Liquidity Management and Capital Budgeting Overview

A no-frills terminology dump on liquidity management, working capital, and financing policies — because these chapters sure aren't giving us any practical how-tos. T_T

Personally, since these chapters have no answers to “How to ~ ?”

it’s freaking not fun T_TT_TT_TT_TT_T

I wrote this thinking of it as just sorting out terminology T_T

Liquidity refers to how quickly an asset can be converted to cash at an appropriate price level.

So then, a firm’s liquidity ends up referring to the firm’s short-term ability to pay.

For a firm to avoid falling into insolvency and to maintain liquidity,

it must hold an appropriate level of liquid assets including cash.

But excessive holding of liquid assets has a negative impact on the firm’s profitability (liquid assets contribute little to profitability),

so ’liquidity management’ means maintaining appropriate liquidity,

lowering the risk of falling into insolvency

while keeping profitability appropriately maintained… that’s what’s called liquidity management.

Working capital refers to the liquid assets on the balance sheet.

But, since ‘working capital’ in general is recognized as meaning ’net working capital’,

working capital → “the amount of liquid assets minus current liabilities”

A firm’s liquidity management refers to the management of net working capital,

so what a firm must do well is

not only to manage liquid assets well,

but also to manage current liabilities like accounts payable and short-term debt well!

<That way you catch both rabbits — insolvency risk & profitability, yo!>

- Investment in liquid assets

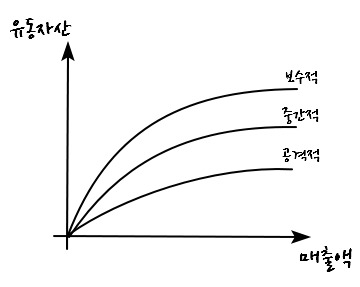

The most important variable in the size of liquid assets is the firm’s sales.

As the firm’s sales increase, liquid assets increase.

Depending on the level of liquid asset holdings, it’s classified into conservative, aggressive, or intermediate liquid asset management policies.

Conservative policy: a policy of holding many liquid assets to focus on maintaining the ability to pay

Aggressive policy: a policy of holding relatively few liquid assets to focus on maintaining profitability

Intermediate policy: a character intermediate between the two policies

- Investment in liquid assets and financing

A firm raises the necessary funds, secures cash, and invests in liquid assets other than cash.

- Aggressive financing policy

Also called the hedging method, it’s a policy of raising short-term funds with short-term debt

and raising long-term funds with corresponding long-term debt or equity.

(As a method of raising funds matched to the period of short- and long-term fund needs, it’s also called the maturity matching method.)

This minimizes idle capital and minimizes interest expense, so it doesn’t impede the firm’s profitability, but because dependence on short-term debt is large and surplus funds aren’t sufficient, if things go sideways it can fall into insolvency.

- Conservative financing policy

a method of raising all necessary funds with long-term capital,

this always holds funds with leeway, maintaining abundant liquidity, so there’s no risk of falling into insolvency,

but profitability will be lower than the aggressive financing policy.

Excessive investment in liquid assets can lead to the loss of opportunities to earn profits.

This is called ‘opportunity cost’, right? Also, not only opportunity cost, but they say excessive interest expense can impede profitability even more more more more.

Management of liquid assets

- * Cash management

We said that liquid assets are funds that can be converted to cash in a short period, right?

There would be things like marketable securities, accounts receivable, inventory and so on,

and among these, the one a firm must handle most importantly should be ‘cash’!

Cash is the asset with the greatest liquidity, but as much as it has the greatest liquidity, it’s a non-profitable asset,

so from the firm’s standpoint it’s gotta minimize this guy.

But if there’s also too little of it, it might not be able to exert force in a short-term crisis, so it has to maintain an appropriate level.

- - 1. Cash inflow/outflow management

Management that maintains an appropriate level of cash holdings while efficiently managing the inflow and outflow of cash.

First, the inflow of cash must have no leakage, and must be quick! And, outflow must be delayed as much as possible!!!

- Determining cash holding level

: yeah, appropriately

- Marketable securities management

: The marketable securities here refer to securities that are easy to convert to cash and can be made into a short-term investment target.

Then how should marketable securities be selected?

1. First, shouldn’t you evaluate the credit of the entity that issued the marketable securities?

<Those issued by the state or public enterprises would have no risk, but their profitability is correspondingly low, so consider this kind of thing>

- Right now we’re choosing marketable securities as part of liquidity management,

so you have to consider importantly whether the security can be easily sold at an appropriate price when needed.

- Marketable securities should be invested by forming an appropriate portfolio. (for diversified investment)

- Inventory management

: Appropriate inventory management is also essential. A shortage of inventory hinders business activities,

and excess causes large costs in inventory management and induces a decline in inventory value, so it must be managed.

The optimal holding level must be determined considering sales volume, inventory management cost, production lead time, durability of products, etc.

< For coping with contingent situations: safety stock>

- 1. Inventory holding cost

cost incurred in storing and maintaining held inventory

ex. losses from spoilage, theft, etc., property tax, insurance, etc. And also note that the cost of capital invested specially in inventory is included in holding cost.

- Inventory ordering cost

: cost incurred from ordering inventory until it arrives. ex. ordering cost, transportation cost

- Opportunity cost

: cost caused by inventory shortage. ex. loss of sales opportunity, loss from disruption of production activity

- Accounts receivable management

: Accounts receivable arise when there are amounts not yet collected out of operating sales.

Accounts receivable are influenced by the firm’s credit policy. There are 3 of them, continuing below

- Credit period

: the repayment period for accounts receivable allowed to customers in transactional relationships

the period that may be required from purchasing goods on credit until paying the amount

The length of this credit period is appropriately determined according to internal and external situations such as economic conditions, customer characteristics, product profitability, fund situation, etc.

