Defined Benefit Pension Plans: Accounting Treatment

A breakdown of how severance pay and DB/DC pension plans hit the financial statements — and why stashing money outside the company matters when things go south.

Chapter 2.

Employee Compensation: Post-Employment and Share-Based.

Two ways companies pay people after they leave: severance pay or a retirement pension. And we’re also kicking off the stock options theme!!

OK so let’s think about how this should hit the financial statements. It would be wrong to dump the whole severance payment onto the books at the moment it goes out the door. Why? Because one of the core accounting principles is that revenues and expenses have to match. If an employee gave you 10 years of service and 10 years of revenue, the severance you eventually pay them needs to be smeared across those 10 years too.

So every year — assuming the employee could leave in year XX — you book a chunk of expected severance as an expense on the I/S, and that expense piles up as a liability on the B/S. Then when the employee actually really resigns, Cash↓ / Obligation↓ cancel out, and look at that — the cost matching that Cash $100M↓ has been getting expensed bit by bit consistently over the years, so now the Matching Principle is happy! This whole setup is called the severance pay system.

Apparently the concept doesn’t even exist in the US.

And even big Korean companies mostly don’t do it anymore.

Why? Because the severance pay system has a problem…

You’re diligently expensing things step by step like a good citizen, and then the company suddenly goes bankrupt???

Now other creditors come stampeding in going “give us our money~~”, and in that case, couldn’t you end up just… not getting your severance…

(Korean labor law gives the top priority to 3 years’ worth of severance and 3 months’ worth of salary, and labor law leans pretty employee-friendly.

But still — an employee with 10 years of tenure… the other 7 years.. (bye bye)..)

To fix this, what came along was the retirement pension system.

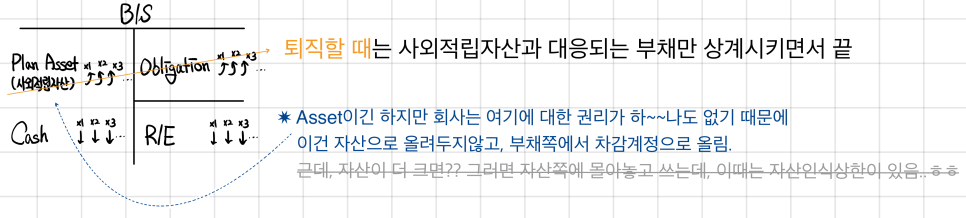

If you stash the money outside the company like this, then even if the company goes bust, those funds are still sitting there safely. For this to actually mean anything, the company can absolutely never withdraw money from there, and you can’t even touch it as collateral no matter how hard you try. Just think of it as no longer being the company’s money — it’s the individual employee’s. Of course, creditors can’t go after it either. That’s why severance pay = the internal reserve system, and pension = the external reserve system.

Under this kind of system, let’s take a quick look at how the financial statements get hit.

This pension system splits into two flavors:

DB (Defined Benefit) / DC (Defined Contribution)

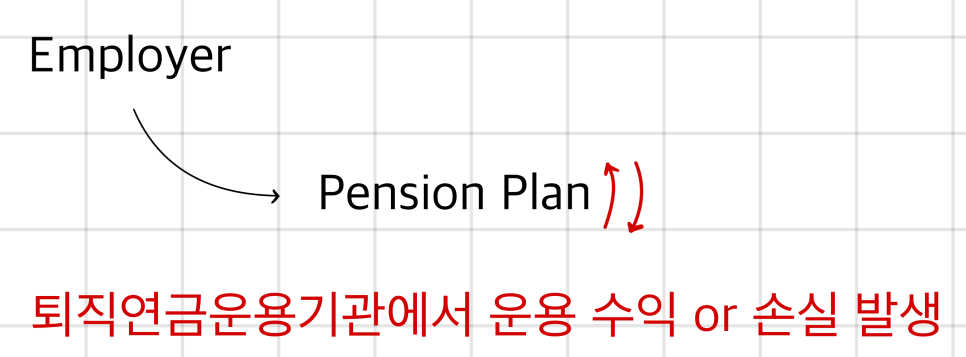

DB Type: Doesn’t matter what kind of operating gain or loss the managing institution coughs up — none of it matters,

because the Benefit going to the employee is fixed (defined).

In other words, the employer eats the operational risk.

DC Type: The operational risk is on the employee.

From the company’s side, you just steadily shovel money into the Pension Plan and that’s it.

(Since it ends with “just shovel money in,” there are no juicy issues here.. So no exam problems get made out of this either.)

