Time Value of Money

A fun, casual walkthrough of time value of money concepts — future value, present value, and the compound value interest factor (CVIF) explained with zero boring.

So now let’s properly look at the techniques used in the financial management field regarding time value of money.

First, starting slowly from the concept of ‘money swells up!‘

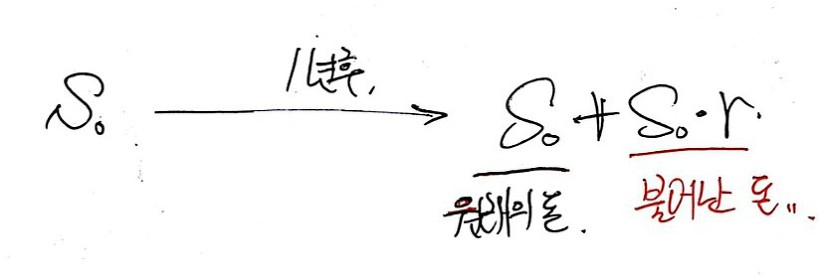

Let’s say I currently have S amount of money.

And if we call the deposit interest rate at commercial banks r,

are we going to keep the S amount of money we have at home in a safe, or in the trunk of our car??

Did we commit a crime?? If it’s not money received through shady routes, we’d put it in the bank, right?

Then, with the deposit interest rate applied, the money will grow by that amount.

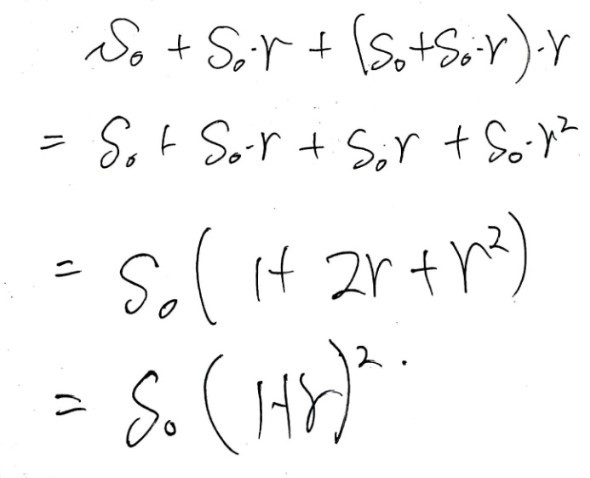

Alright, so let’s say we left S in there for 2 years, juuuust~~~~ like that~

(Of course, assuming the interest rate is constant at r)

Let me organize it prettily~

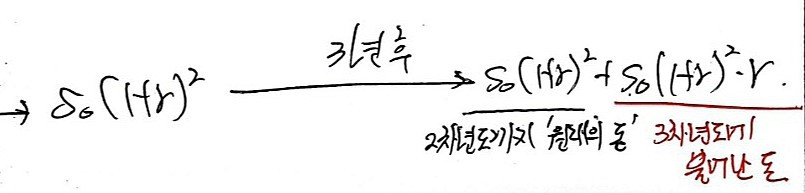

Should we try 3 years later too?????

If we calculate that prettily,

Since we learned sequences in high school,

by checking up to the 3rd year

(as long as the interest rate is constant at r,)

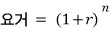

we figured out that there’s a rule

and after n years, the value of S

will become this — we can be confident of that…

By plugging any natural number into n,

we can figure out what the value of S becomes after an arbitrary amount of time has passed.

That’s right — “this guy”

All you had to do was multiply by this guy!!!!!

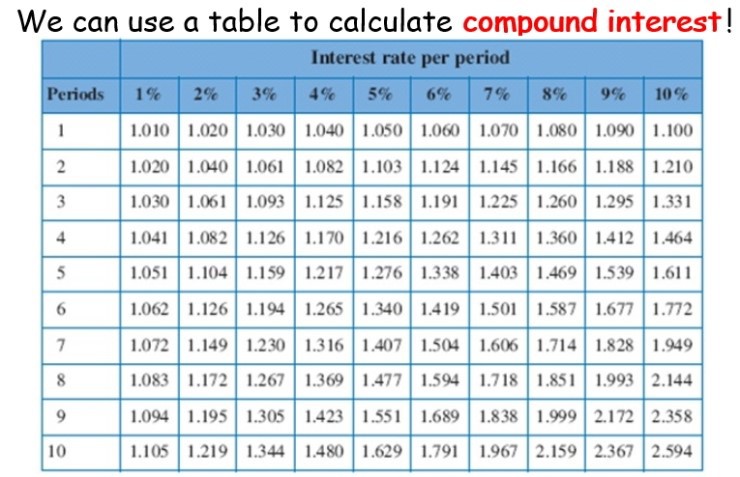

We now call this ’this guy’ the “compound value interest factor: CVIF”, apparently.

