Valuation of Bonds and Stocks

Breaking down how to slap a price tag on bonds and stocks using present value formulas — and yes, yield to maturity is just as annoying to solve as it sounds.

Earlier I said finance is a noble discipline, where

the nobles would ask some sharp lower-class person

“Hey~ I’m supposed to receive such-and-such amount in a few years, convert for me in money how much that’s worth to me right now!!!!“

or

“Hey~ I signed such-and-such contract, convert for me in money how much that’s worth to me right now!”

This chapter is in the same vein

“Yoyo~~ you lowly GD who isn’t even that sharp~~~ I’ll use this as the final judgment on whether to sell you off elsewhere or not”

“I currently have such-and-such bonds~~~ and such-and-such stocks, convert for me how much having these is the same as having ‘right now’!!!!!!!!!!! Before I sell you off somewhere else!!!!!!!!!!“

If I were asked a question like this,….

I’d hope to be sold off quickly…. hell-Joseon…. ugh………

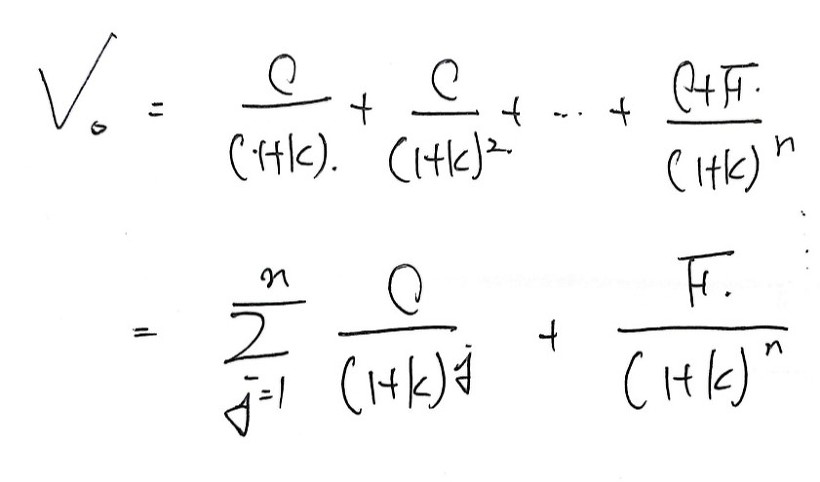

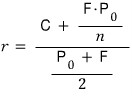

- Bond Valuation Model

: The value of a bond is defined as the sum of the present values of the expected future cash flows from holding the bond.

(Doesn’t this definition feel like something??? Kind of like when a math major fires off a proof???? ‘plausible plausible’ lolololololololol)

If we say there’s a bond like this,

holding one sheet of that piece of paper is equivalent in value to

V_0 : value

C : face-value coupon amount (coupon rate × face value)

F : face value

k : market interest rate (discount rate)

n : bond maturity

As you can see from this formula, the factors determining a bond’s value are C, F, n, k,

and excluding the discount rate k, the other three are factors already determined at the bond’s issuance,

the discount rate, that is, the market interest rate, is a factor that changes according to market conditions!!! Oh ho!!

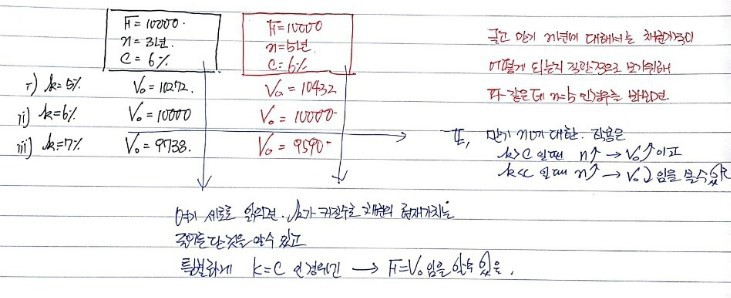

Then, to see how the bond price changes with respect to the market interest rate,

for a bond with face value 10,000 won, 3-year maturity, coupon rate (face-value interest rate) 6%,

if we calculate for k=5% and k=7% respectively,

we can get a feel for it

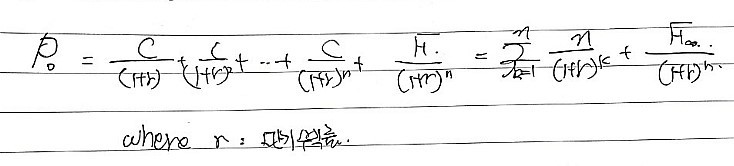

- Yield to Maturity of a Bond

: The yield to maturity of a bond refers to the discount rate at which the bond’s value — the present value of the cash flows arising from investing in the bond —

equals the bond’s market price

!!!