It’s the DB type that’s the troublemaker.. Because it’s the concept that the company manages the gains and losses,

if there’s a gain, you contribute a little less to Plan Asset / if there’s a loss, contribute a little more.. that kind of vibe.

Also, it’s not like 100% of all employees will all eventually resign,

so you just estimate roughly how many you expect to leave and size the liability against that

(Like a bank holding reserves against deposits at the reserve ratio.

Of course, the law does say that even for DB type, you have to fund 90–95% or more.)

Anyway, the first issue is

the question of how much to set aside as that liability!!

Because the standard says: that liability = “the present value of the amounts that’ll go out as severance in the future”..

The probability each employee leaves, how much severance they’ll actually get when they leave, whether they take it as a lump sum or as an annuity,

if as an annuity, you also need to fold in mortality rates..

This part is seriously hairy from an accounting standpoint..

✷ Discount rate, average service life, mortality rate, compensation growth rate, and on and on

So many assumptions go into the calculation.. So this number doesn’t get computed by the company itself — usually,

an actuarial firm gets all the company’s data and crunches it.

(In other words, the assumptions here are Actuarial Assumptions.)

On top of that, the state of the company keeps changing, and as it does, this liability number keeps wobbling and slamming into the financial statements…

And the intro isn’t even DONE yet!!!! lol

OK from here we’ll start studying each account one by one,

but one thing’s for sure — this is not a chapter you read once and “get” in one shot, so slooowly….

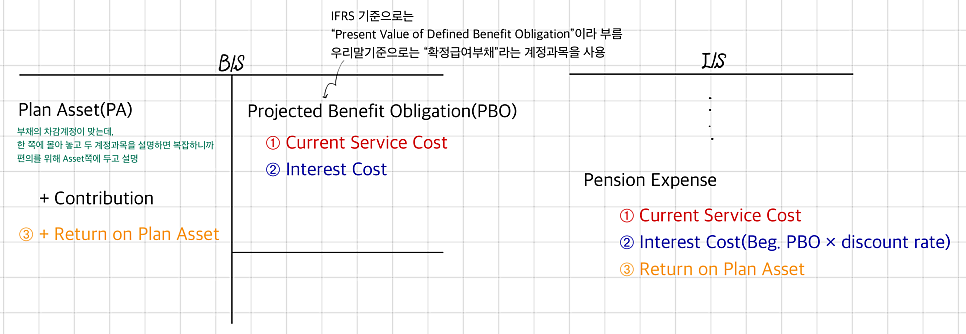

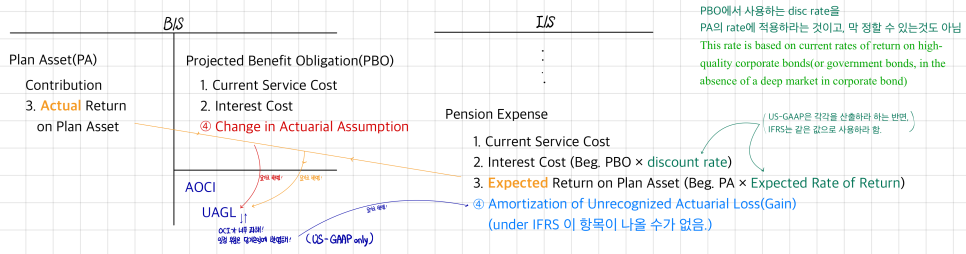

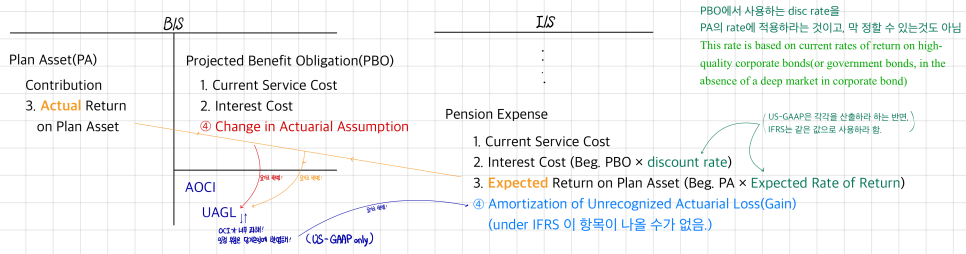

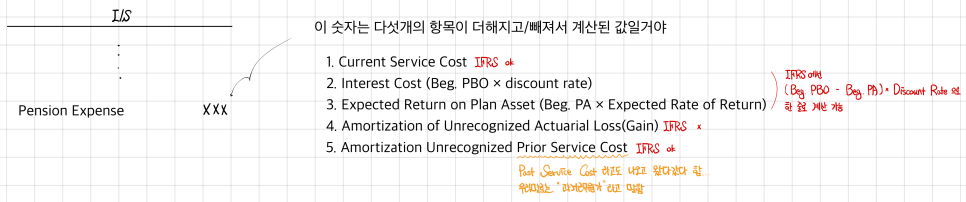

Right then, we’re gonna intensively study 5 account items. Let me lay out 1 through 3 first and we’ll look,

First — PA (Plan Asset) and Contribution wrap up easy so I didn’t slap numbers on them.

