Goodwill (Full and Partial) and Bargain Purchases

Breaking down how goodwill pops out of consolidation accounting, how NCI gets booked, and what happens with partial goodwill and bargain purchases — CFA-style.

Remember that bit I mentioned in gray during the equity method section?

Equity method accounting bundles the goodwill-flavored value inside the equity-method investment line and just lets it ride along — but consolidation breaks goodwill out and accounts for it separately!

That’s exactly what we’re cracking open now.

And remember — out of the 3 things you have to think about in equity method accounting, I said CFA only really asks about 2 of them. In consolidation? You need all 3.

CFA-style consolidated accounting!!!!

➀ BV ≠ FV: the part that gets distorted because net assets are over- or understated ➁ The part you paid on top of FV: Goodwill ➂ Intercompany transactions with the subsidiary (up-stream & down-stream)

Honestly — the odds of #3 showing up on the exam? Basically zero.

In consolidation, the effect is totally different depending on whether it’s upstream or downstream, and it gets ridiculously, ridiculously complicated. No way CFA’s gonna make you do that lol.

Phew. OK, I think we’re set up enough! Let’s dive in.

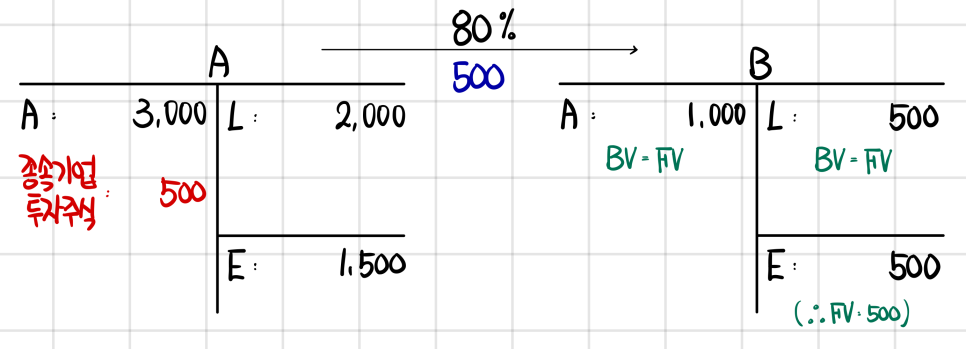

Suppose A negotiates to acquire 80% of B’s shares, and let’s say B’s BV happens to equal its FV.

Then if there were no premium on top, to grab 80% of something worth 500, you’d just pay 400. Easy~

But — they decided to pay 500. Meaning they paid a premium of 100 on top.

(So how were they valuing B’s net assets? Working backward from $625 \times 80\% = 500$, they were treating B’s net asset value — i.e., its market cap, the thing people casually call “valuation” — as 625.)

So A handed over 500 of value, and on its standalone financial statements would have booked an investment of 500.

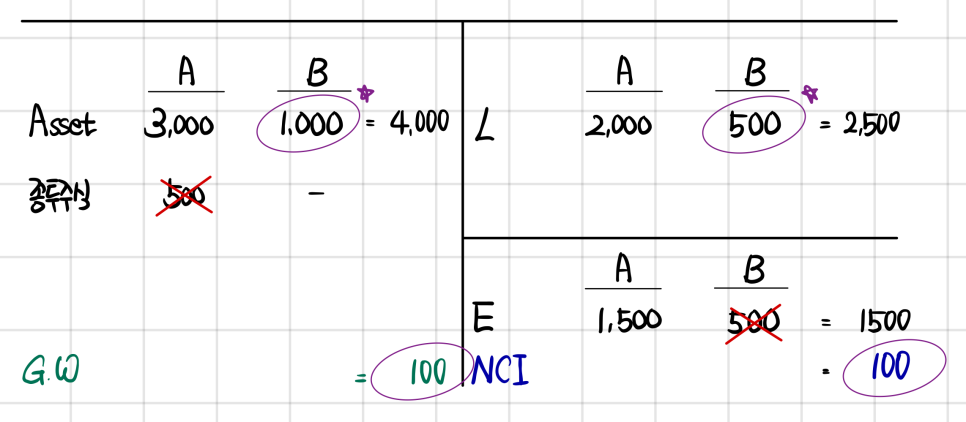

Same as we did with consolidation before — let’s eliminate that investment and flip B’s assets and liabilities onto our books, and watch how Goodwill pops out of the process.