→ Ah, so they basically call the interest rate that makes it equal to the bond’s market value the yield to maturity, huh?

That is, the way to calculate it is

(When solving a problem, everything except r in here gets replaced with numbers. And we find the r that satisfies the equation and we say we’ve found the yield to maturity)

But this yield to maturity is hella tricky to calculate…..

Can’t do it by hand, probably have to run programming…

Go on, plug in n=4 and try solving the equation, see if this equation solves…

http://gdpresent.blog.me/220835676064

Derivatives I Studied Chapter 4. Interest Rates

quiz 1. The bank interest rate is 14% per year on a quarterly compounding basis. This interest rate, a) on a continuous compounding basis, …

blog.naver.com

Looking at the solution to Prob 4.12 at the veeeeeery bottom of this post might help, so I’m linking it.

Anyway, I said there that calculating this exactly by hand is nearly impossible,

so I did a Taylor series expansion to at least find an approximation,

uh….. and here in financial management

they threw out one formula for finding an approximate value for this yield to maturity

They gave an approximation formula

They say this is the approximation formula for the yield to maturity,

and I actually thought this formula was an approximation formula fit via Taylor series expansion,

but apparently not…. so now… T_T I don’t know how this formula was derived T_T T_T T_T T_T ugh ugh

If any of you readers know how this approximation formula was derived,

please teach me T_T T_T T_T I’ll learn a thing or two. Thanks~

So now the bond valuation part is done, done.

So to summarize, what the first bond valuation formula above

means is,

using the given bond conditions, you calculate the present value

and then by comparing it with the “price” at which the bond is actually being sold in reality,

it lets you think about whether it’s overvalued, undervalued, or appropriately priced,

and the second, yield to maturity, is what,

you plug in the given bond conditions and the current selling price of the bond

and calculate the yield to maturity,

“Ah, so holding that bond is the same as earning this much yield to maturity”

lets you think like this….

Anyway… well….

This bond talk isn’t just here, it comes up in almost every finance class,

so this isn’t the first time, and it’s super…. boring but. T_T

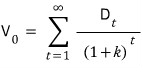

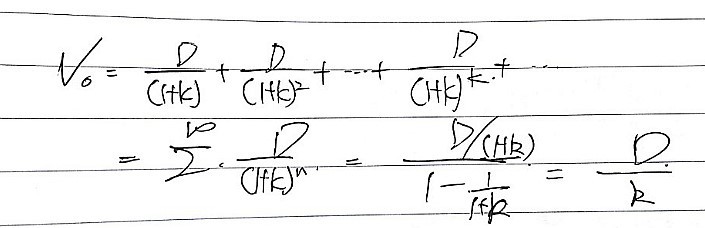

- Stock Valuation

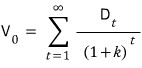

The value of a stock is the sum of the future cash flows expected from holding the stock, discounted at an appropriate discount rate

(well, the context seems the same as bonds…. plausible plausible~ bang bang!)

But, you may or may not have heard it said that a stock can also be viewed as a bond with no maturity?

That is, calculating the value of a stock under the assumption “if you were to hold the stock perpetually” is the first button to fasten,

and if you’ve done high school math, this is a breeze!!!!!!

Here too k is the discount rate, that’s right,

um but D_t is the cash flow that occurs periodically from the stock… that is! the dividend, right

As you’ve probably caught on, since we don’t know D exactly for future periods,

stock valuation doesn’t seem easy does it???

Hmm???????

yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah yeah

It’s not easy

No, actually it’s impossible lolololololololololol

lolololololololololololololololololol how would you accurately predict what will happen in the future

What is this, sorcery lolllll

Ah but, even so, there’s one thing we can know!!!!!!

And that is, the content right below.

Let’s keep going.

First question!

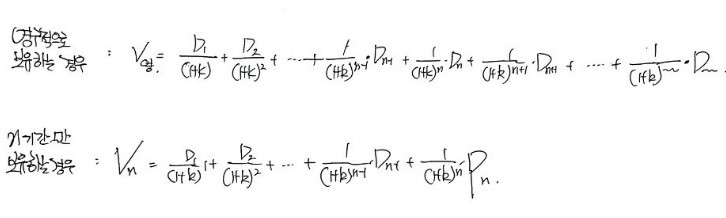

There must be lots of people planning to hold it not for an infinite period, but for n periods,

so how can we do stock valuation for an n-period case???

You’d just have to ‘finitely’ discount the cash flows that will occur and sum them….

Before writing that formula, above it

I’ll write the formula for the case of holding perpetually,

and below it I’ll write the sum for the case of holding for n periods

I wrote it like this????????

Right, you receive dividends up to period n-1 and after selling the stock in period n,

you discount the incoming P_n by an appropriate discount rate to get its present value,

so what do we do about P_n??????????