This part is just contributions + interest & gains earned,

think of it like a bank account balance, nothing scary.

Now let’s tackle the numbered ones one at a time,

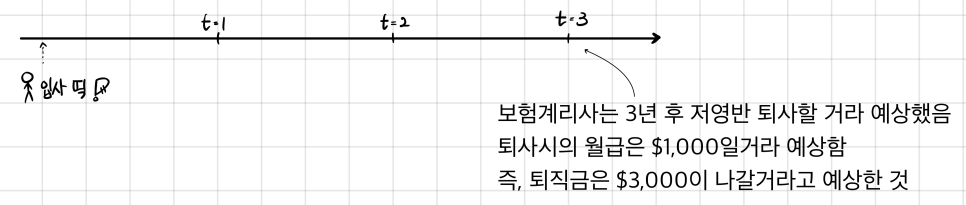

The point in time when the company’s obligation to pay severance kicks in is 1 year later.

So at this point, the company owes 1/3 of $3,000, which is $1,000,

and the present value of that is what becomes the liability. $1,000/(1.1) = $826

If the discount rate is 10%, it’s $826,

and this number is called “Current Service Cost” (you have to know all these terms!!!)

This gets reflected in the B/S and I/S at position ➀.

And since 826 is now discounted at 10%,

that means it’ll grow by 10% next year.

The following year, 826×1.1 = 908 it has to become,

and the difference of 82 is treated as “Interest Expense.”

(Not booked as interest expense inside operating expenses — both IFRS and US-GAAP explicitly say to include it inside Pension Expense.)

That employee has now logged another year of service, so we’re at 2 years.

So the obligation becomes 2/3 of $3,000, and the PV is $2,000/1.1 = 1,818,

and the 826 we loaded last year

has grown to 908 by now, so the remaining 910 gets booked as the second year’s Current Service Cost.

In year 3, the full $3,000 has to be captured.

End-of-prior-year PBO is sitting at 1,818, which grows by 10% to $2,000,

and the leftover $1,000 gets booked as Current Service Cost — done.

And if everything plays out exactly as expected and they ride it all the way to resignation,

you just blow away the $3,000 piled up as PBO together with what’s sitting on the Asset side!

But wait — on the Asset side, do you only reflect what got contributed via Cash↓…

No no no, because it’s DB type,

operating gains or losses also feed into that asset,

so wouldn’t it be fine to just reflect that in Actual Return on Plan Asset..

And this operating income would also hit the I/S, so it ends up reflected in R/E…

IFRS, US-GAAP both say don’t recognize that operating gain or loss separately on the I/S —

they specify to net it inside what gets booked as pension expense..

OK we’ve now seen up through item 3 (well, no, we’ll talk about item 3 a little more) —

what needs to pile up as Pension Expense on the I/S goes all the way out to item 5!!! (For IFRS, item 4 of the 4 and 5 gets dropped, heh.)

Two more to go!!!!!!!

Ahh!! It’s quite a lot complicated!!!! lol

Once you get it later it won’t feel this complicated,

but the first time you bump into it, yeah, it does feel pretty complicated (T_T)!!

Take a rough look at the picture first, then bounce back and forth between the explanation and the picture below..

When a company is on a DB type retirement pension system,

we’re looking at how — and through which account items — the B/S and I/S get hit,

and we’ve seen how PA, PBO, and P/Exp interlock and turn together,

and now we’re picking up item 3 again..

The operating gains on the B/S’s PA do increment/decrement correctly against Actual G/L on PA,

but on the I/S side, instead of Actual, they use Expected..;;;

Like — the employees working at the company aren’t really doing anything different,

it’s just the market that’s bouncing up and down, and yet because of that the company’s labor-cost line gets volatile, and accountants hate that.

So as a “Expected” concept, they do a little bit of Smoothing,

the Asset side reflects Actual, and the I/S side eventually rolls into R/E,

but if you use Expected Rate over here, debit and credit obviously aren’t gonna balance.