➀ On A’s books, kill the investment line and flip in every asset & liability of B you can see.

(Same idea as “eliminate the investment, eliminate B’s equity, pull in everything else” — we already saw this in the equity method section!)

➁ Out of B’s net assets (500) we just dragged in, the part that isn’t ours has to be tagged as NCI. So we book NCI for the 20% that isn’t ours, which is 100.

➂ At this point, the balance sheet doesn’t balance. Why? Because the investment of 500 we eliminated contained goodwill-flavored value (just like it was hiding in the equity-method investment line!).

The equity-method investment was kept on one line (so was the standalone investment line), but the consolidated statements are the ones that unpack it — and that’s where Goodwill jumps out!!

✵ The circled stuff is what was previously bundled inside the investment line. ✵ If BV ≠ FV, the starred items get written “at FV as of the acquisition date.”

Just for completeness, let’s write the formulas for Goodwill and NCI:

NCI = FV of Net Assets × NCI% ← obvious, taking it for granted heh

GW = Purchase Price − (ownership% × FV of Net Assets) — in words: it’s whatever you paid over and above your ownership share of the net assets!!!

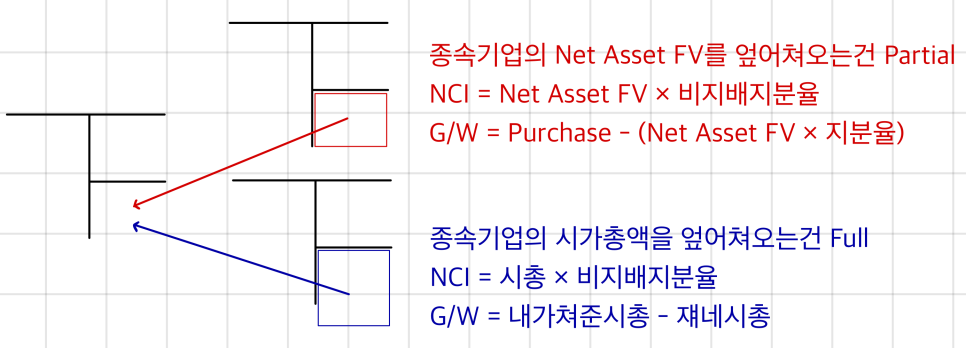

Partial Goodwill vs Full Goodwill

The Goodwill of 100 we just calculated? That’s “Partial Goodwill.”

You also need to know the concept of Full Goodwill.

What’s Full Goodwill? Right now we only pulled in 80%, so there’s some Goodwill that’s invisible — Full Goodwill is the version that puts that on the books too.

Since something with FV = 500 was bought at an implied market cap of 625, the total Goodwill in the deal is 125.

(Every Goodwill we saw from Level 1 onwards was Partial Goodwill.)

Partial Goodwill: IFRS only. Full Goodwill: both IFRS and US-GAAP.

(If the question is US-GAAP, you have to use Full Goodwill, no exceptions. If it’s IFRS, the problem will tell you which method to use.)

✵ The thing you need to remember about Partial vs Full for the exam → Full makes assets and equity bigger. ✵ NCI under Full can get confusing — just use market cap as the base → market cap × NCI%. ✵ In Korea, the vast majority of companies use Partial in practice, because Full is a pain heh.

A friendlier version!

