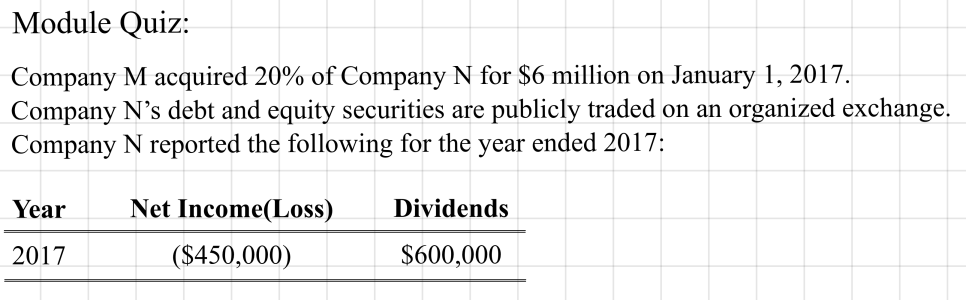

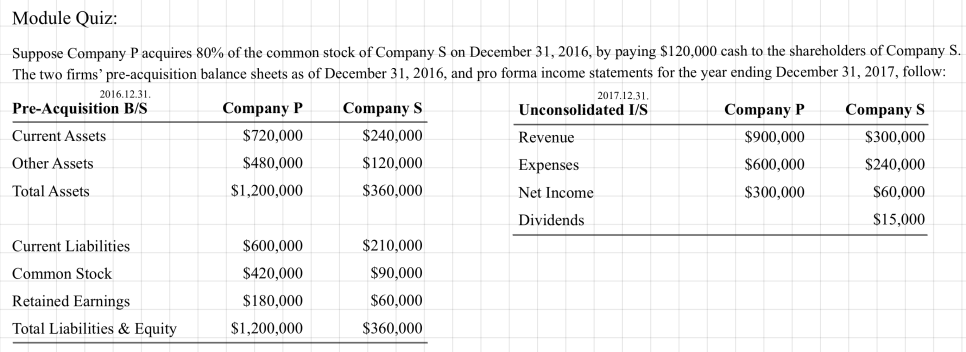

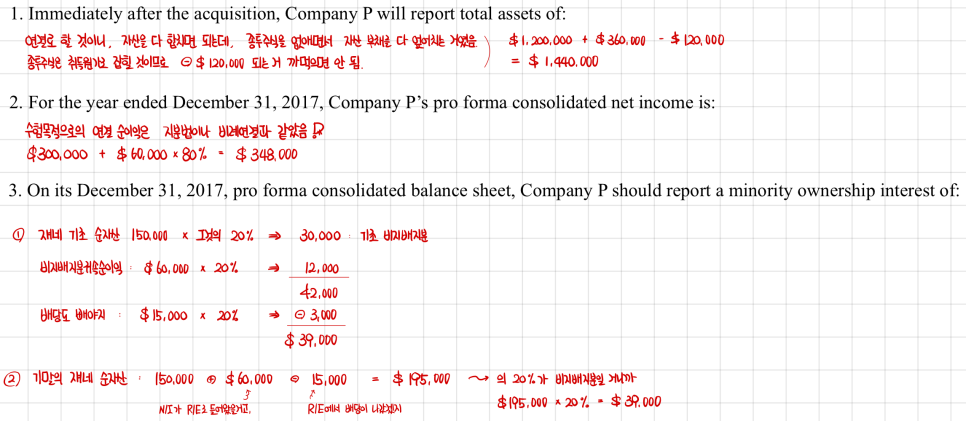

Full Consolidation: The Acquisition Method

A casual breakdown of why full consolidation wins over proportionate consolidation, how NCI keeps the balance sheet balanced, and what it does to your ROE and ROA.

OK so — what does the standard actually mean by “consolidation”?

It’s the thing called "(Full) Consolidation by the Acquisition Method."

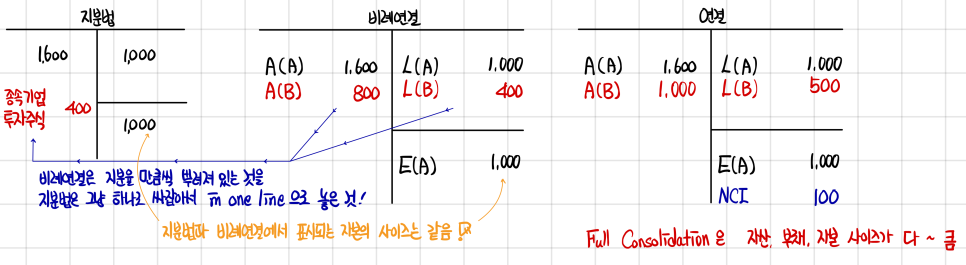

Instead of pulling in assets and liabilities in proportion to your ownership stake, you wipe out the investment-in-subsidiary line and just yank in everything — all of B’s assets, all of B’s liabilities. Just pull it all in!

