Cash Flow Estimation

A casual walkthrough of cash flow estimation for investment evaluation — covering incremental flows, opportunity costs, sunk costs, depreciation, and more.

Since I haven’t studied tax law or accounting, it’s a bit awkward for me to explain this part,

but it’d also be awkward to just skip it;;;;;

so I’ll just briefly hit the keywords and move on.

Chapter 7. Estimation of Cash Flows

Since the evaluation of an investment is based solely on cash flows, measuring the cash flow of an investment is essential.

The cash flow of an investment must consider and forecast all items that affect cash flow until the end of the investment’s lifetime.

“Cash flow” refers to the net cash inflow, calculated by subtracting the cash outflow expected to occur due to the investment from the cash inflow expected to come in.

net cash flow = inflow - outflow

But net cash flow is

classified into three categories — before the facility starts operating / while the facility is operating / and then the final period when the investment facility’s lifetime ends —

and respectively called

initial cash flow / operating cash flow / terminal cash flow.

Before looking at the specific calculation process for these three,

let’s go-go-go-go-go and get these down — a few important “considerations” when calculating each cash flow.

- Cash flow is incremental (Δ).

First, in calculating cash flow, this “cash flow” only counts the additional cash flow measured due to the investment.

This means the difference! between the cash flow measured when a particular investment is chosen and the cash flow when that investment is not chosen.

- Opportunity cost

The cost incurred by giving up the best alternative when the investment is executed.

ex. Say you already bought land a long time ago as a site to build a factory,

and that land could be sold right now for 1 billion won — the opportunity cost is 1 billion won.

(This must be included in investment evaluation.)

- Sunk cost:

An already-past, useless cost that cannot be tied to a particular investment.

This should NOT be included in investment evaluation.

ex. Market research cost

- Side effects

When an investment is chosen and executed and that investment affects the company’s existing investments, causing cash flow to change — the effect that occurs at that time.

ex. Launching a new home appliance could reduce sales of existing models. (An example of cash flow decrease due to side effects.)

- Interest expense

Cash flow only takes as its evaluation target the cash flow obtained as the result of operating activities from the invested assets.

So, since interest expense paid during the capital procurement process has nothing to do with operating activities, it is not reflected in cash flow.

In other words, cash flow is calculated under the assumption that there is no debt capital.)

- Depreciation expense

Depreciation expense also should rightly not be included as a cash outflow of investment cash flow.

However, depreciation affects tax calculations. (Depending on the tax rate, there’s no way cash flow isn’t affected…)

- Net working capital investment

When executing an investment, you don’t invest only in fixed assets — generally, it’s also accompanied by investment in current assets like inventory and accounts receivable. The increase in net working capital at this time (current assets - current liabilities) is included in cash outflows.

(Current assets and current liabilities are things that are turned into cash or repaid within a year. So net working capital investment is recovered or reinvested on a yearly basis.

In other words, in the terminal year, the previous year’s net working capital investment is recovered and included in cash inflows, and after that no more occurs and it ends.)

- Tax effect

When measuring cash flow, taxes are clearly treated as cash outflows, so the existence of taxes affects cash flow in various ways.

a. Earlier, we assumed cash flow is under the case of no debt capital, so for taxes too we’ll assume there’s no interest expense arising from the existence of debt capital.

b. When disposing of existing fixed assets such as machinery equipment, cash flow must be measured taking tax effects into account.

ex. When selling a machine, if there’s a difference between the machine’s book value (or residual value) and the selling price (market value), the tax effect must be reflected.

If the selling price is greater than the book value, it’s considered that a gain from the disposal of fixed assets has occurred, and tax is imposed on the gain; conversely, if the selling price is less than the book value, it’s considered that a loss from the disposal of fixed assets has occurred, and a tax reduction effect of that amount occurs.)

“Cash inflow from sale of fixed asset = selling price - (selling price - book value) × tax rate

c. If there’s a tax reduction effect from an investment tax credit, cash flow must be calculated taking this into account. The investment tax credit system is a system that deducts from corporate tax an amount corresponding to a certain percentage of the investment amount, in order to induce corporate investment.

d. Depreciation expense is not treated as a cash outflow, but it brings about a tax reduction effect that decreases taxes.

