Defined Benefit Pension Plans: Analytical Perspective

Even though it got yanked from the 2024 CFA L2 curriculum, here's how analysts reclassify pension F/S and compute TPPC — both ways — from an economic lens.

Heads up — this content actually got cut from the 2024 CFA Level 2 curriculum, did you know that??

But knowing those CFA folks, they could yank this section right back in at any moment. So I’m just gonna write it down anyway, for safety.

For Analytical Purpose (1): Reclassify & Restate F/S

From here on, instead of coming at this from the accounting-standards angle, let’s flip and look at it from an analytical angle. (There are 2 things on the analyst’s to-do list — we’ll hit both.)

If you’re the one doing the analysis, you need to think about some adjustments. Why??

Because the accounting standard right now is obsessed with one thing: smoothing out personnel costs. Without the smoothing, anything that got wrecked because the actual market did what it did would all hit P&L. Reflect all of that — and on top of that, take everything stuffed into that garbage bin called AOCI and shove that through P&L too —

and what does the financial statement even look like at that point?!

One more thing.

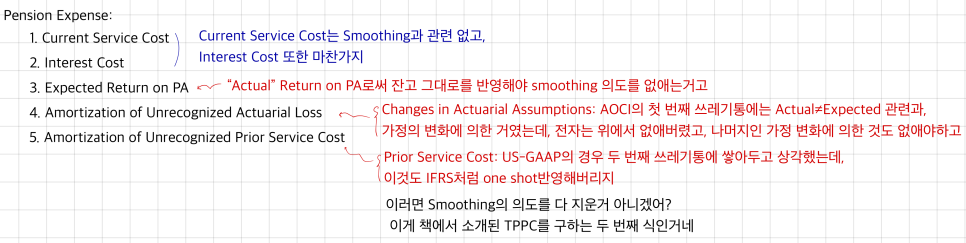

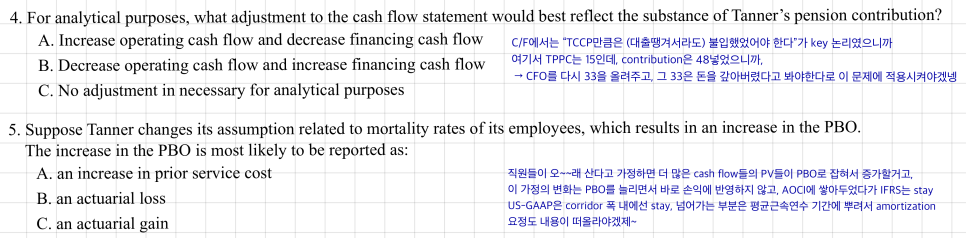

Pension Expense is a personnel-cost item, right? So personnel costs for factory workers go into CGS (cost of goods sold), and personnel costs for office workers go into SG&A.

But hold on — out of the five items that make up Pension Expense, items 2 and 3 are interest costs. And interest cost on the I/S? That lives in non-operating income/loss, below operating income, alongside interest income and interest expense.

→ So the move is: take items 2 and 3 and stick them down in non-operating interest expense, where they actually belong by nature.

That’s the concept. And with that concept in mind, we need to Restate the B/S, the I/S, and the C/F.

OK so — does PA, recognized from the accounting side, need to be corrected for the analyst who’s looking at this through an economic lens? Nah. PA is recognized basically like a real bank account balance, so there’s nothing to fix. What about PBO? From the accounting side, PBO is forecasting future retirement payouts and pulling them back to present value. Doesn’t seem like we need to mess with that either. So — the items already sitting on the B/S are economic-perspective figures as is. The B/S does not need adjusting. That’s why the textbook also says Funded Status = Economic Status.

The Pension Expense on the I/S, though — that one has Smoothing baked in. So the move there is to convert it to TPPC (Total Periodic Pension Cost) — i.e., ask “what would this number have been if nobody had smoothed it?”

There are two ways to compute TPPC. (You need to know both.)

