Proportionate Consolidation

A quick breakdown of proportionate consolidation — folding in assets, liabilities, revenues, and expenses at your exact ownership %, and why accounting standards don't actually use it.

If A buys, say, 80% of B’s shares, then A is the controlling company (parent), and B is the subsidiary.

And for that subsidiary — the rule says: Consolidate.

Hold on. Before we dive in — what was the M in M&A again?

Merge = merger. So if A absorbs B, B is gone. Doesn’t exist anymore. The two companies fuse into one and march forward as A. Merge isn’t “buying 80% or 60%” — it’s swallowing the whole thing, period.

Then the A in M&A is Acquisition — that’s buying a stake.

The acquired company is still alive! You’re just grabbing management control. After the deal, they keep operating separately as A and B.

The “consolidation” we’re studying from here on is on the Acquisition side.

When control is acquired via Acquisition, the accounting treatment says: consolidate — and that’s what we’re about to unpack!!!!

Equity method accounting follows the Equity Method, right? OK.

And the deal with consolidated financial statements is — preparing them follows the Acquisition Method.

But before we charge straight into the acquisition method, let’s warm up with proportionate consolidation first — same vibe, somewhat easier logic.

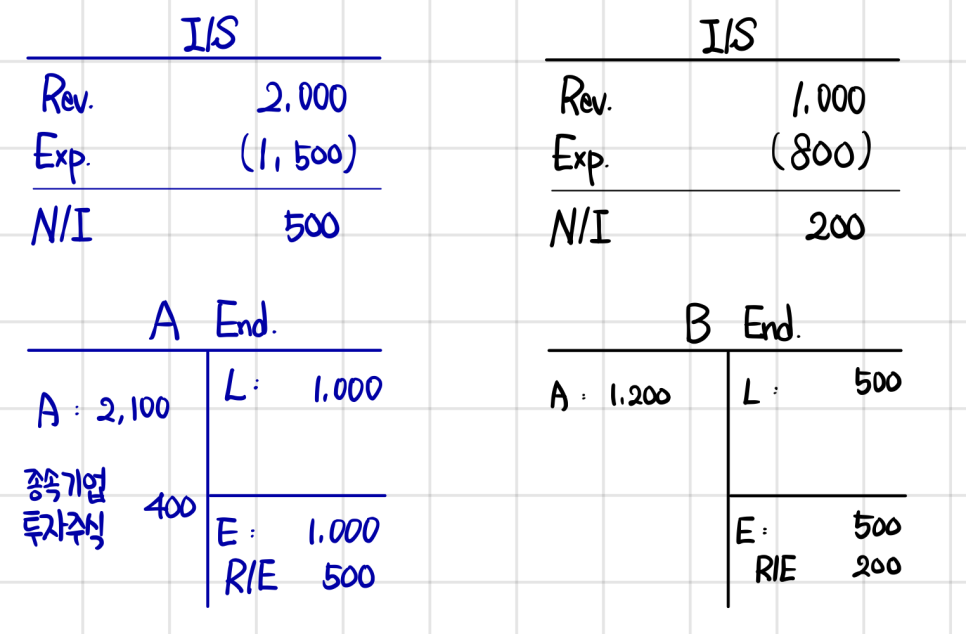

We’ll start step by step from the case where BV = FV.

So say B has BV = FV, and we picked up 80% of 500 for 400.

A’s been running its own race this year, B’s been running its own race this year — so we’ve got two sets of standalone numbers like below. End-of-period financial statements look like this:

