standing, P.P.E. is marked up by $50,000, so the extra depreciation on that markup — $50,000 over 10 years straight-line, a.k.a. $5,000 — should’ve been expensed on top.

So I’m knocking another $5,000 off the Net Income *you're* quoting me!!! Which means Blue's N/I as *I* see it is $95,000, and 30% of that — $28,500 — is mine!!!!

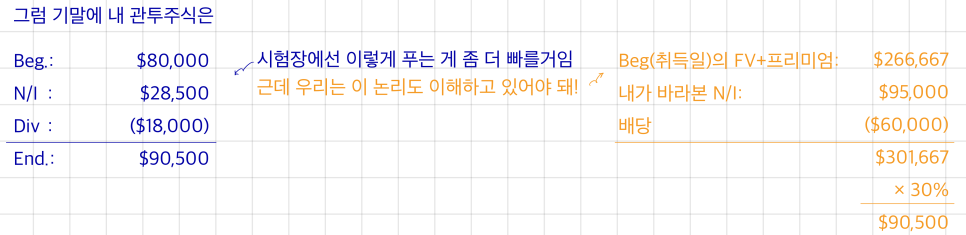

Since the CFA exam usually asks about the following year, this approach will carry you through exam day.

If this were a CPA problem, they usually push it to the year after next — like x3, x4 — and if you don’t have the right-hand side absolutely cold, there is no way you’re solving it in time..

For us though, the exam usually stops right about here!!

The stuff past this point is what crawls out when they really crank the difficulty knob up..?

Well, just how hard can it possibly be..??? Yeahhh yeah yeah, very hard lol.

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.