Multinational Operations

A quick breakdown of transaction exposure — how FX rate changes hit your AR and what counts as realized vs. unrealized in multinational accounting.

OK so the meat of this chapter is actually foreign subsidiaries — like, you’ve got a sub in another country, how do you apply exchange rates when you consolidate it?

There are two methodologies, and the core of the studying is the Current Rate Method vs the Temporal Method. That’s all part (ii) Translation territory.

But before we get there, there’s one little thing to knock out first.

(i) Transaction Exposure — not a ton of content here. I’m gonna try to wrap this one up in a single page, let’s go.

Transaction Exposure

i) Export Case

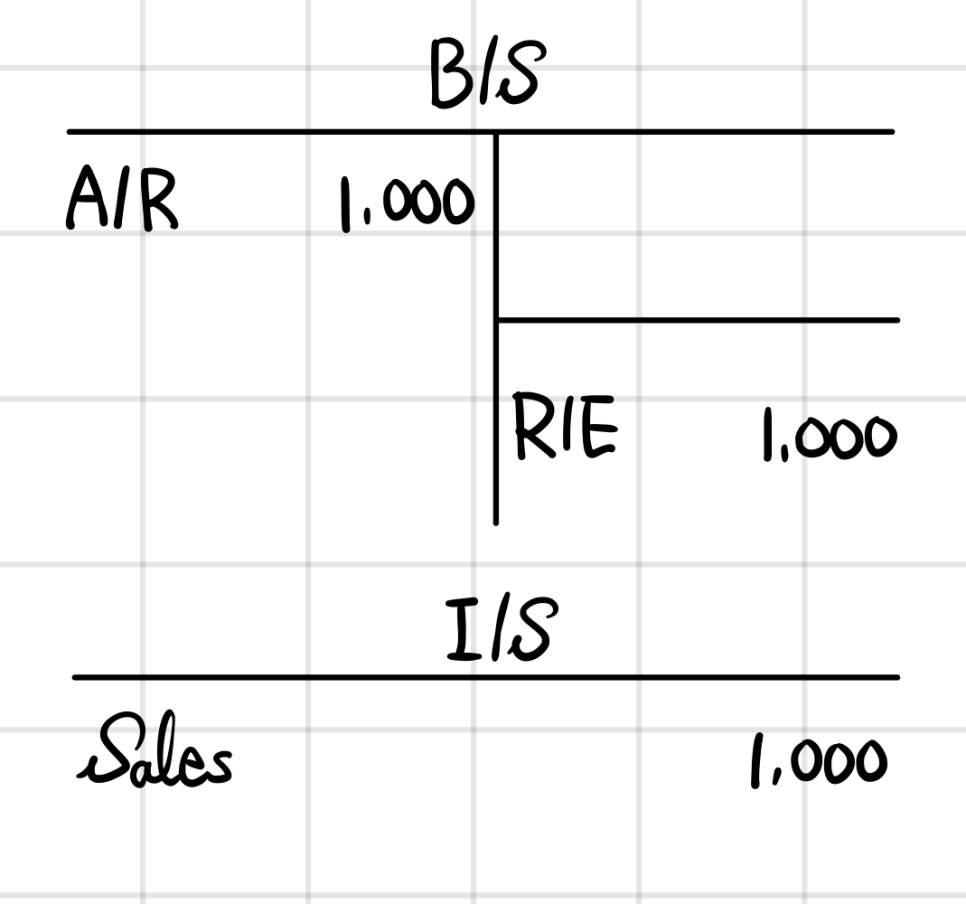

So let’s say it’s a Korean company, and they sold $1 worth of goods at the moment when the exchange rate was 1,000 won/$.