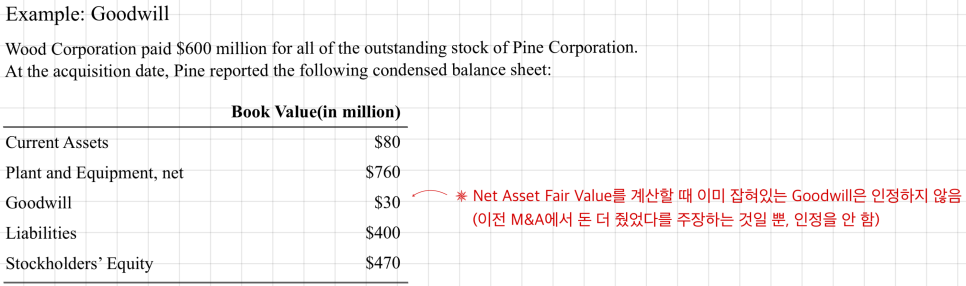

The fair value of the plant and equipment was $120 million more than its recorded book value. The fair values of all other identifiable assets and liabilities were equal to their recorded book values. Calculate the amount of goodwill Wood should report in its consolidated balance sheet.

Wait — the FV of net assets at the acquisition date is already different from BV. What’s going on lol.

Anyway: Goodwill isn’t on the books yet, and we tack on +120 to PPE to bring it to FV → $80 + (760 + 120) - 400 = 560$.

They acquired everything for 600, which is 40 more than 560, so book Goodwill of 40.

Example: Full Goodwill vs. Partial Goodwill Continuing the previous example, suppose that Wood paid $450 million for 75% of the stock of Pine. Calculate the amount of goodwill Wood should report using the full goodwill method and the partial goodwill method.

Net asset FV from above was 560, and 75% of 560 is 420. They paid 450 for that 75% → Partial Goodwill is 30.

If it had been a 100% acquisition, the implied price would be 600. That’s 40 over the implied market cap of 560 → Full Goodwill is 40.

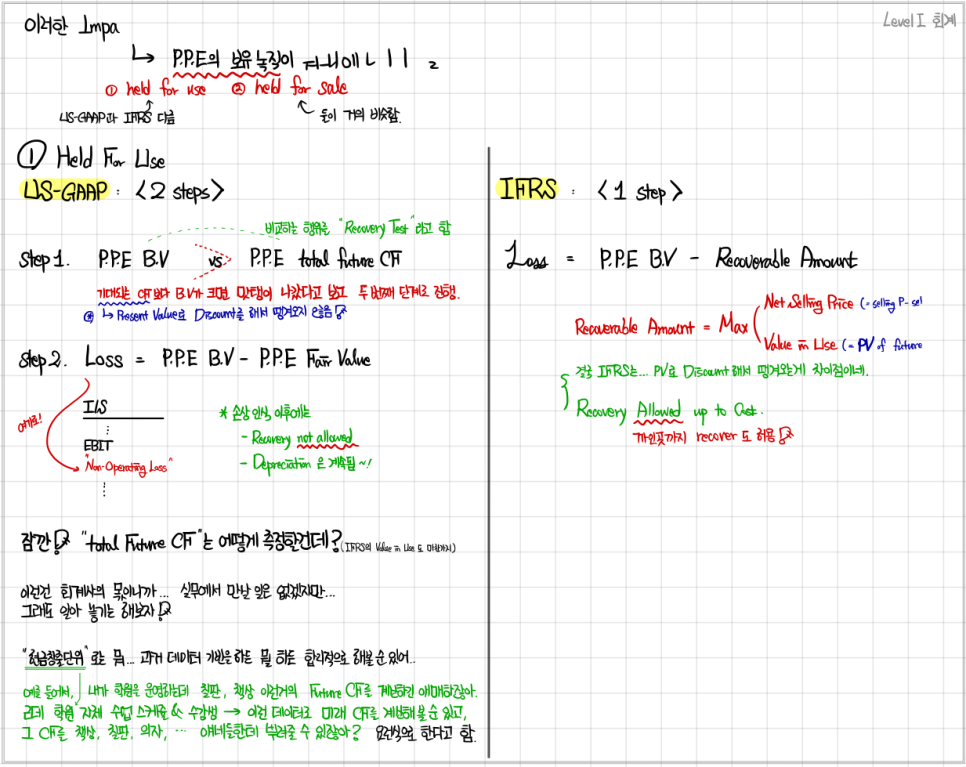

Goodwill Impairment

From what we did at Level 1: Goodwill is classified as an intangible asset with an indefinite useful life, so no amortization.

No amortization, sure — but the moment you sniff that something has gone economically rotten, you slap an impairment on it!!!

