The Current Rate Method

A quick rundown of the Current Rate Method — when to use it, how to translate I/S before B/S, and how to make sense of AOCI without overcomplicating it!!

OK so — how do we actually do the translation?! We’ve got two methods to study:

- Current Rate Method

- Temporal Method

This chapter isn’t really about deep theoretical understanding — it’s enough to go “oh, so that’s how you do it” on the technical side and move on. It’s not even that complicated!!

Don’t forget — this is one of those chapters where you just go “ah, in this kind of situation you translate this way, in that kind of situation you translate that way,” and keep moving!!

That said, for exam purposes you do need to have a solid grip on the differences between the two methods!!

- First off, this one is used when the Functional Currency is the same as the Local Currency.

Meaning — the foreign subsidiary is running its business pretty independently,

so the local currency of that foreign sub ends up being the functional currency.

(If the problem says the Subsidiary is independent, or throws around something like “self-contained,” read that as a giant arrow pointing at this method.)

- Once you’ve decided you’re going with this one,

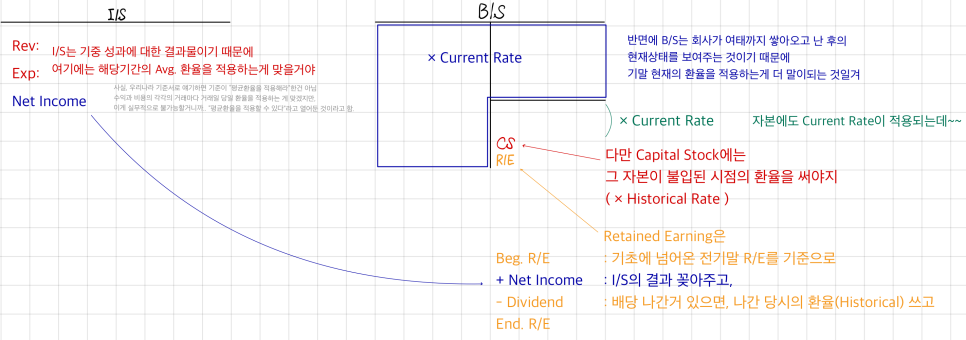

Translate the I/S first → then the B/S, in that order!!

Oof.. yeah it looks like a lot lol

But there’s nothing logically weird going on, so I don’t think it’s actually hard.

Anyway, if you stare at the B/S as a whole —

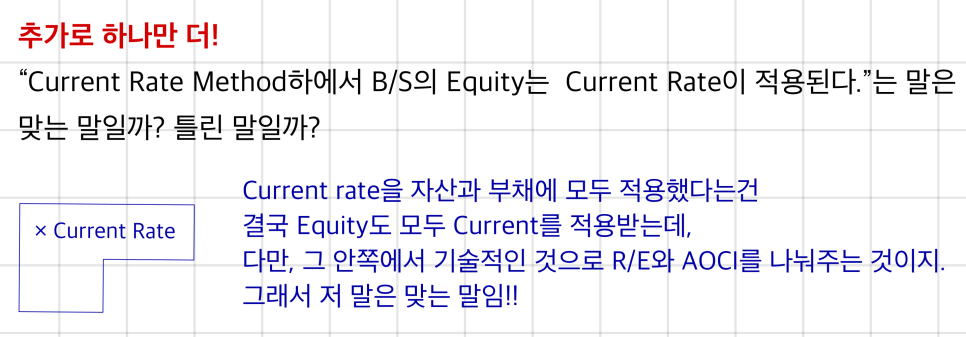

the exchange rates being applied are all different, so of course debits and credits aren’t going to balance,

and the plug value that makes it balance gets dumped into AOCI.

The account name? Foreign Currency Translation Adjustment.

AOCI is a value calculated on the B/S, which means it’s a “cumulative balance,”

so if the problem asks for “OCI occurring in the current period,” you’ve got to compute OCI as the difference between the cumulative balance at the end of the prior period and the cumulative balance this time around!

When this gets turned into an exam question,

they’ll give you the foreign sub’s financial statements

→ then list out all the exchange rates by type

→ and ask you for AOCI, right? ok ok.