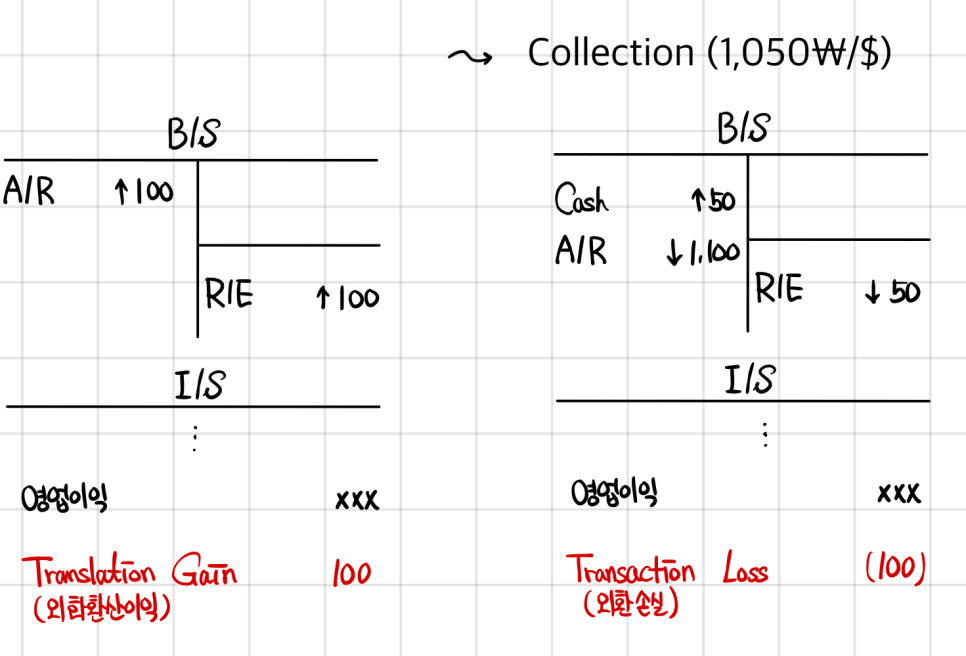

Whoa, but at year-end the rate jumped to 1,100 won/$????

And the cash for that AR hasn’t actually landed yet.

So when we do the financial report, that right-to-receive $1 has to show up as 1,100 won. The extra 100 won? That’s gain from FX fluctuation — it does get reflected in profit or loss for the period.

But — and this is the thing — it does not show up in operating profit.

And then when the $1 actually gets collected, if the rate at that moment is 1,050, that also has to be expressed in won.

In this case we don’t call it a translation gain/loss — it goes in as a Transaction Loss.

Side note — IFRS doesn’t define every single account title one by one. In practice you can journal it like this, or just use the same account title, lol — account titles are honestly not important in the standards.

(Which is why it’s not weird at all that the account titles different companies use are all over the place lol — it’s each company’s own call. Sales revenue, revenue, sales, … however you wanna say it.)

Just for fun, let me toss in an extra bit about FX translation gains:

That bump in the receivable’s value from the rate move — isn’t that an “unrealized gain/loss”? Is it really fine to dump unrealized stuff like this straight into R/E?!

⇒ Actually — there are plenty of unrealized gain/loss items that get reflected straight into R/E heh. FVPL is also unrealized and it goes right into R/E too. The flavor of unrealized stuff that gets stashed in AOCI is more like… “realistically not gonna get realized for a good long while” — that’s the bar.

⇒ And one more thing —

“Hold up, so if I go ask for dividends, I might not get any money?! If everything’s unrealized?!”

OK so when a company tries to pay dividends, what they do first is calculate the distributable profit out of R/E, and in that process, all the accounting unrealized gains are supposed to get subtracted back out.

Classic examples of those: FX fluctuation effects / equity method income / FVPL / etc heh.

So — Translation is still considered unrealized, Transaction is considered realized.

But wait. If a company is 90% export business, currency risk is just… unavoidable for them. Shouldn’t there be cases where you’ve gotta treat this as one of the operating activities too?

So IFRS basically goes “you guys figure out and define what your own operating activities are.”

And in fact, depending on the company, this stuff can get loaded into operating profit.

But it was getting too chaotic out there, so the FSS (Financial Supervisory Service) was apparently like “nah, can’t let that fly.” → “Separate from whatever operating profit you have in your head, here’s a form we defined — fit your numbers to this and submit!”

That’s what’s getting uploaded to DART right now, apparently.

And in that form, those FX losses/gains are supposed to be excluded from operating profit. So instead, companies like this use an account title called “adjusted operating profit,” which is basically saying “this is operating profit using our form, not FSS’s form~” — apparently.

…OK we’ve drifted way off course.

Anyway. We confirmed through the financial statements that for an exporting company, it’s good when the rate goes up, and bad when the rate goes down~

(For an exporter, it’s good when the home currency is weak, and a loss when the home currency is strong!)

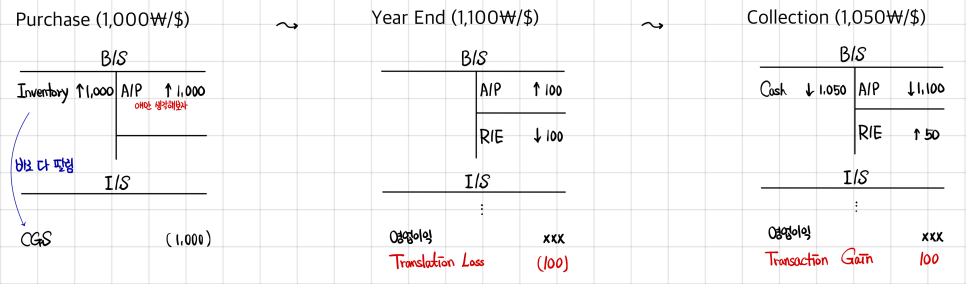

ii) Import Case

A company holding monetary foreign currency liabilities is worse off when the home currency is weak, and better off when the home currency is strong~

…and they’re stretching this across 3 pages. Like — what is this.

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.