P_n is the value of the stock at period n, right???

So you’d just have to compute P_n by taking the future income coming in over periods n+1, n+2, n+3, n+4, . . . . . and reducing them to the value at time n,

now you see why I wrote the perpetual-holding case above…?

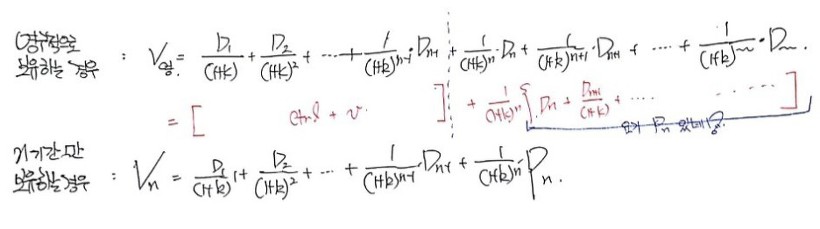

If we mess around just a little with the trailing term above,,,.

Yep…. you can see the two formulas are completely identical.

So in ‘dividend valuation of stocks’, the fact is, whether you hold perpetually or for a fixed period,

the value of the stock is more or less the same — that’s what it tells us!!! (but so what, we don’t know D_t precisely, so we still can’t know exactly what value they’re equal to. Just — whether you hold for n periods or keeeeep holding, the value is the same lolololol)

Phew…. so now let’s somehow handle D_t properly….

How do we handle this… T_T T_T T_T

But, humans want to evaluate value somehow no matter what????

So they end up taking an extreme assumption.

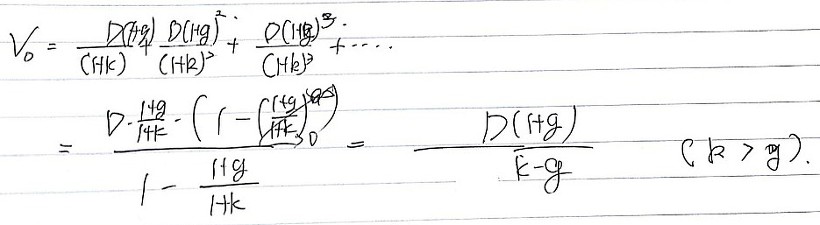

“If the dividend stays constant forever,” they measure the value of the stock under this kind of assumption….

If we assume this, calculation becomes super simple as shown above… T_T

This seems a bit… too unrealistic,

so someone plugged in the assumption “what if the dividend grows at a constant ratio g?” and computed it, apparently…

<cf. This stock valuation model is called the Gordon Model. Or constant growth model>

But, isn’t that kinda overkill too???

How can it just keep growing at g forever?

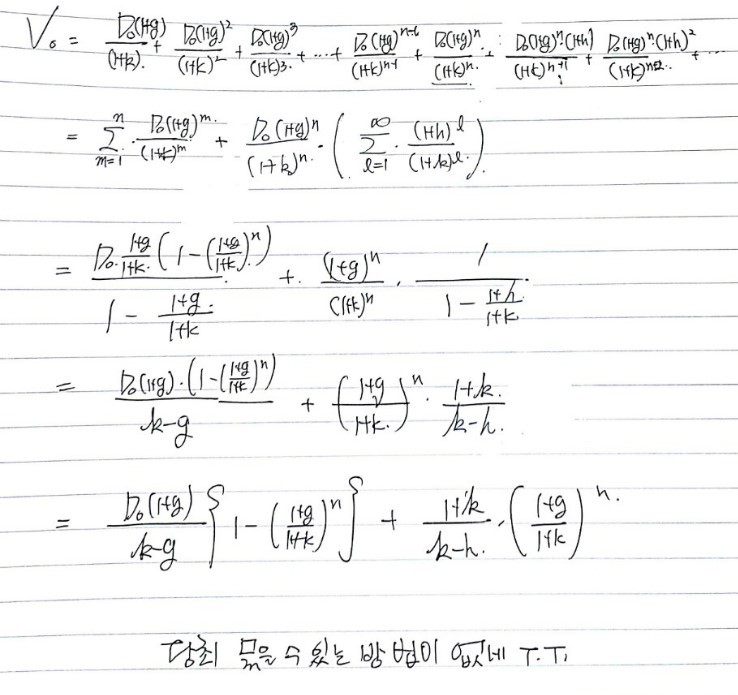

So this time they extended the model a bit with “the growth rate differs by period.”

First, for 2 stages

From 1 to n (stage 1) the growth rate is constant at g,

and from n+1 onwaaaard (stage 2): from this point the growth rate is h!!!

3-stage model

4-stage model?

If you keep extending it, again

it’ll end up converging back to here.. lolol

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.