Share-Based Compensation

Picking up with post-employment benefits and share-based comp — breaking down the actuarial stuff, stock options, SARs, and the vesting quirks you actually need to know.

OK so, picking up where we left off, stock options are up next —

But first, let me pause for just a sec.

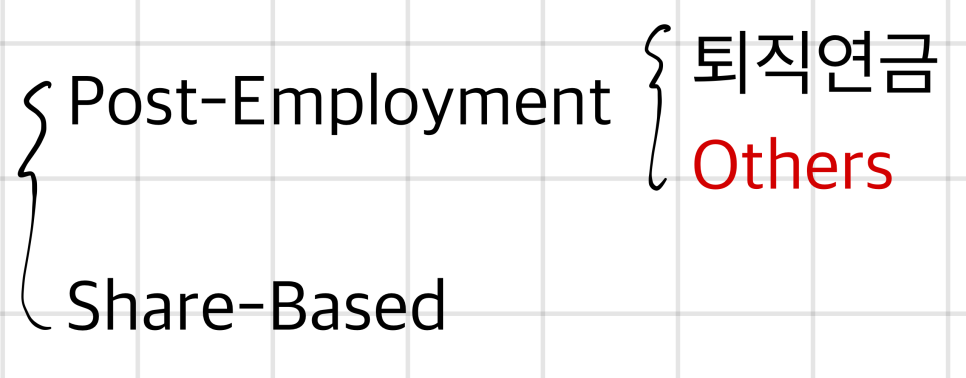

The chapter we’re in for this second theme is called Employee Compensation: Post-Employment and Share-Based, and the way it’s actually broken down is…

So those various odds-and-ends bundled under “Others” — they get like one or two paragraphs each (T_T)

Tuition / Health Care / etc. — stuff that’s not really a thing in Korea but is super common in the US.

And in the US they even have clauses like this..

“Work for our company for 15 years, and no matter when you leave after that, if you ever come down with such-and-such disease, we’ll cover you”

or

“Work for our company for 20 years, and no matter when you leave after that, if your kid goes to college, we’ll cover their Tuition”

Wow.. how on earth do you do accounting for something like that??? lol

If they promised cancer-related support, for instance, you’d have to estimate the probability the employee actually completes that tenure, and when they might get cancer, all of that..

Back in the day, because there were just way too many shaky assumptions stacked into this part, even at the cost of breaking the matching principle of revenues and expenses… they just didn’t account for it at all, and when the actual event happened, then they’d expense it. That’s apparently how it used to work.

Now? None of that.

Just like a DB-type actuary forecasts everything and takes the Present Value, this stuff is aaall estimated piece by piece so that the accounting doesn’t break the matching principle — apparently!

So the change in PBO or Expense for this “other benefit” from changes in Assumptions? Exactly the same drill. You can solve it just like a DB-type problem. The way you’d solve for the effect of the expected wage growth rate on retirement pensions — same as the effect of expected inflation on other benefits. That’s what I mean.

One more thing.

With retirement pensions, as employees keep racking up service years, the benefit keeps building up continuously.

But with these others, once you’ve merely put in some defined period of service, you’ve acquired a kind of right — and the point is that Service Cost gets recognized up until the day that right “Vests.”

And while retirement pensions legally require continuous contributions to be accumulated in a PA, these others aren’t legally mandated like that — so the PBO might be recognized while the PA might not.

Let’s just carry these “others” differences forward in our heads.

When this shows up as a problem, the combo style is: the main course is a DB-type problem, and occasionally one stock option problem gets slipped in. Apparently.

Stock-based compensation actually covers a bunch of things besides stock options — the headliner is stock options, and there’s also Stock Appreciation Right (SAR), Stock Grant, and others. Apparently.

But problems most likely come out as stock options…

✷ Stock options got introduced in Korea in the mid-1990s. The related laws got cleaned up around then too, and the procedures for granting stock options were written into the Commercial Act. Apparently.

✷ Stock options can’t exceed 10% of the company’s total shares. For ventures the ceiling’s a bit higher, and for listed corporations there’s an exception where up to 20% — double — is allowed.

✷ Korean unlisted companies use K-GAAP, and under K-GAAP stock options don’t need to be accounted for — you just disclose them in the notes.. But when they decide to go public, everything has to be converted to IFRS, and suddenly expense recognition kicks in — so apparently this becomes one of those classic IPO-time issues.

✷ This isn’t weird. The US used to not expense stock options either. Microsoft is the textbook example.. Right up to Microsoft’s IPO in 1995, there was zero stock option expense recognition, and so MS’s net income at the time looked like it was surging through the roof. They got their Valuation off of that and listed.

But according to research, “if stock options had been expensed~” — if you redraw the financial statements from that era, MS apparently wouldn’t have posted a single profitable year up to listing. Not one.

When you grant a stock option, there are basically 3 conditions attached. Apparently.