These days, you can very easily derive the value just by hitting the calculator,

but people in the old days couldn’t possibly have calculators like the ones we have now…

Our ancestors probably used something like this

(from. http://slideplayer.com/slide/9016453/)

Oh my goodness………….

What we did up there was about ‘future value.’

“I currently have S in money — what will it be worth after n years?”

— that was the answer to this, so calling it future value shouldn’t stir up any controversy.

Alright. Now, present value…

What question is this the answer to? It goes:

“Yum yum, my friend says he’ll give me P after n years — so in present terms, how much should I say that is?” — that’ll be the answer to this.

<A fun side story, by the way>

The professor asked a question: do you know why geometry developed?

Geometry is that thing — that guy Euclid, who said the sum of interior angles of a triangle is 180˚,

and blah blah about quadrilaterals, that stuff we brought compasses to class for in middle school and drew circles,

that stuff… drawing pictures? That’s what (Euclidean) geometry is,

and apparently this is a discipline that developed rapidly way back in the day through all that war and territorial expansion.

After expanding their land, they’d say

“Hey~ slave~ I’m curious how much land I own. Go measure it and come back~~~”

“Yes, my lord~~~”

The size of the land that could be measured like this

kept getting bigger and bigger,

“Hey~~ slave~~~ I’m curious about my land again. This time, run around it and come back~~~~”

“Yes~ my lord~~~”

Doing this, now that the land had gotten so huge, it probably happened a lot that the slave, once sent, wouldn’t come back…?

As this went on, they’d hire smart commoners and go, “calculate for me♡”

They probably did that. Well anyway, geometry is an aristocratic discipline that started this way, he said.

I was trying to talk about ‘converting to present value….’ right now, … why is this kind of story suddenly coming up…..

It’s related.

Even in the old days, although most transactions were barter exchanges, there were contract transactions too.

A lot of them.

Apparently there’s even a record of an ‘options trade’ left from BC times???(If you look up the story of the philosopher Thales, you can find out exactly about it. This record is said to be humanity’s first options trade record.)

This kind of financial content related to present value is also definitely an ‘aristocratic discipline.’

They probably hired smart commoners and asked them

“Hey, I’ve got this contract right now~”, or “Hey, I’m supposed to get some money a few years from now~”

“How much… how much is this contract, this promise worth? Convert it to money…. money is what matters to me, money!! Money money money!!!!”

Coming back.

Where was I,

“Yum yum, my friend says he’ll give me P after n years — so in present terms, how much should I say that is?”

— that’ll be the answer to this.

I was saying that, and then I suddenly veered off somewhere else…hehe.

Anyway, so let me twist that question slightly and change it into an equivalent question.

P amount of money comes in after n years. ↔ “If I had ‘how much’ now, would it become P after n years?“

If we answer the latter, that answer can be considered the answer to the original question too.

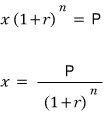

Let’s say we have x in the present.

The value after n years

will be this

Then, since all we need to do is find the unknown x that makes this

equal to P,

we can figure it out with a simple equation

Done

Now putting it simply, it comes out to this.

“The present value of P flowing in after n years is

— is the samey-same.”

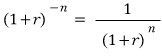

In other words, if you’re just curious about present value, all you have to do is multiply by ’that thing.’

So~~~ this time, “that guy”

The ’that guy’ here will be

and that guy is called the “present value interest factor: PVIF”, apparently.

Whether it’s CVIF or PVIF, it’s the same story, and the derivation isn’t hard either, so I think this much should be enough.

But what we need to watch out for here is

there was an assumption that came along with this

we need to keep in mind that there was an assumption that the interest rate is constant at r for n years.

So now we’ll end up using expressions like this a lot.

The value of P to be received after 5 years, “discounted” at interest rate r,

is this.

Stuff like this…..

- When we use ‘discount’ in this way,

it’ll probably be used to mean something like shaving it down taking time value into account.

If up to that point it was the future value of a single S

or the present value of a single P,

here now it’s not single anymore. It’s multiple.