The mismatch gets specified to be reflected in AOCI.

The account name used is “Unrecognized Actuarial Gain or Loss (UAGL).”

You can think of UAGL as the trash bin where the garbage from smoothing Pension Expense piles up.

Cases caused by PA:

i) Actual > Expected → Unrecognized Actuarial Gain arises

ii) Actual < Expected → Unrecognized Actuarial Loss arises

There are also cases where UAGL arises because of PBO. (Meaning UAGL has two sources.)

When you calculate PBO, a ton of Estimates get assessed and used,

like, last year you used a wage growth rate of 3%,

but this year, looking at it again… 2% feels more appropriate… that kind of thing.

So you might think, hmm, last year’s number over- or underestimated PBO~

This assumption keeps changing every year,

and every time it does, the liability could swell or shrink,

and if you smash that swing onto the I/S, the labor-cost line is no longer smooth..

So this also gets piled into UAGL as trash.

ex.

Wage growth rate 3% → 2%: PBO needs to be marked down a bit → reflected in UAG of AOCI in equity by the amount the liability shrank

Wage growth rate 2% → 3%: PBO needs to be marked up a bit → reflected in UAL of AOCI in equity by the amount the liability grew

And UAGL from PA & UAGL from PBO are netted together and shown as one line.

Now look at the picture again

How do we deal with all this trash piling up in UAGL going forward..?

IFRS ⇒ No Action:

Actuarial assumptions can be off in the short run,

but in the long run they’ll naturally converge and cancel out,

so when they show up, let them pile up; when they vanish, let them vanish (= just leave it alone).

Eventually that pile becomes 0.

US-GAAP ⇒ In principle No Action, but it sets a Corridor (a range),

and says the part exceeding the corridor must be reflected in current period P&L.

The part exceeding Max(Beg. PA, Beg. PBO) × 10% gets pushed into P&L.

This is called Amortization, by the Corridor Method. (Amortization by Corridor Method.)

But it doesn’t say to amortize that excess part all in one shot —

you spread it over the average service life and reflect that in current period P&L.. (wow, this is really crossing a line lol.)

Summary summary!!

UAGL of AOCI arises under both IFRS and US-GAAP,

but the handling differs,

and because of that difference, item ➃ on the I/S is absent in IFRS / present in US-GAAP,

and that’s where the gap comes from!!

And one more term!!

The stuff reflected in UAGL (the 2 kinds) is collectively called “Remeasurement Cost”~!

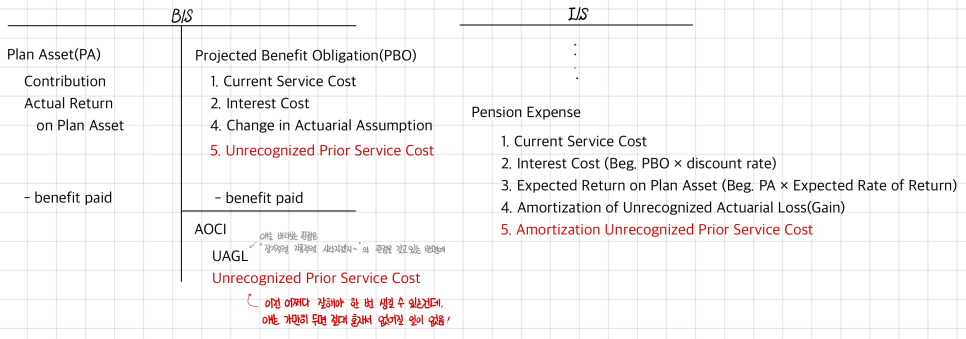

Last item ➄! This one shows up under both IFRS & US-GAAP!

Item 4 was about a change in Assumptions used to make some Estimate (Expected Rate, or actuarial assumptions… that kind of thing),

a change in assumptions,

item ➄ is about “cases where our company’s pension-related Policy changes.”

Easy example — say the retirement benefit policy was salary × years of service, and then

they suddenly lose their minds and announce they’re switching to salary × months of service!!!

Well, if you slam that onto the I/S and B/S all at once as labor cost,

that obscures the whole Smoothing goal again,

so for this one too, they say don’t reflect it in current period P&L —

reflect it in the AOCI trash bin.

But! Not the same trash bin from before —

they say make a separate trash bin and pile it in there… (seriously, stop crossing the line…)

So under both US-GAAP & IFRS, they say not to leave this item alone — push it into current period P&L,

IFRS: instead of piling that occasional item in AOCI,

they just push it into current period P&L in one shot.