The standard here actually splits a bit between US-GAAP and IFRS.

Quick recall from Level 1 on tangible/intangible asset impairment:

US-GAAP: forecast the asset’s BV and the cash flows that asset will throw off. If those cash flows fall short of BV — yep, gone rotten — impair it.

IFRS: compute the so-called Recoverable Amount = Max(Value in Use, Net Selling Price), and impair down to that.

* Value in Use: forecast future cash flows, discount to PV.

Now you might think, “hey, Goodwill is an intangible asset, just do the same impairment dance,” but accounting actually views Goodwill kind of differently from other intangibles.

Tangibles like machines, intangibles like trademarks and patents — the key thing is: you can peel them off and transact in them on their own.

Goodwill? Not so much. The official stance is that forecasting future cash flows attributable to Goodwill alone is basically impossible.

So both US-GAAP and IFRS clearly chewed on this for a while, and the conclusion they landed on was:

“For Goodwill impairment, attach it to the business unit / cash-generating unit that’s actually producing cash flows, do your forecasting there, and check whether that has gone rotten.”

So the very starting point is different from other tangible/intangible assets!

1. Judgment criteria

US-GAAP: attach it to a Reporting Unit (= Operating Segment) and judge there. (An operating segment is basically a business division of the company.)

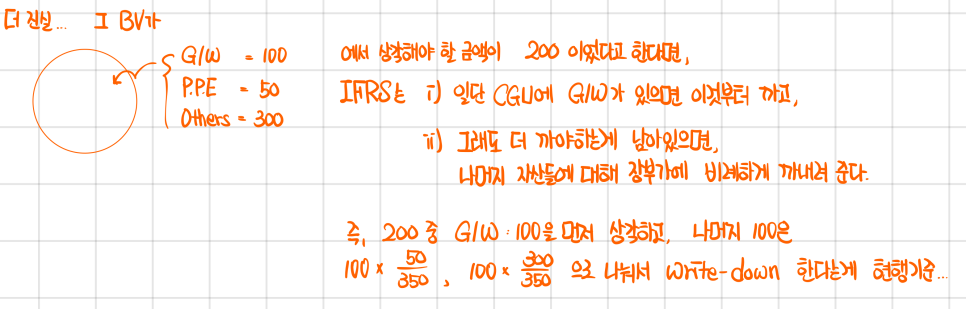

IFRS: attach it to a CGU (Cash Generating Unit) and judge there.

* Where the CGU starts and stops… in practice this gets ridiculously complicated, but since this is for the exam, just hold the words in your head. * Reporting Unit, by definition, is a broader concept than CGU.

The judgment is basically: using those respective units, decide whether to impair or not.

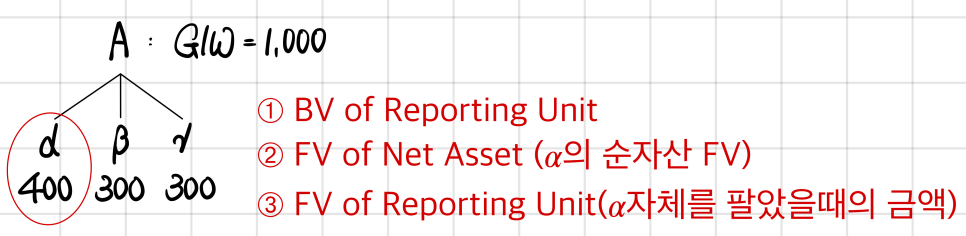

For US-GAAP — say G/W is 1,000, and it’s allocated 400 / 300 / 300 to business divisions 𝛼, 𝛽, 𝛾:

i) If ➀ < ➂: no signs of impairment yet. If ➀ > ➂: signs of impairment detected.

ii) How much do you record as Impairment Loss? Loss = BV of G/W − FV of G/W

That is, you need to realign BV down to the Fair Value of G/W. So ➂ − ➁ is exactly your impairment Loss.

You just run that process division by division. Heh.

