The Temporal Method

Breaking down the Temporal Method — when to use it, which assets get translated at what rate, and how to snap to a gain/loss answer fast on the CFA.

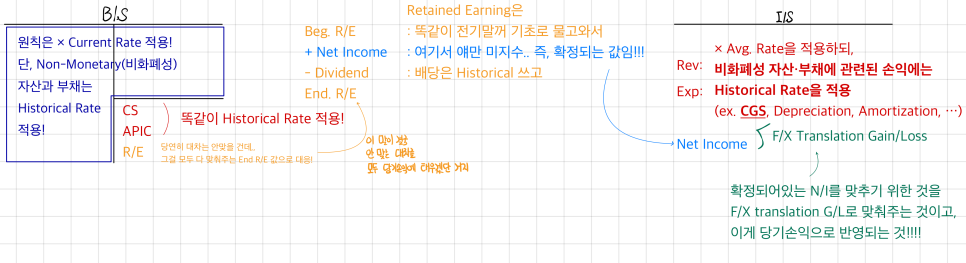

Temporal Method (Remeasurement)

The book also called this thing “Remeasurement” — so what is it, actually?

1. You use this method when the foreign sub’s Functional Currency lines up with the Presentation Currency (FC = PC), AND the currency the sub actually makes decisions in is the parent’s Functional Currency.

Translation: the sub mostly transacts with the parent. It’s basically a dependent of the parent.

So: Subsidiary → Dependent / well-integrated into parent.

A sentence phrased like that is your tell — that’s the problem nudging you toward Temporal.

In real life, figuring out what the Functional Currency actually is… yeah, not easy at all.

But generally, the FC of an overseas sub is the local currency, and Temporal Method doesn’t really show up that often.. heh.

2. Once you’ve decided to use this method, the order of translation is:

translate the B/S first → then the I/S,

which is the reverse of the Current Method.

And the gains/losses that pop out here? Not OCI. They land straight in current period P/L!

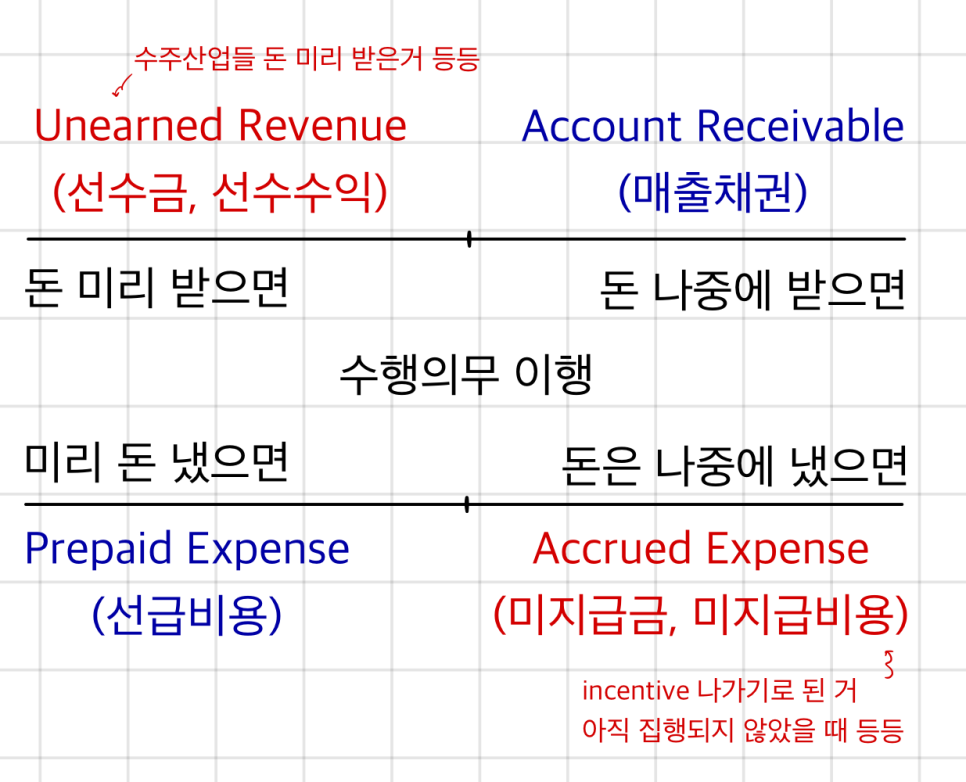

“Non-monetary” means: the value moves with inflation/deflation, in the same direction. That’s what gets the non-monetary label.