Book the liability, bam!, and shove it up to the I/S.

(So under IFRS, there’d be no account called UPSC in AOCI.)

US-GAAP: Amortization over average service life — so it bleeds into current period P&L little by little.

Phew.. all 5 done..

You have to memorize all 5 of these items and know how to compute each one accurately..

That’s it for DB type.. (T_T) That was a long road..

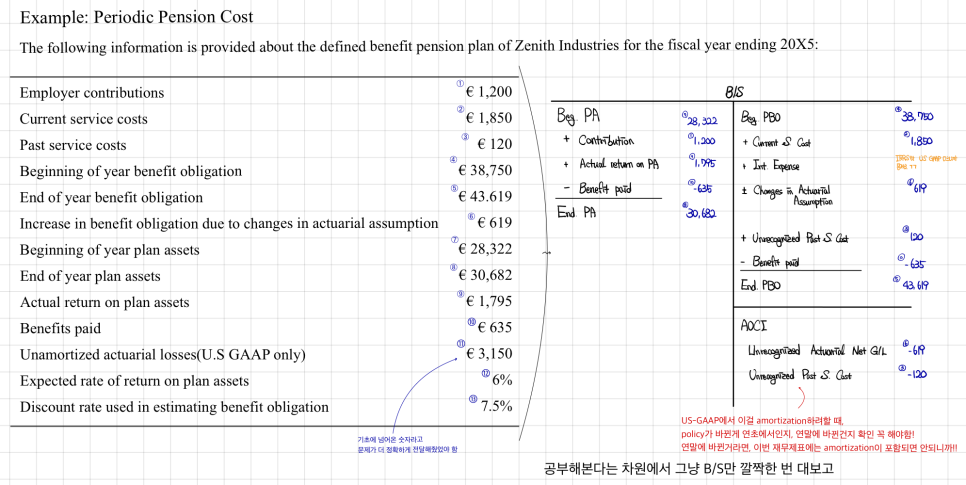

Calculate:

1. Beginning & Ending Funded Status:

Beg. PA - Beg. PBO = 28,322 - 38,750 = (10,428)

End. PA - End. PBO = 30,682 - 43,619 = (12,937)

3. Periodic Pension Cost reported in P&L under US-GAAP (ignore amortization of past service cost)

You have to fill in all 5 items on the I/S in order. 1. Current Service Cost is given as 1,850.

- Interest Cost is Beg. PBO × discount rate,

and Beg. PBO is the opening PBO viewed from the end-of-period vantage point,

but in this problem the policy change is pinned at the beginning,

so the beginning PBO viewed from the end is 38,750 + 120.

That × 7.5% gives Interest Cost = 2,915.

- Expected Return on PA is different under IFRS and US-GAAP,

US-GAAP: 28,322 × 6% = 1,699

IFRS: 28,322 × 7.5% = 2,124

- Amortization of Unrecognized Actuarial Loss:

under US-GAAP — 619 arose, and Max(Beg. PA, Beg. PBO) × 10% = 3,875 → it’s inside the Corridor range so there’s nothing to amortize.

Under IFRS, this account item doesn’t even exist.

- Amortization of Unrecognized Past Service Cost:

Under US-GAAP, it’d need to be divided by average service life, but that wasn’t given and we were told to ignore it heh.

IFRS reflects it in one shot.

Pension Expense (US-GAAP) = 1,850 + 2,915 - 1,699 = 3,066

4. Periodic Pension Cost reported in P&L under IFRS

There’s no instruction to ignore past service cost here..

Pension Expense (IFRS) = 1,850 + 2,915 - 2,125 + 120 = 2,761

You just tack on the Past Service Cost 120 (reflected all at once) and that’s it.

5. Periodic Pension Cost reported in OCI under US-GAAP

6. Periodic Pension Cost reported in OCI under IFRS

First trash bin, Unrecognized Actuarial G/L:

Due to change in assumptions → (619) (same under IFRS)

Due to the gap between Actual and Expected → 1,795 - 1,699 = 96 (Under IFRS: 1,796 - 2,124 = (329))

Second trash bin, Unrecognized Past Service Cost:

US-GAAP (120)

IFRS: nothing going through OCI

Capturing only the newly-arising trash as OCI,

US-GAAP: -619 + 96 - 120 = (643)

IFRS: -619 - 329 = (948)

There are more problems in the Textbook,

hmm.. the Textbook problems seem a bit easier so — pass~!

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.