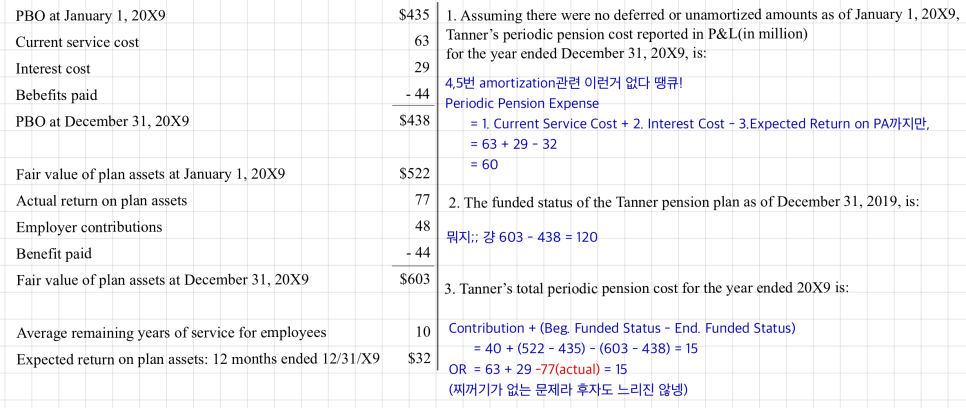

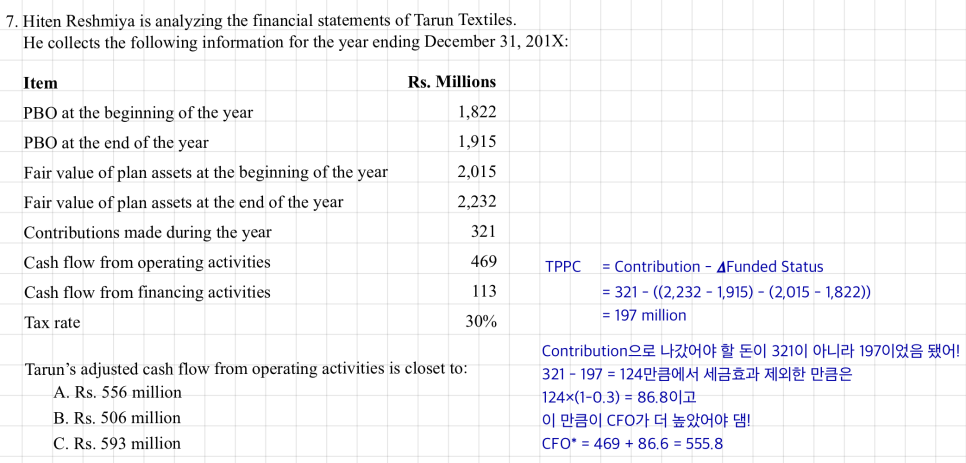

$$\text{i) TPPC} = \text{Employer Contribution} - (\text{End. Funded Status} - \text{Beg. Funded Status}) = \text{Contribution} - \Delta\text{Funded Status}$$$$\text{ii) TPPC} = \text{Current Service Cost}$$$$+ \text{Interest Cost}$$$$- \text{Actual Return on PA}$$$$- \text{Actuarial Losses/Gains due to Changes in Assumption affecting PBO}$$$$+ \text{Prior Service Cost}$$Rather than just following what the book does, let’s approach this conceptually for a sec. Our Pension Expense formula is:

So how do we get the first TPPC formula?

Look at how PA & PBO were rolled forward:

Beg PA − Beg PBO + Contribution + $\alpha$ = End PA − End PBO

Beg Funded Status + Contribution + $\alpha$ = End Funded Status

Beg Funded Status − End Funded Status + Contribution = $-\alpha$

And boom — that’s where the first formula comes from. Heh.

Would be great if every problem could be cracked with that nice clean formula. But problems aren’t always designed to be solvable with formula (i) alone, so — you gotta know both.

OK OK OK OK, to summarize:

One of the things on our to-do list for analytical purposes is Reclassify & Restate:

- Step 1. Compute TPPC. That’s number one.

- Step 2. Take Interest Cost and Actual Return — both inside TPPC — and push them down below operating income, right alongside the other interest expense & income, so they get classified as non-operating and don’t contaminate operating income.

Two steps. That’s it!

For Analytical Purpose (2): Plan Assumptions

Out of PA, PBO, and Pension Expense — PA has no assumptions going into it. The other two do.

And these assumptions aren’t the accounting standard’s — they’re assumptions made by whatever actuary the company is using.

Now — if the company is big and has a not-small number of employees, well, even just one assumption — say the wage growth rate gets set even 0.01% differently — the impact on the personnel-cost line item is going to be far from trivial.

Which is to say: the analyst needs to have done sensitivity analysis — what would the financial statements have looked like if the assumptions had been a bit different? (And conveniently, the assumptions are required to be disclosed in the notes, no exceptions.)

✷ The effect of an assumption change on PA is always No Effect!

If the wage growth rate goes down, future retirement benefits going out get projected smaller. So the corresponding liability shrinks, and cost recognition shrinks. Current Service Cost drops → so TPPC drops too.

Expected Rate is not reflected in PBO!!!

Pension Expense gets affected, but since the resulting gain/loss ends up in AOCI on the B/S, neither PA nor PBO move. And since TPPC uses Actual Rate of Return, TPPC also has No Effect!!

(IFRS doesn’t use Expected rate of return at all, by the way… like, IFRS straight-up says no.)