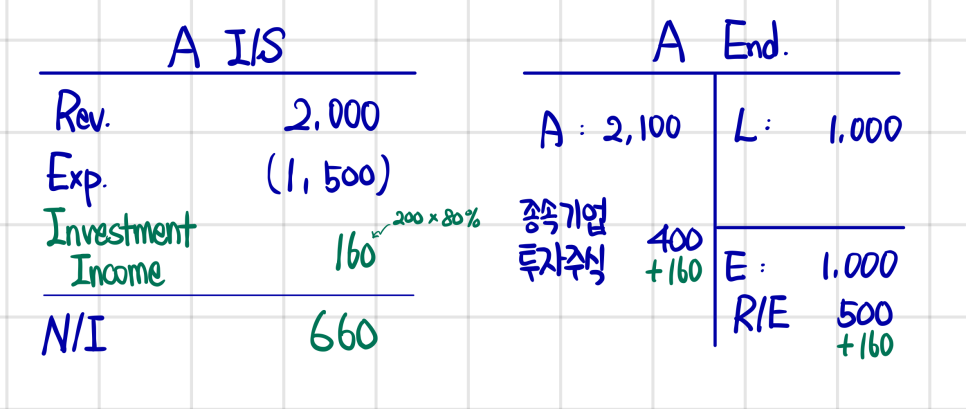

If you treat it with the Equity Method —

(The exam loves asking equity method vs. consolidation!!)

OK, now consolidation.

Consolidation under control takes the perspective of “One Economic Entity.”

So that 400 sitting there as “Investment in Subsidiary”? It was basically saying “80% of B’s net assets is mine.” And what says “80% of net assets is mine”? → 80% of B’s Asset 1,000, which is 800, is mine → 80% of B’s Liability 500, which is 400, is mine — and when you consolidate by swapping it in like this, the parent’s “Investment in Subsidiary” gets eliminated and the line items get flipped over like so. (Honestly — 80% of B effectively does belong to A, right..?)

The I/S follows the same logic — flip all of B’s revenues and expenses over at 80%.

The Ending B/S? Same deal — flip everything at 80% by the same principle.

This kind of consolidation is called Proportionate Consolidation.

You’re bringing over all assets, liabilities, revenues, and expenses at exactly your ownership percentage.

Easy!!! Easy — but this version of consolidation is not the one accounting standards recognize. T_T

(That said, problems sometimes ask you to compare against proportionate consolidation, so it’s accounting theory you need to be aware of!!!)

So which one does the standard actually recognize…

It’s "(Full) Consolidation by Acquisition Method" — and that’s for the next post. Let’s go.

Consolidated financial statements are consolidated financial statements,

and the financial statements for a single company — whether it’s one you control or just have significant influence over — are called “separate financial statements.”

And then there are companies where there’s nothing like control or significant influence going on at all,

and the financial statements for a single such company are called “individual financial statements.” heh

Pop into DART and look up any listed company’s financials — you’ll see two types.

Consolidated and separate.

(Among listed companies, how many actually have zero subsidiaries..? Samsung Electronics had 300+ entities subject to consolidation..)

But hop over to EDGAR and pull up something like Apple..

you won’t find separate financial statements anywhere..

Whether you’re under US-GAAP or IFRS, the principle is consolidation,

but in Korea’s case, under the “External Audit Act” (Act on External Audit of Stock Companies)..

even companies that file consolidated financial statements, on top of the consolidated disclosure,

there’s a law that requires them to also show your pure standalone state separately..

That’s why both showed up in DART. heh

Every company has compliance stuff to deal with,

and the one that usually trips them up is the “Capital Markets Act”..

For instance — KOSDAQ: if operating profit is in the red four years in a row, you get bumped to the watch list,

and one more red year → qualification review → fail to pass = delisting..

(Companies in this zone somehow (?) manage to scrape out a profit once every four years lol

— and these kinds of stocks are called “Olympic stocks,” you know.. because they turn a profit every four years lol)

But hold on — this operating profit that the Capital Markets Act refers to —

is it from the separate financial statements or the consolidated financial statements?!?!?!?!

→ The operating profit here is the operating profit from the separate financial statements..

So among stocks definitely tagged “Olympic stocks,"

when you actually crack open the financial statements,

what is this?! 20 straight years of losses, or zero losses at all?!

— you could very well find that..

If the financials you’re staring at right now are consolidated,

they have nothing whatsoever to do with that law lol

So whenever anyone brings up financial statements,

you have to be clear about which set you’re using as the basis.

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.