Special Purpose Entities (SPE) and Variable Interest Entities (VIE)

VIEs always get consolidated — no exceptions — and here's the wild history of how Korea's IMF crisis, ABS, and IFRS killed off-balance-sheet SPC financing for good.

Forget parent vs. sub vs. whatever. Some entities just have to be consolidated, no questions asked.

That’s the VIE — Variable Interest Entity.

This one gets consolidated. Period!!!!

For exam purposes, I think that’s basically all you need haha.

Below… another fun business-history detour hehe.

ABS (Asset Backed Securities) showed up in Korea around the mid-to-late 90s,

right around the IMF crisis,

when banks were piling up non-performing, bad A/Rs…

a credit crunch was kicking in, A/R default probabilities were creeping up,

and KAMCO (the Industrial Assets Corporation, now the Korea Asset Management Corporation) stepped in with public funds and just scooped up all those A/Rs.

Securitize them, and suddenly companies could breathe a little.

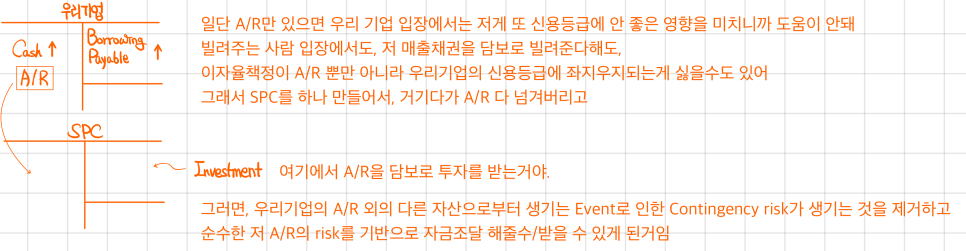

OK so — when a company has A/R sitting on the books

and needs cash now, the easiest move is to borrow against the A/R as collateral.

What that does to the financial statements:

But back then, instead of going to one specific investor,

they’d take money from a bunch of investors on a bunch of different terms,

and that whole package is what we collectively call ABS.

That’s the simple structure of ABS.

And it’s not just A/R — real estate / patents / specific pharmaceutical tech / etc…. all of it can be securitized.

Because what’s really backing it is the Cash Flow off the assets.

In Korea, this whole “spin up an SPC and securitize the asset” technique exploded during the IMF crisis.

Companies were desperate for liquidity..

Who sets up the SPC??? → Our company sets it up!

So the SPC’s Equity belongs to our company.