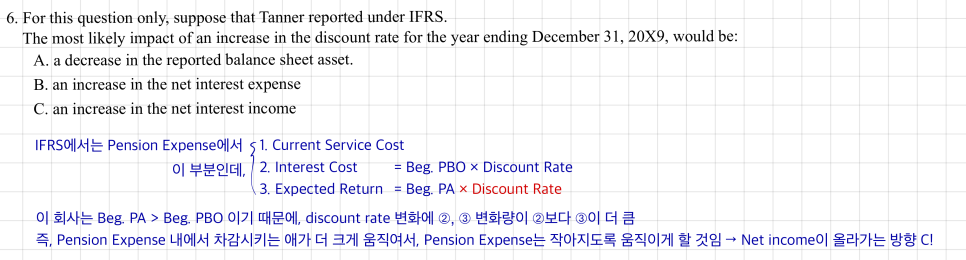

For PV of PBO — if you use a big discount rate, the PV comes out smaller. So PBO shrinks. Then Current Service Cost shrinks. So Pension Expense on the I/S shrinks, and TPPC shrinks too —

But wait. The concept was that Interest Cost accrues at the discount rate. So interest cost goes up, right??

Hmm. So a change in Discount Rate can push TPPC and Pension Expense either up or down.

Here’s the tiebreaker, though:

- For a company where PBO is huge, a discount-rate change has a bigger effect on Interest Cost than on Current Service Cost (effect on CSC < effect on Interest Cost).

- For a company where PBO is small, the discount-rate change hits Current Service Cost harder than Interest Cost (effect on CSC > effect on Interest Cost).

So on the exam, the premise will pretty much always be set up like:

“The firm has a relatively young workforce with a low percentage of retirees”

That’s the signal that it’s a young company — meaning PBO isn’t huge yet because not enough years of service have piled up. (Which means the Current Service Cost effect dominates.)

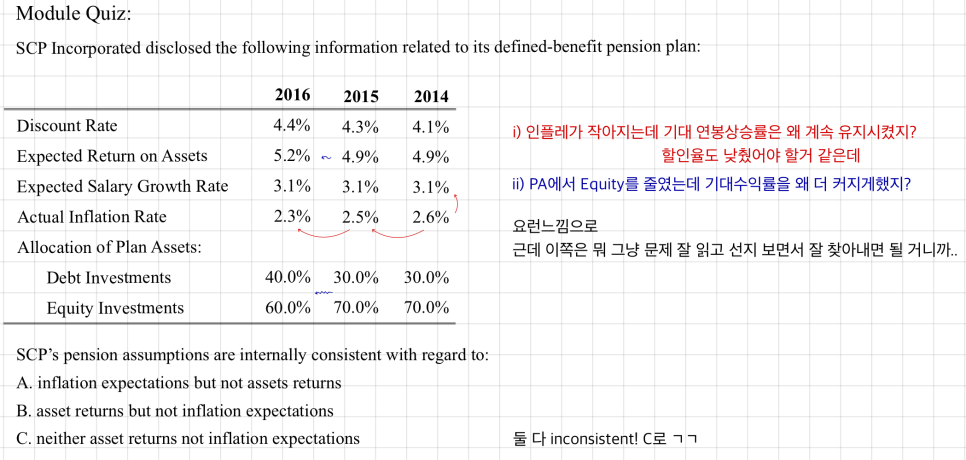

On assumptions in general — the analyst should look at the assumptions the company is using and notice if anything looks inconsistent. So expect a question that asks you to spot the inconsistency.

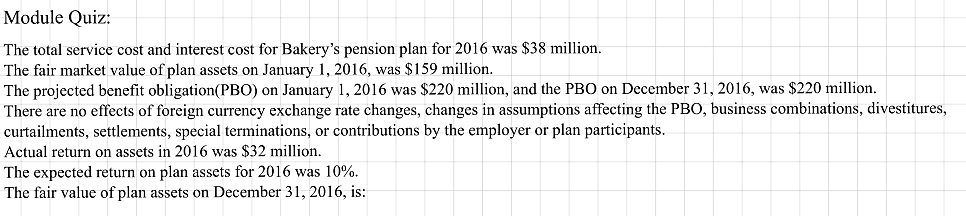

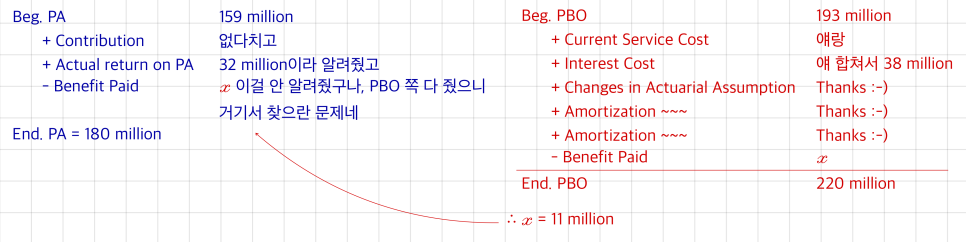

For example, here’s a Module Quiz:

It says this above in really small text, but: all assumptions used in a DB plan are required to be disclosed in the notes (don’t need to go all the way to MD&A).

Risk-related note disclosure about pensions and post-employment benefits → include information about actuarial risks that could lead to differences between the reported obligation and the actual benefit → found in the notes to the F/S This info can be presented as the effects of a change in assumptions, or as sensitivity analysis.

And with that — DB-type retirement pension content is done!

Let’s bang out a few problems on this and then we’ll roll on to the next chunk~

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.