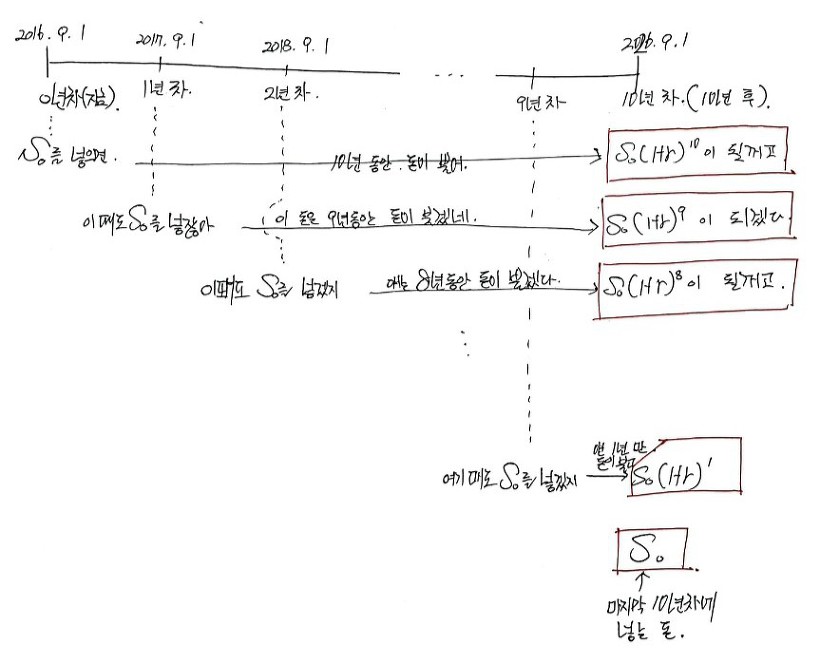

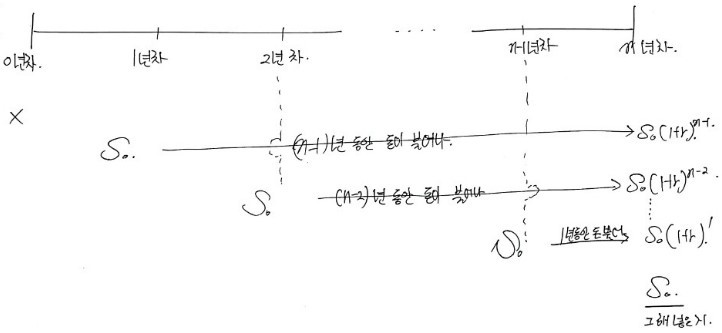

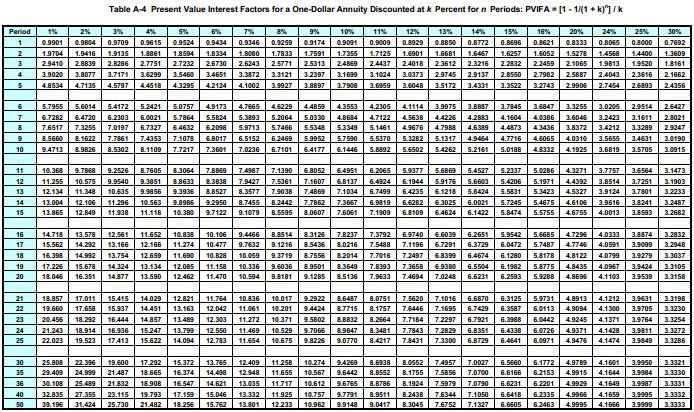

For example, if you put in S every year faithfully, what happens to the value after 10 years?

You put in S 10 times, so the value after 10 years is 10 Ss, i.e., 10S.

— saying that would be elementary-school level…

Taking the interest rate into account and speaking like a high schooler,

you draw a picture like this

When the math teacher in high school drew pictures like that,

I’d get a freaking nuclear brain-meltdown and just sleep,

and now here I am drawing it myself..T_T T_T

Ah… how time flies….

Anyway, since the sum of all the values piled up in the 10th year is

“the value after 10 years,”

we can say,

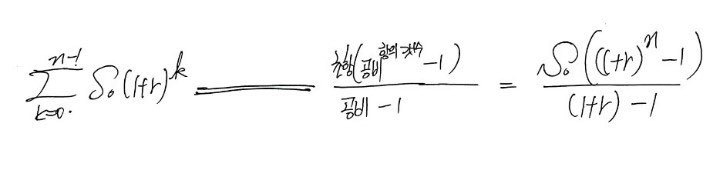

OK, let’s add them all up.

Let’s stylishly write out the sigma first — booom~~~~

Huh?! It’s probably different from the book.