If the credit period lengthens, sales can increase due to an increase in customers,

but because accounts receivable increase, opportunity cost, accounts receivable collection cost, etc. can increase.

- Credit standards

: criteria for determining customers to whom credit transactions will be allowed

If this is loosened, sales will increase due to an increase in customers.

But, this will also incur accounts receivable collection cost, opportunity cost, etc., right??

But if you make the standards strict, sales will decrease,

so it must be appropriately determined through sufficient consultation among each department.

- Discount policy

: a policy that aims to increase customers and shorten the collection period of accounts receivable by giving customers certain benefits related to payment.

However, if the discount rate increases, the collection period is shortened so collection cost can be reduced, but profitability on sales can decrease (it should be determined at the level where the decrease in collection cost equals the decrease in sales profit).

- Current liabilities management

: Current liabilities are debts that must be paid in the short term, debts that must be repaid within 1 year,

a firm’s current liabilities include ‘accounts payable, bank short-term loans, commercial paper’, etc.

If you raise funds using short-term debt, there are advantages compared to long-term debt such as shorter time required for fundraising, lower cost, etc., but

since you have to constantly check fundraising & repayment, in a sudden situation you can fall into insolvency risk.

- Accounts payable

: arises by delaying payment of amounts. This way it can become a short-term financing source.

But if the amount is paid in cash, in cases where there is a discount, an opportunity cost of giving this up arises.

- Bank loans

: this is what firms use most,

procedures are complicated, and interest on the loan is incurred differently depending on principal and interest repayment ability.

- CP (commercial paper)

: a means of raising short-term funds by issuing notes promising payment by a set deadline.

In this, there is a broker between the firm and the investor, and through the intermediary institution the issued note is discounted and purchased and sold to investors, so they can scrape a living off the discount-rate difference as a kind of fee.

The discount rate is applied differently according to the credit evaluation done by the intermediary institution.

Chapter 6. Overview of capital budgeting.

- The meaning of capital budgeting

Capital budgeting is the field that deals with the comprehensive plan related to investment activities carried out from a long-term perspective in a firm.

Mainly for investment in real assets corresponding to tangible fixed assets such as machinery and equipment, buildings, etc.

And it’s recognized as a systematic management activity for making investments rationally.

It’s classified into searching for investment proposals, estimating cash flows for investment proposals, evaluating the economic viability of investment proposals, formulating and allocating financing plans, etc.

The most core thing is “economic viability evaluation” → this is concentrated on in chapter 8.

(In general, capital budgeting is said to mainly mean the economic viability evaluation of investment proposals.)

* Importance of capital budgeting

- Capital budgeting mainly deals with investment decisions related to production facilities, so the investment effect cannot appear immediately.

These investments can bring great influence and constraints on the firm’s future activities, so they’re very important.

- The investments dealt with in capital budgeting are large-scale investments that require a lot of funds.

Facility investment in fixed assets related to a firm’s production activities

requires more funds than any other type of investment, so you have to be more more more more more more careful.

If you do this wrong, liquidity deterioration is greatly affected!

- From a strategic perspective, to gain a competitive advantage, you have to do well.

<Yeah—— thanks for the super-obvious lecture.>

The order of capital budgeting.

- Searching for investment opportunities

: The stage of finding investment opportunities so they can be put into action by analyzing the firm’s internal capabilities and external environment.

Investments aimed at expanding existing facilities, investments aimed at developing new products,

investments aimed at replacing existing facilities, various kinds…

- Setting investment proposals

: the stage of selecting concrete investment proposals that can achieve investment objectives.

- Measuring cash flows

: when the investment proposal is adopted, measure the expected cash outflows and inflows and calculate net inflow

- Evaluating investment proposals

: the stage of evaluating the economic viability of investment proposals based on the measured cash flows of each investment proposal

the stage of selecting by considering the firm’s management strategy, financing capability, internal and external environment.

- Execution and management of investment

: the stage of executing the investment, management of whether the planned investment is being carried out

if problems are discovered, the stage where capital budgeting is modified and post-investment management is carried out.

Classification of investment proposals.

- Classification by purpose.

- Replacement investment

: investment to replace existing equipment with new ones, physical obsolescence done because existing equipment has aged

it can be classified into those due to technological obsolescence in which existing old equipment is replaced with new production technology equipment.

- Expansion investment

: investment to expand existing facilities.

Done when current production capacity is expected to be hard-pressed to handle future demand.

That is, accurately predicting future demand must be done first.

- Product investment

: investment to improve or upgrade the quality of existing products that the firm produces, to produce new model products.

Or investment to produce products of a totally different concept from existing products.

- Strategic investment.

: literally investment from a strategic dimension where the effect of investment is expected to be the greatest.

ex. R&D investment, welfare investment, pollution prevention facility investment, etc.

- Classification by investment relevance

- Independent investment

: an investment in which the adoption of one investment proposal has no effect at all on the cash flows that occur when other investment proposals are executed

(Each investment proposal can be evaluated and analyzed individually to execute capital budgeting.)

- Dependent investment

: an investment in which the adoption of one investment proposal affects the cash flows of other investment proposals.

Such investments are classified into complementary investments and substitute investments.

- a. Complementary investment.: a case where the adoption of one investment proposal increases the cash flows of another investment proposal

ex. an investment proposal to build a gas station on two adjacent plots of land, and an investment proposal to build a parking lot (mutually complementary relationship)

- b. Substitute investment: a case where the adoption of one investment proposal decreases the cash flows of another investment proposal

. an investment proposal to purchase the same equipment as existing equipment, and an investment proposal to purchase equipment with new technology (mutually exclusive relationship)

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.