But just in case a problem

only asks whether AOCI is positive or negative —

cranking out a full detailed calculation you weren’t even asked for would be a total waste..

You can think about this simply and move on.

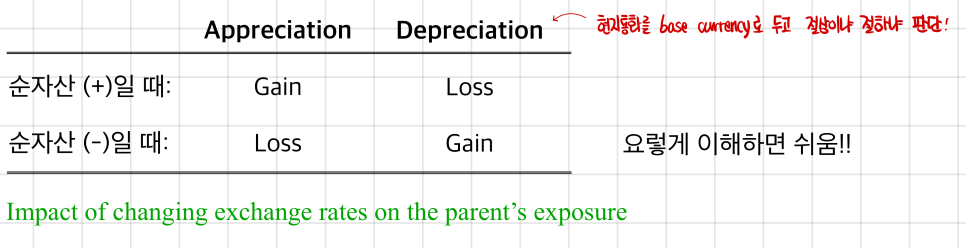

If you think about it this way — the foreign sub’s Net Assets can be understood as being exposed to the local exchange rate. Then, depending on whether the Net Assets are strong or weak —

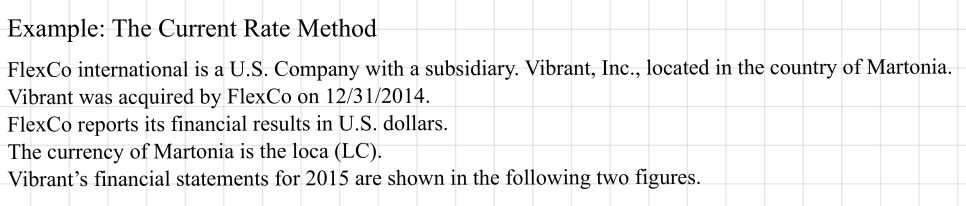

The majority of Vibrant’s operational, financial, and investment decisions are made locally in Martonia,

although Vibrant does rely on FlexCo for information technology expertise.

Use the appropriate method to translate Vibrant’s 2015 balance sheet and income statement into U.S. dollars.

I/S first!!!

Vibrant is a subsidiary of FlexCo (acquired at the start of 2015),

and all the operating/financing/investing decisions are being made at the sub itself,

so → that’s a green light for the Current Method.

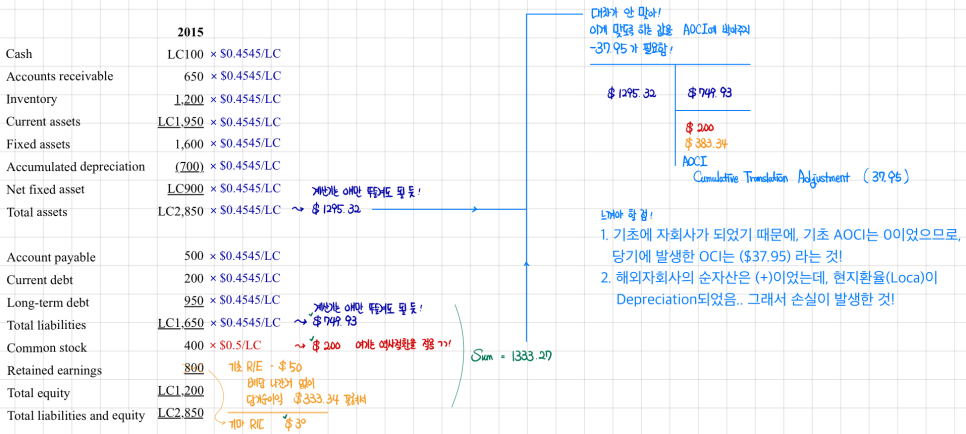

So let’s kick things off by multiplying everything on the I/S by the average exchange rate!

Every line item gets hit with Avg. rate = $0.4762/LC,

Net Income($) = LC700 × $0.4762/LC = $333.34

And even though they handed us individual historical rates for PPE and inventory,

that kind of trap is meaningless~~ not gonna work~~

For everything except Common Stock and Retained Earnings,

we just slap on the Current Rate — the end-of-2015 exchange rate (a.k.a. the closing rate)!

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.