Not stuff like Cash, Receivable, Payable — but inventory. When prices go up, you sell it at the higher price, right? Land works the same way — classic non-monetary.

Non-monetary assets to keep in your head for CFA:

Inventory / P.P.E. / Intangible Asset / Unearned Revenue

Same deal here — if the question only wants to know whether that F/X translation is a Gain or a Loss, you need a way to snap to the answer without translating every line item one by one!!!

Let’s look.

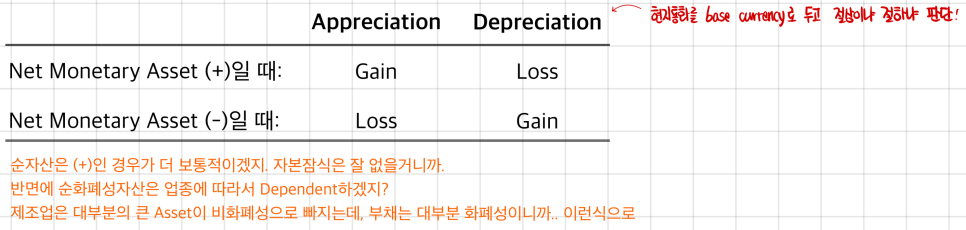

In the Current Rate Method, the entire net assets of the foreign sub were exposed to the Current Rate. All of it.

In Temporal Method, not all assets and liabilities are exposed to the Current Rate. Only the monetary ones are.

So for this one, you can quickly call (+)/(-) based on Appreciation/Depreciation just by checking whether Net Monetary Asset is (+) or (-)!

The exam doesn’t ask the Why, but let’s spend a sec on the Why anyway and actually get it.

(Now that we’ve also covered Temporal, this should click — heh heh.)