But… if you grab 100%, the balance sheet obviously won’t balance, right? Bringing in 100% of B’s assets and liabilities means you’ve also brought in 100% of B’s net assets. So how do you make it balance? You pull in 100% first, and then the slice that isn’t actually yours gets shoved into equity as Non-Controlling Interest. Bam — balanced.

Honestly, common-sensically, proportionate consolidation — where you only pull in your own ownership slice — kinda sounds like the more reasonable method, no?

So why on earth — whether US-GAAP or IFRS — did they pick Full Consolidation as the standard…?

Think about it physically for a sec. Wouldn’t proportionate seem more real?

Say the company I control is Hyundai Motor.

If you proportionately-consolidate it,

each car gets sliced at 80% — that part is mine; each machine that builds the cars gets sliced at 80% — that part is mine;

snip snip snip everything gets sliced and “this much is mine!!” — that’s the financial statement you’d get.

But acquisition-method consolidation says: “nah, just use all of theirs for now~~, and then on top of that, list out who has a claim on what.” You’d think that’s the more self-evident view…

OK so up to this point, putting together the methods that describe relationships between companies —

if we line up the three: equity method vs. proportionate consolidation vs. consolidation —

which one comes out with the biggest size?!?! → Consolidation, obviously!!

You’re not slicing and bringing in, you’re bringing it in whole — not only assets and liabilities,

but equity is also biggest under consolidation, because NCI is sitting in there.

Let’s eyeball a comparison.

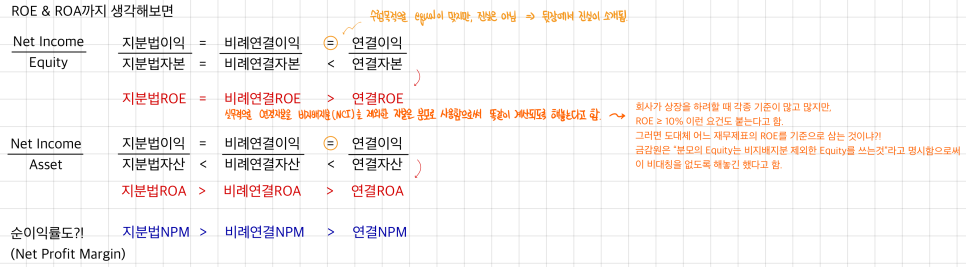

Because of this, certain Financial Ratios get… well…

ROE comes out the same whether you use equity method or proportionate consolidation,

but ROA? Not the same! Proportionate consolidation gives a larger ROA.

And the smallest ROA? Full consolidation, no contest. heh

(they might ask about this kind of comparison)

Quick history detour: before Korea adopted IFRS in 2011, having a subsidiary did not trigger consolidation — you’d just use the equity method.

Then all of a sudden consolidated financial statements became the primary statements, and overnight every company looked like its ROE, ROA, and net profit margin had collapsed. Like collectively, all at once.

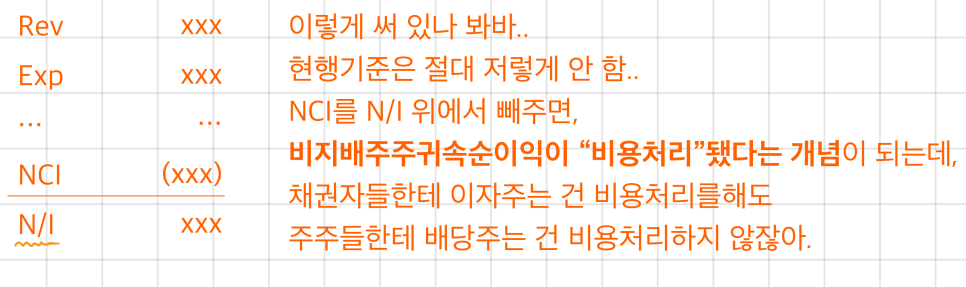

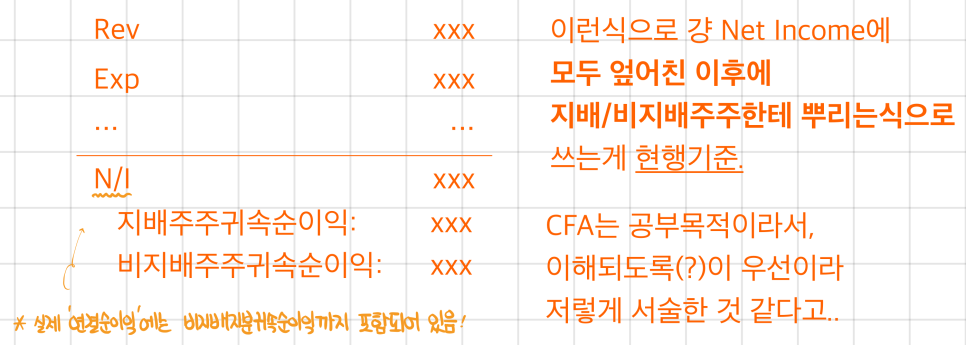

OK now let’s also look at consolidation on the income side.