I deliberately threw out an example that differs from the book at the start.

Why? Because the difference that comes from whether money goes in at year 0 (now) or not

— to show that you absolutely have to keep that in mind?

(No… actually I made a mistake…. I accidentally put S at year 0…heh.hehe Actually it’s all my mistake lolololololol)

Anyway, in problems

you’ve got to grasp things accurately and then solve them….sigh..,

a sloppy guy like me……

really should just die, seriously…ugghhh,,,aminer aingneo iann mineo ingh na

But from now on, if it’s said without special conditions, like r=6%, n=10,

we’ll go with the default that nothing goes in at year 0.

(I don’t know why, but why is this book written that way?)

Then I’ll derive the value after n years of putting in S each year starting next year (the annuity-like thing).

OKOKO this time it’ll come out properly

the result I want

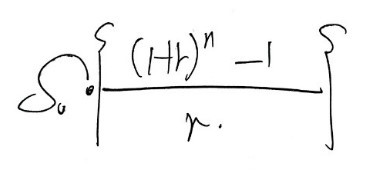

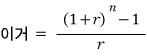

If we sum all the values at year n,

Yep, it came out.

It’s the value after n years.

In this case too,

“Hey, if you save the same S every year, and the interest rate stays constant at r during that period,”

we can say S × “this thing”,

and since the “this thing” here

can be given as the answer,

this ’this thing’ here is called the compound value interest factor an annuity: CVIFA, apparently.

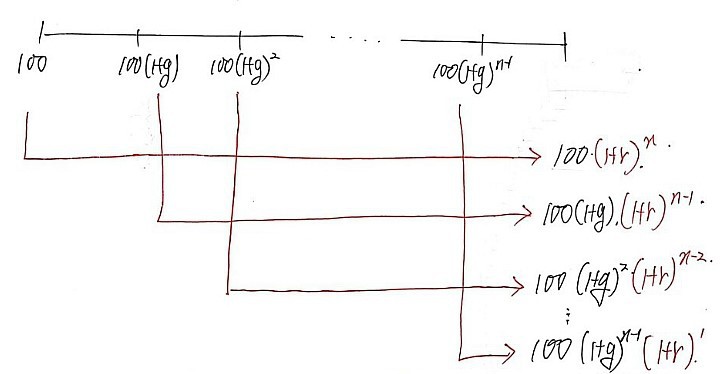

By the way, this CVIFA also has a table that looks like something our ancestors would’ve used lolol shudder shudder shudder shudder

(from. http://eroleplay.ru/pvifa-table-PDF.html.)

shudder shudder shudder….

Ah damn, why are there so many–

I’ll move on quickly.

Now what’s the situation this time,

bread-shuttle??? Ah, this example is a bit violent.

Aaaaah let’s say you won the annuity lottery.

Starting next year, you’re told 5 million won will come in every year

Now I’ll just kinda sloppily skip over with pictures,

derive the formula with the geometric series sum formula, introduce only the factor name, and move on quickly.

You’re supposed to receive 5 million won every year for n years, but you nag to get it all at once.

Since it’s 5 million won × n times, would it be reasonable to ask for 5n million won?

NoNo, it wouldn’t, right?

It seems reasonable to ask for all the sums after returning every one of those 5 million wons over n years to present value.

OK so, kinda sloppily

skipping through with a picture, smashing out the geometric formula… I’ll do it that way (still a lot left…T_T T_T)

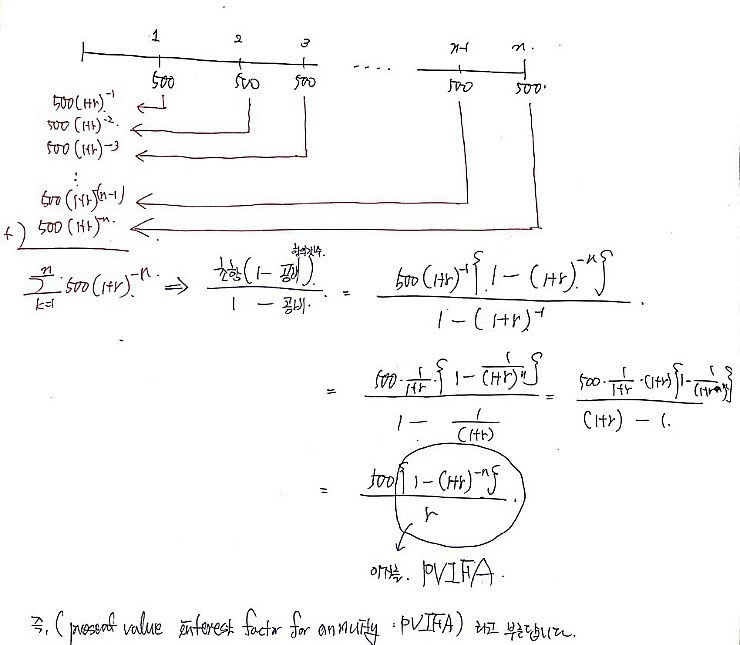

Alright, so what if it’s a pension received perpetually???(As a real example, apparently there’s something called a perpetual bond.)