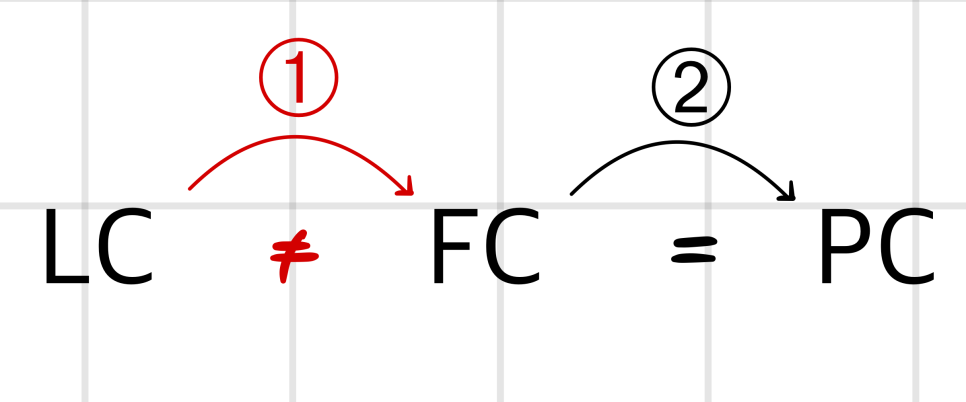

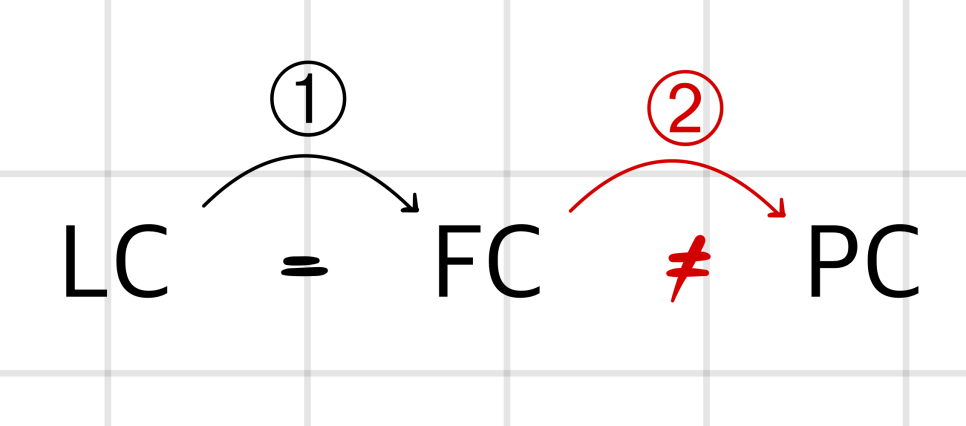

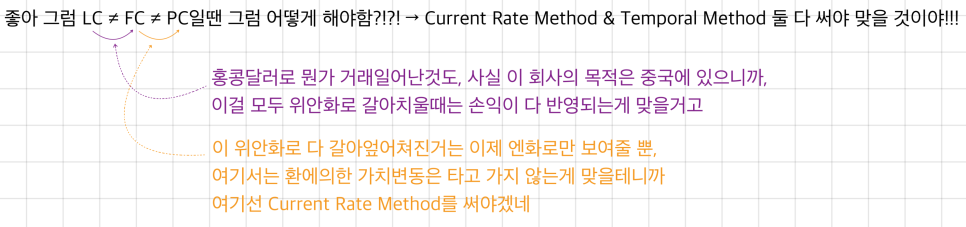

The setup: [ LC ≠ FC ≠ PC ]

A Japanese company → spins up a subsidiary in Hong Kong → for the purpose of breaking into the Chinese market (China is socialist, so having a legal entity in China is… you know).

In this case, when the Japanese parent wants to consolidate the Hong Kong sub, what’s the right way to translate?

I’m gonna think this through with plain common-sense intuition.

That is: I want to figure out how to handle LC ≠ FC ≠ PC, and I’ll build the logic by warming up with 1. LC ≠ FC = PC and 2. LC = FC ≠ PC first!!!

But before that —

Suppose the sub has some assets and liabilities sitting on its books, and you just slap the current exchange rate on every single one of them…

There are obviously monetary and non-monetary items mixed in there. If you don’t distinguish, just smash the current rate on everything, and then dump the whole thing into AOCI — then F/X gains and losses don’t get reflected at aaall.

Because when you hold something in monetary form, there’s clearly a value change as the exchange rate moves. Think about it that way and Temporal Method starts making sense. OK OK.

Alright — case 1. The Hong Kong sub only transacts with the Japanese parent.

Then depending on whether the yen (= the Functional Currency) appreciates or depreciates, it makes total sense to split monetary/non-monetary and recognize a Loss/Gain!!

It’s right that gains and losses should pop out here.

Case 2. The Hong Kong sub is being run independently, all its action happening in Hong Kong.

Then the vibe is: “I do my economic activities in a different country’s currency, that’s just my life. But the parent is dragging me along!!”

In that case, since you’re just converting FC to PC, when you’re getting dragged along, there shouldn’t be a value change. Only the currency you’re displayed in changes.

OK now let’s flip through the book a bit and skim what’s worth reading at least once.

The functional currency is picked by management — meaning it might not be totally objective. Per IASB, management should consider:

✔ The currency that influences sales prices of goods and services ✔ The currency of the country whose competitive forces and regulations mainly drive the sales price of goods and services ✔ The currency that influences labor, material, and other costs ✔ The currency in which funds are generated ✔ The currency in which receipts from operating activities usually get retained

For FASB, it gets a “similar~” treatment, like, that level of mention.

Anyway — this is just to show that yes, there’s guidance for this in the standards.