Same vibe — you bring in 100% of everything first,

and then at the bottom you peel off the slice that isn’t yours,

like so.

Out of B’s profit of 200, you peel off 20% as not-mine. (net income attributable to non-controlling interest)

The not-mine deduction is the same as in the other methods, so the bottom-line number ends up identical. And since the leftover is what belongs to A’s shareholders, we call it “net income attributable to controlling interest.”

Now that we’ve got the rough picture, let’s summarize the I/S impact across the three treatments.

Revenue: equity method < proportionate consolidation < consolidation |Expenses|: equity method < proportionate consolidation < consolidation Income: equity method = proportionate consolidation = consolidation (* income only ever reflects the proportional ownership slice no matter the method, so they have to come out equal~)

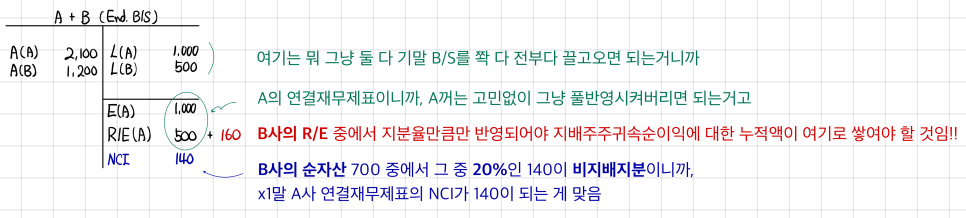

OK let’s run the year-end consolidation all the way through and close it out.

➀ In the consolidated B/S at the start of x1, R/E was zero, and looking at the I/S, the net income attributable to controlling interest is what flows into A’s consolidated R/E. Tracks. So at end of x1, A’s consolidated R/E = 0 + 660 = 660. NCI was 100 at the start, then during the period net income attributable to non-controlling interest of 40 piled on, so ending NCI = 100 + 40.

Approach ➀ is the logic of: “beginning consolidated B/S of x1 + consolidated I/S of x1 ⇒ ending consolidated B/S of x1.”

You also need to be able to derive it using approach ➁: “A’s end-of-x1 separate + B’s end-of-x1 separate ⇒ ending consolidated B/S.”

Now the moment of truth..