In the formula above, can’t we just send the existing n to infinity??????????????/

If we take the limit,,,,

Too simple!!!

It’s so simple there isn’t even a factor or anything!

Let’s move on quickly!!!

This time, actually, regarding “irregular cash flows,”

we have to discuss future value and present value,

but as the word “irregular” implies,

it’s like saying hopeless….

…. there’s really no… answer for irregular cash flows.

But if it’s not irregular but ’non-constant,’ and within that non-constancy we can find some kind of rule and calculate, …?

In other words, we’ll think about non-constant, not irregular.

It’s non-constant, but we’re discussing “cash flows that grow at a constant rate” — non-constant, but with a rule.

But the principle is the same.

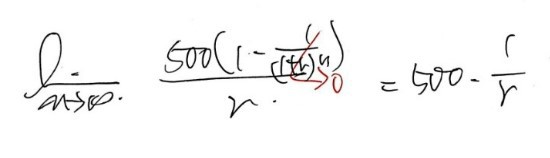

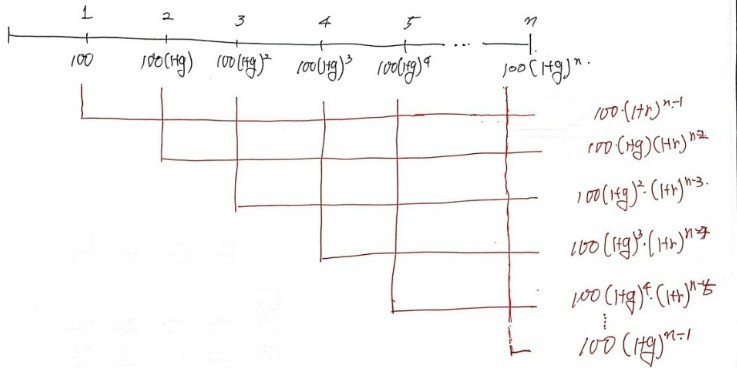

We’re going to save for n years, and the money will grow at a constant rate g as we save.

That is, if it’s 1 million won in year 1,

in year 2 we save 100(1+g) million won, increased by g%,

in year 3 we put in 100(1+g)^2 million won,

and in year n, we’ll put in 100(1+g)^(n-1) — that’s what it means!!!!!!

In. that. case.!

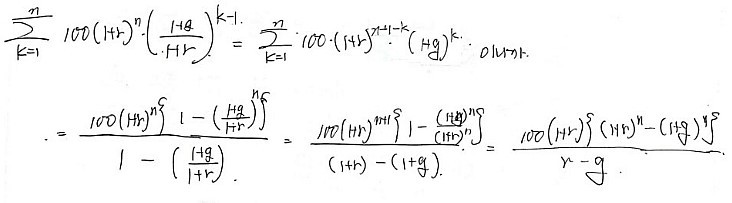

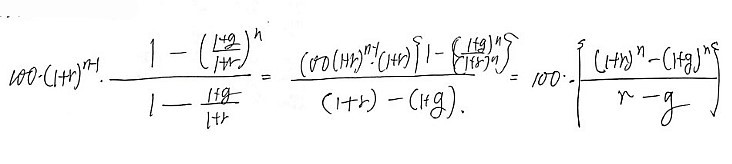

Let’s first check the future value after n years! (Same old — smash the picture in, then lightly smash the geometric series formula.)

Oho, looking at this, I can tell right away —

the first term is 100(1+r)^n,

and the common ratio is (1+g/1+r) — it’s a geometric sequence!!!

The number of terms is n!!!

Oh yeah~~~ it’s doneee~~~~

What if payment were starting from next year?

Then the first term is 100(1+r)^(n-1), the common ratio is (1+g/1+r), the count is n, so

Wow~~~~~~~~~~

It’s~~~~~~ do~~~~~ ne~~~~~

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.