So depending on which depreciation method you use, the tax reduction effect differs.

“Tax reduction effect from depreciation = depreciation expense × tax rate

Measurement of cash flow

initial cash flow / operating cash flow / terminal cash flow

We’ll break it down into these three!

- Initial cash flow:

Cash flow related to the initial investment amount incurred by purchasing assets.

First, calculate the cash outflows such as the purchase and installation cost of the new asset and the increase in net working capital,

and when the new asset replaces an existing asset, calculate the cash inflow that occurs when the existing asset is sold.

Don’t forget that when there’s an opportunity cost, the opportunity cost also has to be reflected in cash flow.

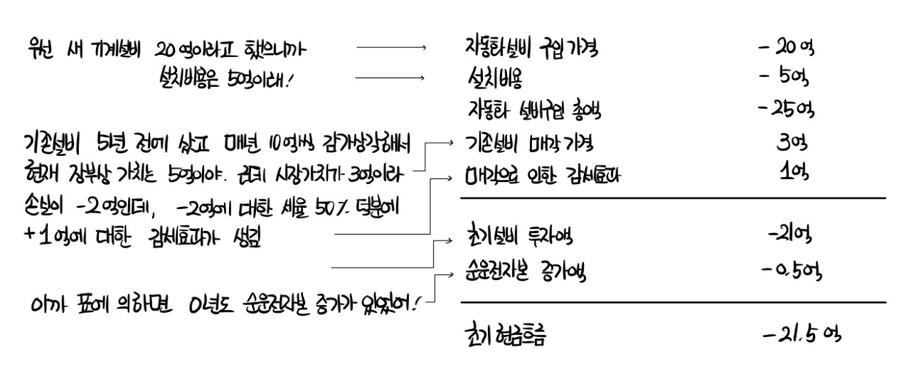

-> Ex. Case

Hanguk Corporation, which produces personal computers (PCs), is trying to replace part of its existing production facility with an automated facility.

The purchase price of the new automated facility is 2 billion won,

and the installation cost of the facility is 500 million won.

The useful life of the new facility is 5 years, and after the useful life ends, the book residual value is none, but the market value is estimated at 400 million.

Depreciation uses the straight-line method.

The existing facility to be replaced was purchased 5 years ago with a useful life of 10 years at the time of purchase,

with a purchase price of 1 billion won, and after the useful life ends, both the book residual value and the market value are estimated to be none.

As a result of depreciating using the straight-line method at 100 million won per year, the current book value is 500 million won.

Korea’s corporate tax rate is 50%.

The market value at which it can currently be sold is 300 million won.

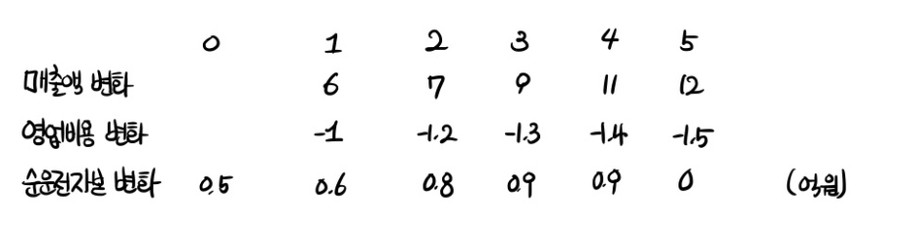

When the existing facility is replaced with the automated facility, the expected increase or decrease in sales and operating costs, and the size of net working capital, are as follows.

Let’s calculate the initial cash flow with this information.

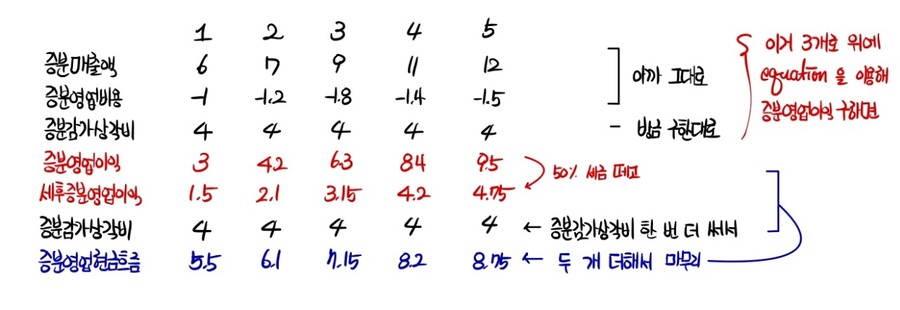

- Operating cash flow

When initial investment is completed and the facility operates normally, cash flow from operating activities (in terms of the incremental concept) is

calculated by the formula below.

