Equity Method Accounting: Intercompany Transactions and Impairment

A casual breakdown of how intercompany transactions mess with your equity-method income — upstream, downstream, unrealized profits, and when impairment comes knocking.

Transactions with the investee

When there’s an intercompany transaction with an associate…

Example time. Imagine Celltrion doesn’t trade with anyone else — it just sells everything to Celltrion Healthcare, and Celltrion Healthcare is the one with the exclusive sales rights, pushing the goods out into the world from there. (Disclaimer — these two aren’t actually associates, heh. I’m just using them as a vibe-check example, heh.)

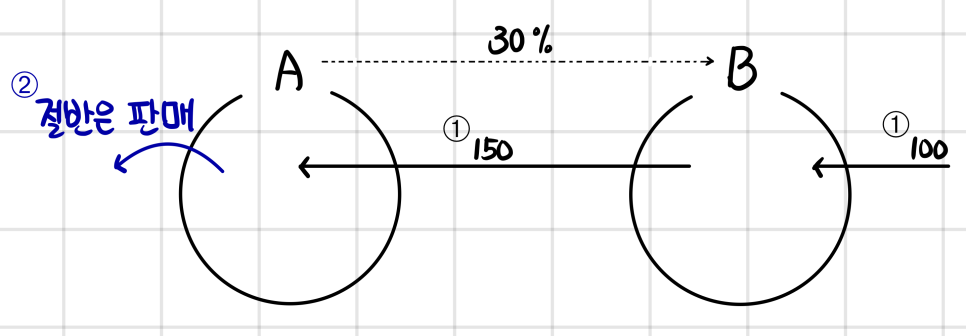

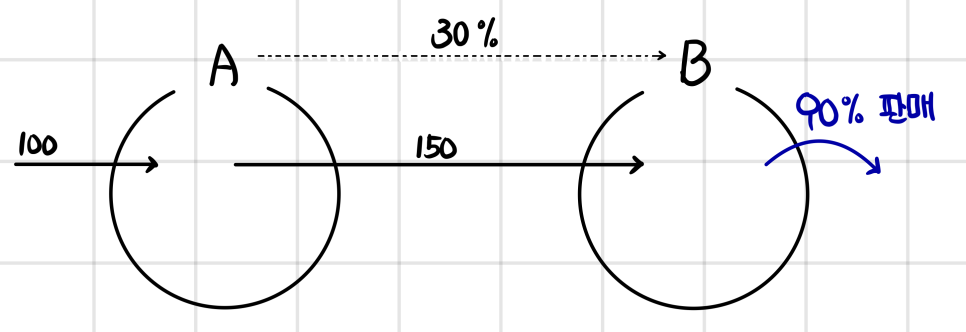

➀ A owns 30% of B, and because that puts it in equity-method-investment territory, A is doing equity-method accounting on B. Now say B bought some goods for 100 and sold them to A for 150. And by period-end, A hasn’t sold any of it onward to anybody else.

OK so now period-end rolls around, and we sit down to do the equity-method accounting. The point is — you can’t just grab 30% of B’s Net Income and slap it onto A’s equity-method investment line. These two are tangled up in each other’s pockets. All that actually happened is some inventory walked from B’s warehouse to A’s warehouse — and yet, because of that walk, B’s books are showing an extra 150 − 100 = 50 of profit.

And we’re going to take that and reflect it as B’s profit in A’s equity-method investment??? Come on. So out of the profit A sees flowing out of B, that 50 worth shouldn’t be reflected. There’s no economic substance to the transaction. (No economic resources actually got transferred ← that’s literally the definition of revenue.)

Then flip it — what if A had sold everything onward???

In that case, all the goods truly made it out into the real world, so we just simply go: yep, recognize all of B’s profit now~! When everything’s realized, there’s no equity-method income to adjust!!!

➁ Now say A has only moved 50% of that inventory out the door externally. The lingo for this is “the intercompany transaction has been realized,” and when we’re stripping B’s Net Income down to feed into A’s equity-method investment, 25 of the 50 is now realized — so that 25 does get reflected in A’s equity-method investment.