➀ number of shares — how many shares of options to buy

➁ Exercise Price — what the exercise price is

➂ Vesting Period — how much tenure you have to put in to exercise (legally the floor is 2 years (minimum vesting period))

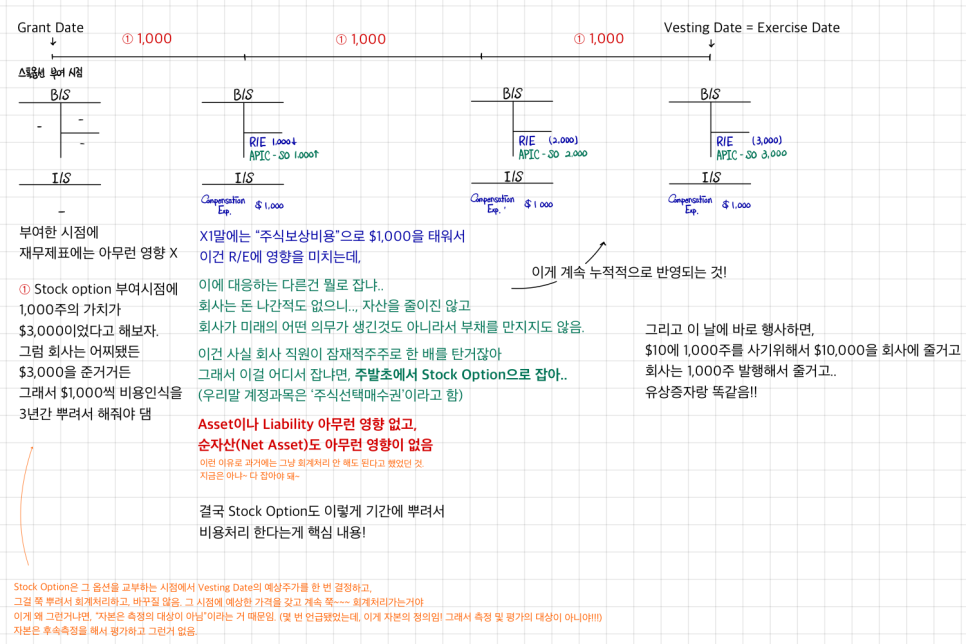

OK so how do we account for this..

➀ the right to buy 1,000 shares

➁ at $10

➂ 3 years from now — say you got a stock option like that.

That employee’s gonna work hard~~ for 3 years so the stock price climbs above $10 after 3 years, and they’ll be compensated for the reward of grinding through those 3 years.

So the accounting..

Because it has to live inside the matching principle of revenues and expenses, the amount that’s compensated 3 years from now also has to be spread out neatly across that 3-year period.

BUT!!!!!!!! Here’s the thing.

No calculation problems!

No accounting treatment!

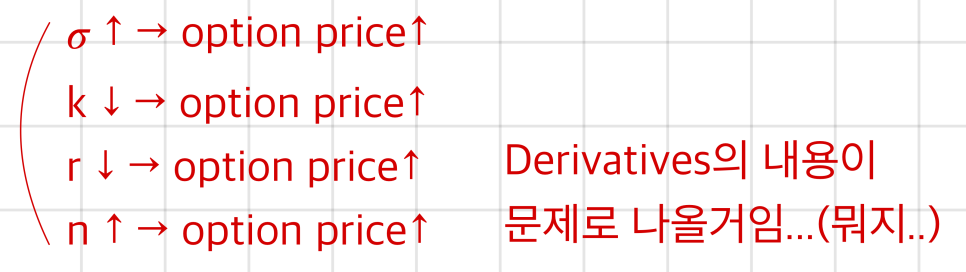

For Stock Options, based on the Black-Scholes equation — what will the Option Price be!

When I studied this part in intermediate accounting originally, this stuff is no joke either, and I figured we’d be going that deep.. lol disappointing — no no no, what a relief!!!

The other share-based comp stuff… nothing really worth calling “content,” lol, more like fun accounting trivia..

Stock Grant is, well, it’s basically the same as a stock option..

You’re giving someone shares and going “they’re yours in 3 years^^ work hard!”

Except when that right vests, a stock option requires you to pony up cash equal to number of shares × exercise price, but a stock grant doesn’t have that — so employees would obviously prefer this.

(In Korea, stock grants are almost nonexistent..)

SAR (Stock Appreciation Right), what is it..

The difference is that it’s tied to the stock price and that difference is just paid out in cash, and the character of it is basically the same as a stock option.

Why did this come about? Apparently it was something that actually happened at a certain unicorn startup recently. Quick version:

The stock options have vested (= conditions satisfied! ready to exercise!!)

I can now buy stocks worth 100 billion won at Fair Value for 1 billion won.

But wait — I don’t have 1 billion won???

In cases like that, the company apparently hooks the employees up with financial institutions to arrange loans.

So I exercise. Then in my account, instead of 100 billion won in cash, I’ve got 100 billion won worth of stock.

Should I sell it right away?

Eh, I’d wait a bit. Could go higher.

But wow — under tax law, when you exercise a Stock Option, whether the gain is realized or unrealized, they slap a tax on that income…

If you exercise while still at the company it’s treated as earned income / if you exercise after leaving it’s treated as other income → and the applied tax rate is different too lol

Anyway, stock options have this kinda crappy side, and what came out of that is SAR. Apparently.

Also — a stock option doesn’t get remeasured along the way.

The reason for that was that it’s classified as equity.

On the other hand, SAR gets recorded as a Liability, and it’s subject to measurement and evaluation.

So it gets remeasured and updated every year.

If the stock price shoots up, the company’s liability keeps ballooning & expense recognition↑ — that’s the accounting treatment it falls into.

This has no shareholder dilution and everything’s clean,

but that’s the burdensome part.

Chapter 2 is done!!!!

That means 2 out of the 3 main pieces are finished~!

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.