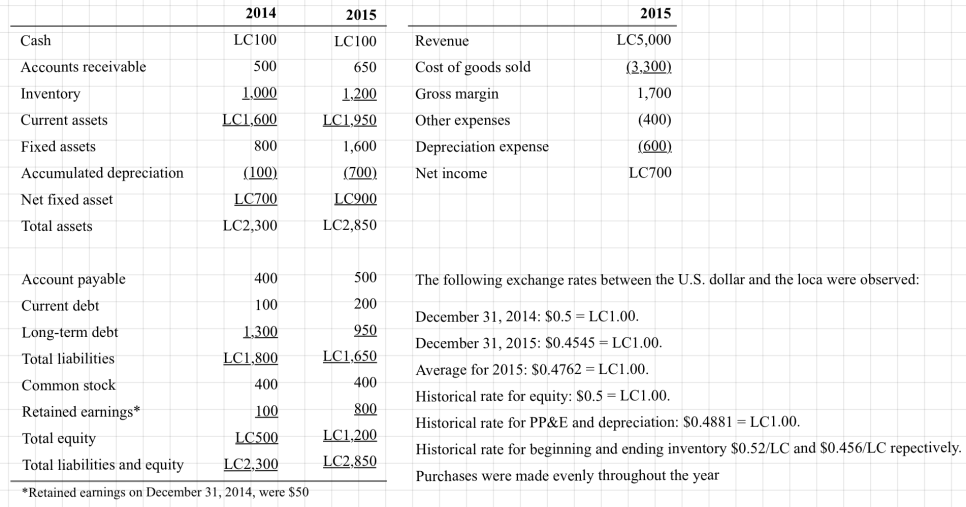

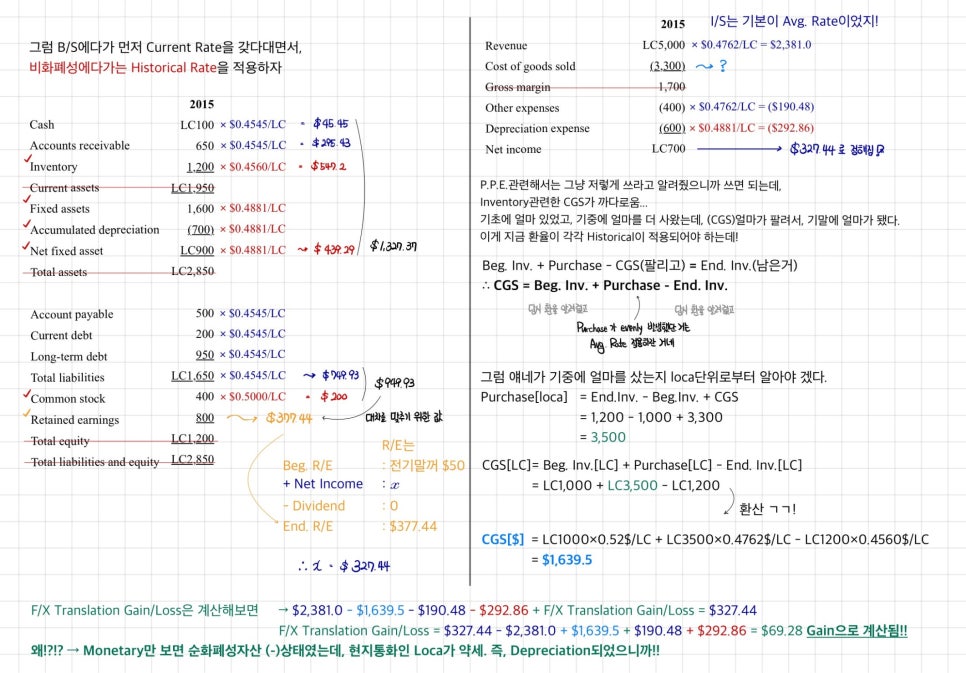

Inventory and COGS Under Temporal

I bled through practice problems on this one. As a poster-child monetary/non-monetary expense, COGS supposedly applies the historical rate — but here’s the thing: a FIFO company and a LIFO company end up in different situations. Under FIFO, the goods being sold off are the old ones (so old exchange rates apply). Under LIFO, the goods being sold off are the recent ones (so recent exchange rates apply).