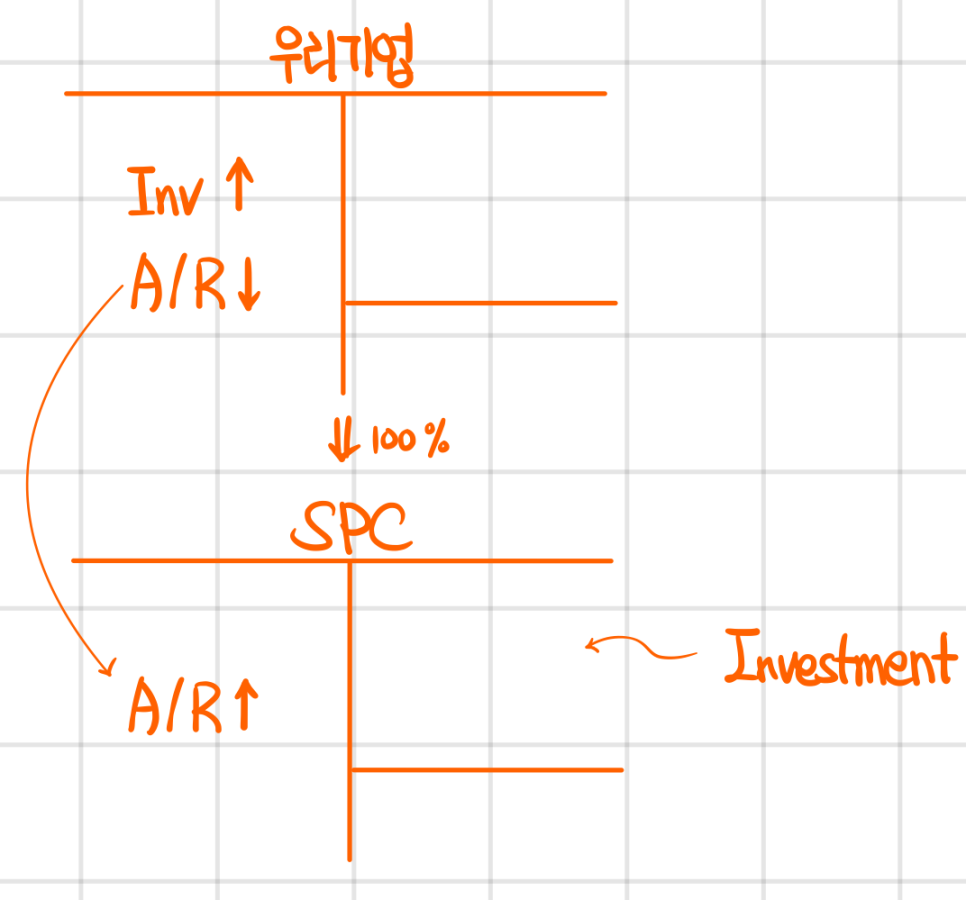

Once the SPC’s up and running, an Investment line shows up on our books.

Boom — Company A just found a way to raise cash off the books (Off B/S Financing),,

But hold on — if we own 100% of the SPC,

we have control → and once you consolidate, it’s not “off” anything anymore,

the equity-method investment just gets flipped back into the SPC’s full balance sheet.

So during the IMF period there were tons of these deals,

but once the concept of consolidation got applied properly,

the whole practical point of this kind of financing pretty much evaporated.

Which is why, under the Asset Securitization Act from the late 90s,

a special law was carved out saying SPC-subsidiaries set up for securitization were excluded from consolidation.

Just to keep securitization actually useful in practice.

Then around 2010, IFRS rolls in,

and with it — Korea’s special laws and all that? Gone!

So as of now, it’s completely impossible for a company to spin up an SPC like this and do Off B/S Financing.

Everything gets flipped and consolidated. No exceptions.

So what scheme do people use instead..

They go: “well it’s not a company we control, right?” — they bring in a 3rd party who puts up only nominal share capital (Thin Capital) into the SPC’s Equity. And the place where this got pushed to an absolutely insane extreme and ended in disaster was the Enron incident.. (and that’s not even all of it haha — the cash raised this way also got booked as CFO, which we’ll get to in Chapter 5) [Book I studied: Managing with Numbers, Vol. 2 (5): The Fall of Enron] After that whole catastrophe blew up, the rule that came out of it was: “Even if there’s no visible direct parent-sub relationship, if an SPC meets certain conditions, you consolidate it!!!” And whatever the “Vehicle” happens to be at that point — an SPC that meets the criteria, a Joint Venture, whatever — that’s what we call a Variable Interest Entity (VIE).

These SPCs aren’t out there running their own separate business or anything,

they exist purely for the benefit of “our company.”

Meaning they move in lockstep, one-to-one, with our company’s interests,

they have no independent interests of their own.. and that’s the sense in which it’s called a VIE.

I was about to just wrap up here, but the story landed so cleanly in my head I feel like I should crack open the book, see how the textbook actually says it, and then finish… heh.

A special purpose entity is a legal structure created to isolate certain assets and liabilities of the sponsor

→ legal structure: can be anything — corporation, partnership, joint venture, trust

And like I said above, third parties do hold the control.

→ sponsor: the company playing the “our company” role here is called the sponsor.

OK so — what are the certain conditions an entity has to satisfy to count as a VIE?

FASB: a VIE is an entity that has one or both of the following characteristics:

- At-risk equity that is insufficient to finance the entity’s activities without additional financial support.

“The equity investors taking on the risk aren’t enough” is basically just a fancy way of describing a Thin Capital structure.

- Equity investors that lack any one of the following:

i) Decision making rights

ii) The obligation to absorb expected losses

iii) The right to receive expected residual returns

So the equity investors have no decision-making power, no residual claim, they’re nothing more than nominal equity holders..

If an SPE is considered a VIE, it must be consolidated by the primary beneficiary.

Among Korean companies operating in China, there are actually quite a few that consolidate entities they own 0% of.

Because China’s a socialist country,

there are plenty of industries where foreign companies straight up aren’t allowed to be shareholders,

so you have to slot a local Chinese person in as the equity holder.

But every single decision is being made from Korea,

so even without any direct controlling-ownership relationship, all of those entities have to get consolidated!

IASB doesn’t use the term VIE,

but it specifies consolidation using the wording “if there is (not formal but) substantive control~”.

Bottom line: SPEs that meet the VIE requirements end up subject to consolidation under IFRS too.

And with that — equity method & consolidation, completely wrapped~

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.