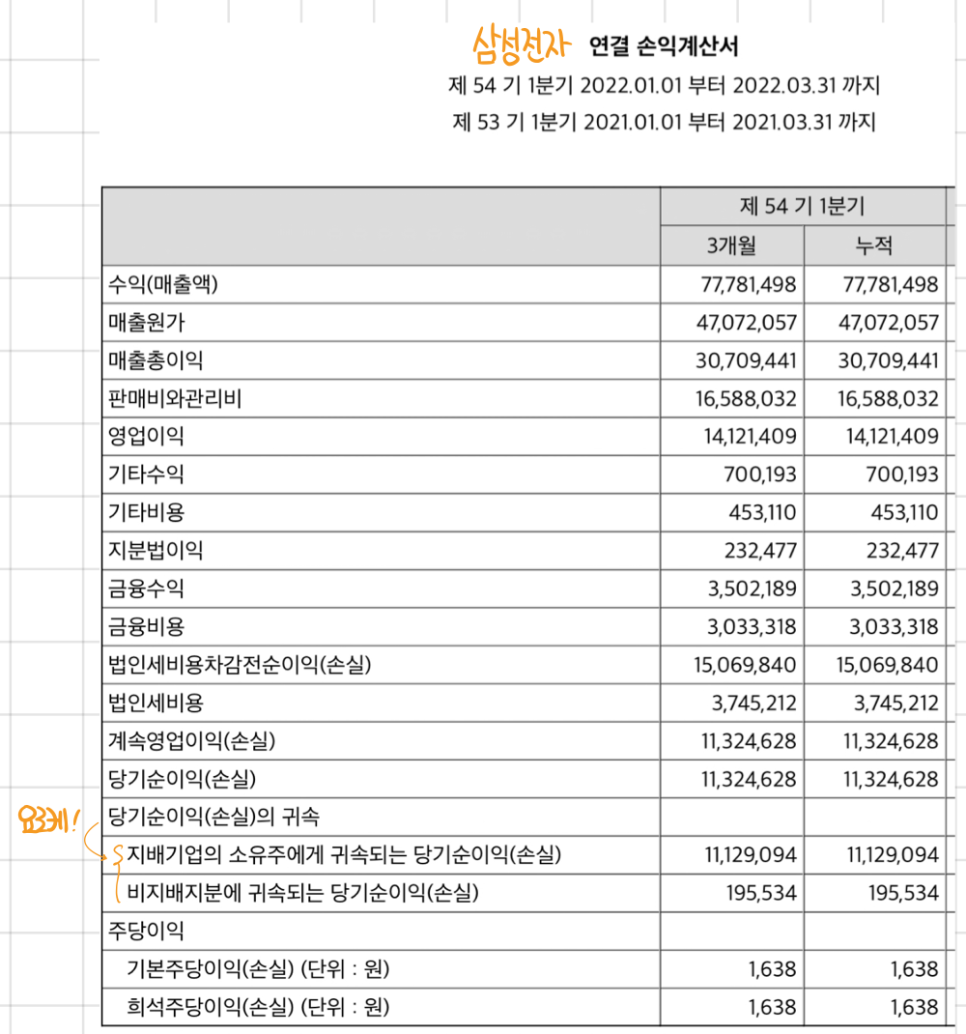

If you actually pop into DART and open up a real set of consolidated financial statements, it looks just like what we worked through above.

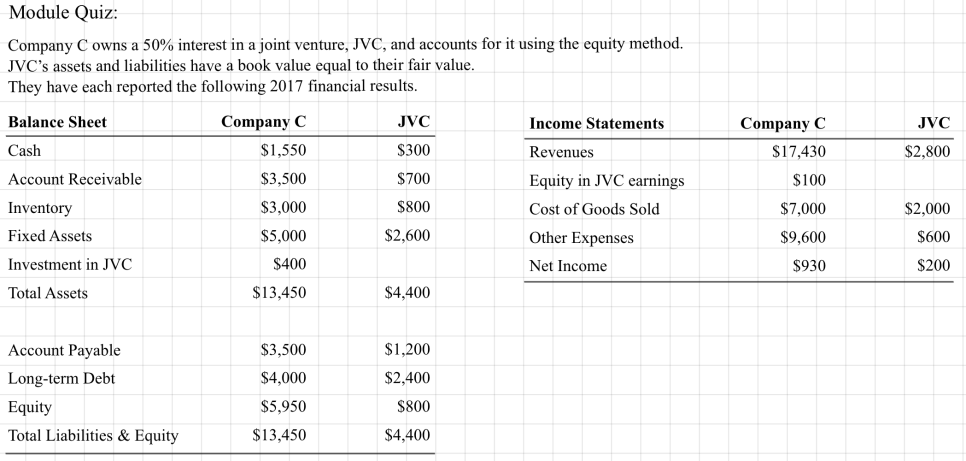

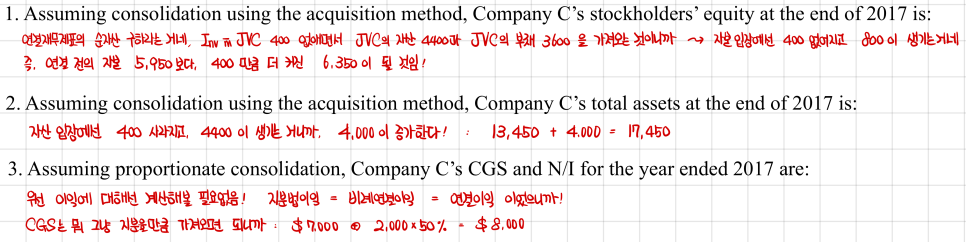

OK story time — the real-brain use case of the equity method vs. proportionate consolidation.. (this one gives me chills..)

Earlier I mentioned Joint Ventures briefly —

“just slap equity method on it..”

— that was about it, and we moved on,

but for setups like this, the actual ownership percentage isn’t really the thing that matters..

because even when the percentages are uneven,

you’ll see lots of deals along the lines of: “when it comes to decision-making, it’s 5:5!”

OK so. Back in the day, Key East — an entertainment company — and JYP set up a JV and shot a drama. At that point, Key East had been running operating losses on its separate financials for 4 straight years. Then this drama became an absolute megahit, right? (None other than “Dream High.”) Oh sweet, saved! …or so you’d think? Nope. Not at all. If you apply equity method accounting, equity-method income gets parked as non-operating income, below the operating line, so they were stuck — staring down a 5th consecutive year of operating losses..

But here’s the thing — at that time, nobody was using proportionate consolidation for JVs, and yet the standard didn’t actually prohibit it..

And if you use proportionate consolidation, you pull in everything proportionately starting from revenue, so you can actually swing the operating line into the black…

Key East’s CEO at the time happened to have an accountant background, flipped his thinking in this exact direction, and — apparently — that’s how they dodged delisting..

A real-deal Brain.. heh wow.

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.