And the remaining unrealized 25 (the Unconfirmed Profit) — that gets peeled out of the version of B’s Net Income that A sees, and then reflected. And since N/I gets multiplied by the ownership % to become equity-method income —

alright alright. Let me just say it cleanly in equity-method-income terms:

“the amount you reverse out of equity-method income = total intercompany transaction gain/loss of 50 × unrealized ratio of 50% × A’s ownership %”

— and that amount is what gets subtracted back out (−).

This kind of intercompany flow, where the sale moves from the smaller side up into the bigger company, is what we call Up-Stream (upstream intercompany transaction).

So obviously there’s a Down-Stream version too.

Cutting straight to the punchline — it’s the same. The amount you yank out of equity-method income is identical: total intercompany gain/loss of 50 × unrealized ratio of 50% × A’s ownership %.

CFA isn’t an accounting exam anyway… so we don’t need to go super deep here, ugh. Let’s just memorize it, heh! Honestly, even under current standards, the rule says to adjust equity-method income by the ownership % regardless of whether it’s upstream or downstream!!!! (There are other theoretical methods too, sure.) This stuff does hit consolidated financial statements differently depending on up vs. down, so it’s actually a hairy topic, lol. But for equity method? Eh, just rough it, heh heh.

For this part, just lock in: “Ah, in accounting, equity-method accounting (and consolidation, similarly) does this — it prevents intercompany transactions from being reflected.” That level of grasp is plenty.

And of course, if it does show up on the exam, you just calculate all the equity-method income as usual, and then on top of that it’s literally just one more line: “unrealized gain/loss × ownership %.” Not exactly impossible, heh.

Impairments of investments in associates

Equity-method investments also get impaired — when you decide the associate has gone down the tubes.

“Gone down the tubes” means: if FV drops below the BV of the equity-method investment, you rewrite the BV down to that fallen FV, and the loss gets booked as an impairment loss (I/S).

But here’s the important bit:

In the consolidation chapter coming later, when we talk impairment, consolidation creates a separate Goodwill account and does impairment accounting on that piece separately,

whereas equity-method investments don’t carve out and manage G/W separately. So it’s not “go pull out the goodwill chunk and impair that” — it’s just: impair and write down the equity-method investment itself!!! I think going this far and moving on is totally fine~

Now compare this to what we studied before — just plain shareholdings where there’s no significant influence and no control. Those were treated purely at FV, and there was zero concept of Impairment in there.

But for equity-method investments, the verdict is: yes, we do apply impairment accounting by comparing against FV.

Why though??? Let’s think about the underlying question for a sec.

If some company is bleeding losses left and right, but there’s still hope for the future, then the FV probably isn’t going to nosedive, right??

It’s the stock that’s losing money and has no future — that’s the one whose FV gets smashed too, which is what triggers impairment recognition on the equity-method investment. So at the end of the day, this impairment recognition is basically the principle of: “let’s go ahead and pre-reflect future losses, and account for Assets as conservatively as we possibly can.”

When you think about it — on the Asset side, basically every account has some flavor of impairment (= allowance for bad debt) accounting. But Liabilities? Nothing like that. You’re not gonna sit there impairing your accounts payable like, “Oh wait, maybe my obligation to pay later might shrink a bit?!” lol nope. (✴ On the liability side, impairment-ish stuff does show up in cases like court receivership where debts get written down — there we do talk about impairing Debt.)

But hold on — would creditors and shareholders both actually be cool with this kind of accounting?

From the creditor’s seat — absolutely amazing. Conservative accounting keeps R/E as low as possible, which prevents that R/E from leaking out the door as dividends, which protects the creditor’s slice.

But from the shareholder’s seat — conservative accounting → R/E ↓ → dividends delayed → wait, why would they sign off on this!??!

→ The accounting scholars’ answer: “Management, who were appointed by the shareholders, are giving them advance notice that shareholder wealth is being eroded — which makes shareholders pump the brakes on dumping more capital into a sinking business,

so it’s perfectly acceptable from the shareholder side too.” Management’s also incentivized to not waste the company’s resources. And yeah, of course there’s the whole Big Bath thing — where companies game this and book massive impairments on stuff that hasn’t actually gone down the drain — but what in this world only has upsides.. that’s just the abuse case, what can you do.

And that’s a wrap on equity method!

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.