For IFRS — the truth is it’s way more complex, but the textbook also just glosses over it in like 3 lines;;

Let’s just roughly remember it like this. A single step is applied:

Recognize the difference between BV of CGU and Recoverable Amount of CGU as Loss. (Recov. Amt. of CGU = Max(Value in Use, Net Selling Price))

If BV of CGU < RA of CGU: the CGU’s assets still carry their weight. If BV of CGU > RA of CGU: knock BV down at least to the level of RA.

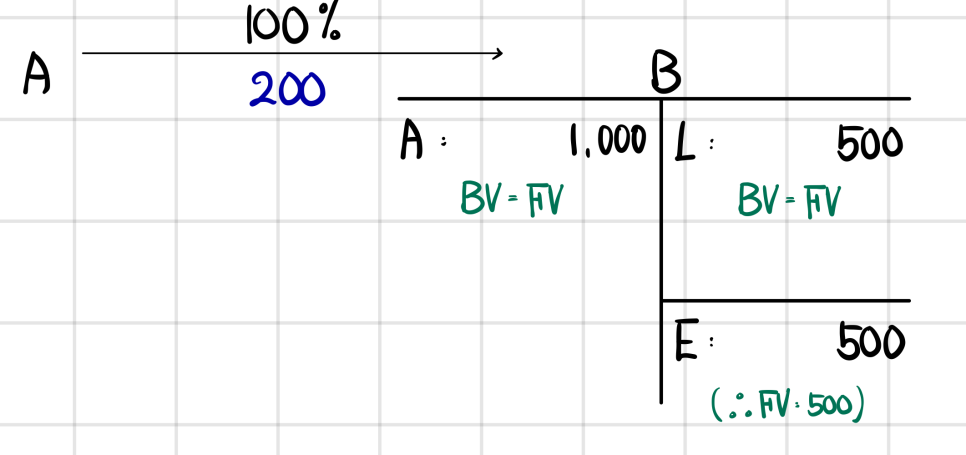

Bargain Purchase

Bargain Purchase is the flip case — instead of paying over the 500 FV of B’s net assets at an implied 625, you pay at a discount.

Say A pays 200 to bring 500 worth of net assets onto A’s balance sheet. Cash drops by 200, 500 of net assets gets flipped onto our books — and obviously the balance sheet won’t balance. Something worth 300 has to materialize on the liabilities or equity side.

This 300 that just got created? It is definitely not a liability. So it has to bump up equity.

In the old days, this was parked directly in equity under an account called “merger surplus” — never touched the income statement.

These days, it does go through P&L (basically: “nice deal, congrats!”). The account is called Bargain Purchase Gain — booked into N/I, which then flows through to R/E.

For exam purposes, that’s all you need!!

In actual M&A — Bargain Purchase deals are basically nonexistent. Almost every real transaction pays above the FV of net assets.

So… were there ever real-world cases of someone buying below?

There was. Hanwha Group acquiring Korea Life Insurance. At the installment-payment stage, a bunch of companies went in jointly: Hanwha, Macquarie out of Australia, ORIX out of Japan…

Of course, Macquarie was only along for the ride to make Hanwha’s acquisition cleaner — Hanwha had a call option on Macquarie’s stake, and Macquarie’s acquisition financing was actually loaned to them by Hanwha. So yeah, plenty of political baggage there, but set all that aside.

If you look purely at Hanwha’s financial statements, here’s what was up. Hanwha was thinking about issuing corporate bonds to raise the funds. The scale was astronomical — a single credit-rating notch could swing hundreds of billions of won in interest expense — so Hanwha was hustling to make their credit rating as pretty as possible.

Their strategy? Trigger a merger between two subsidiaries, generate a Bargain Purchase Gain → push it through N/I into Equity → debt ratio drops → credit rating goes up. Then issue the bonds!!

The problem: IFRS hadn’t been adopted in Korea yet at the time. Under the standard back then, what was called negative goodwill (= minus goodwill) had a rule: “recognize it through P&L over no more than 20 years.”

Most companies were spreading it over 3–5 years. Hanwha? They booked the whole thing at once.

At the time there was uproar — people calling it accounting fraud. But there was also no rule that said “do not recognize it within 1 year”… so from Hanwha’s side they probably felt unfairly singled out.

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.