What the author is really saying:

“Hey buddy, under the Current Method we used Avg. Rate, so this whole issue didn’t even come up. But Temporal applies Historical — so this kind of issue shows up too ^^”

That’s the message, I think → I’ll work through a word-problem-style example below, so don’t sweat it!

I’d say that’s about all there is to read on this page, so let’s get back to grinding more problems..!

A foreign subsidiary is operating in a country where the local currency is depreciating relative to the parent’s presentation currency. Assuming the subsidiary is a FIFO firm, which accounting method will result in the highest gross profit margin reported in the parent’s consolidated income statement?

A. Current rate method B. Temporal method C. The current rate method and the temporal method will result in the same COGS

The sub is in a country where the currency has depreciated, and they’re a FIFO firm.

Which one — Current Rate or Temporal — gives the higher gross profit margin?!

Sales: ← both methods apply Avg. Rate to this.

COGS: ← Current Rate: Avg. Rate / Temporal: Hist. Rate.

Under Temporal, you apply the old exchange rate. And the fact that the currency is now weak means: the smaller the recent rate is compared to back then, the smaller the cost ends up.

Say a cost of 13,000 won was incurred:

- Won appreciated: at 1,000 ₩/$ → $13 of cost recognized

- Won depreciated: at 1,300 ₩/$ → $10 of cost recognized

By the way — that whole move of borrowing money and shoving it out as dividends? It’s called “recapitalization (recap)”. It was apparently a fast-exit play that got popular among American IBs for a stretch.

Lone Star pulled this exact thing when they came into Korea, and their whole game was: exit before maturity, full stop.

And these days there’s also this thing called dividend-in-kind — so apparently they take a company’s most prized assets as the dividend itself. (It’s a way of shrinking assets and squeezing R/E down..)

Like, say you walked in as a shareholder with ~100 billion invested, and there’s an 80-billion-won building sitting on the books. You exit with the building first, then you start.

Survival of the company? Not on the agenda. Only the exit. (People commonly call this “eat and run”.)

A vulture is the bird that picks at a corpse’s organs, so — that’s why these guys are called vulture funds. (a.k.a. corporate raiders.)

When Lone Star bought Kukdong Construction, they came in with 80 billion, and not long after the acquisition, they sold the Kukdong Construction headquarters for 80 billion and yanked the money out.

And they didn’t even pull it via dividends — they used a capital reduction. If you pull from R/E, taxes wreck you. But via capital reduction, you only get taxed on the gap above the investment principal..

If the assets looked thin and even a paid-in capital reduction wouldn’t fly, then — yep — you borrow money using the company itself as collateral, and pull the cash out that way.. haha.

In cases like this, the stock price actually pops a fair bit, apparently. People often invoke the “disciplinary effect of debt” here.

Logic being: load up on debt and now you have the justification to cut costs. Justification to lower salaries, gut research budgets, restructure, the whole package — all in the name of cost reduction..

“Manage by the Numbers, Vol. 2 — from ‘What Is the Right Level of Dividends?’:”

Recap as a defense against hostile takeover attempts??? lmaooo. Who burns down their own house because they’re worried about a burglar..

Apparently almost no one actually does it that way in practice.

There are cases where it was used to push through deliberate restructuring. The classic one is Sealed Air in the US, 1989. Sealed Air’s CEO was the largest shareholder himself, so not only did he pocket a fat slug of cash through the dividend, he deliberately threw the company into crisis mode — manufacturing the justification to do large-scale restructuring. The whole intent was supposedly to crank up management efficiency.

(Stock was at $45 — they fired off a $40-per-share dividend! The dividend was financed entirely with bank loans.)

(Lucky for them no economic crisis was overlapping at the time — if this had hit 2008, the company probably just goes under…)

And in the end, the only ones really eating the damage would’ve been the employees who had no choice but to absorb the restructuring..

Originally written in Korean on my Naver blog (2025-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.