Incremental operating cash flow

= (1 - corporate tax rate)(incremental sales - incremental operating cost - incremental depreciation) + incremental depreciation

= (1 - corporate tax rate) × incremental operating income + incremental depreciation

= after-tax incremental operating income + incremental depreciation

※ Note: depreciation is an item that cannot be recognized as a cash outflow. However, since taxes are cash outflows, for the calculation of taxes, incremental depreciation must be subtracted from incremental sales together with incremental operating cost.

Continuing from the above case,

I’m going to calculate the operating cash flow. As the above formula says, we need incremental sales, incremental operating cost, and incremental depreciation, and earlier in the table we had sales and operating cost!

If we just figure out the incremental depreciation, we can find the incremental operating cash flow!

The new facility cost… earlier the total facility purchase was 2.5 billion, and since the useful life is 5 years and we said we use the straight-line method, subtract 500 million each year.

So is the incremental depreciation 500 million every year? NoNo!!!! Since it’s incremental, we have to do it as “after minus before”, so

incremental depreciation = 5 - 1 = 4

Okay, now let’s write it down.

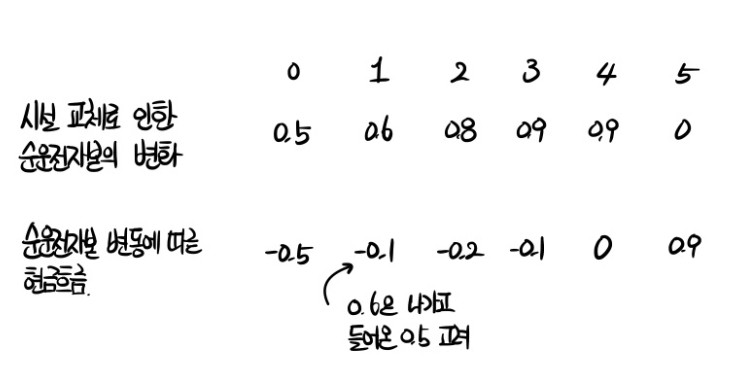

At the step of calculating the ‘operating cash flow’ during the normal-operation period, we have to calculate the ‘additional cash flow due to changes in net working capital’.

Earlier in the bottom row of the first table there was an item corresponding to the net working capital change,

so if we just write that down first,

Hmm, net working capital investment has the nature of being recovered and reinvested on a yearly basis,

so the net working capital increase of 50 million in year 0 is recovered and deducted in year 1! Let’s calculate the cash flow computed this way.

- Terminal cash flow

The terminal cash flow is the cash flow of the year in which the investment period ends.

The terminal cash flow will consist of incremental operating income, the net working capital investment recovered at the end, and the sale of the facility that has reached the end of its life.

And taxes have to be considered too.

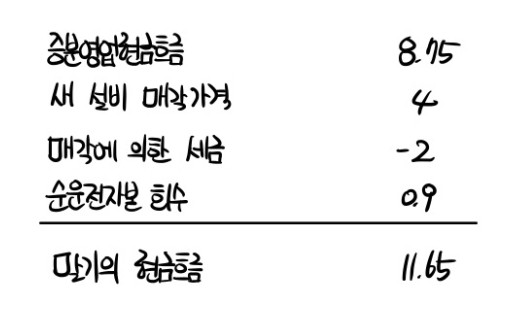

Let’s look at the final year 5 from the corporate case we’ve been handling.

First, incremental operating income in year 5 is 875 million won, cash flow from net working capital is 90 million.

These we’ve already calculated, so now let’s sell the new machine.

Since we said the new facility’s useful life is 5 years, there’s no book value now.

But we said the market value is 400 million!

Oh then is the whole 400 million a gain?! This is also No No — after taxes, only 200 million comes into the company.

Huh, then I guess the terminal cash flow is done!

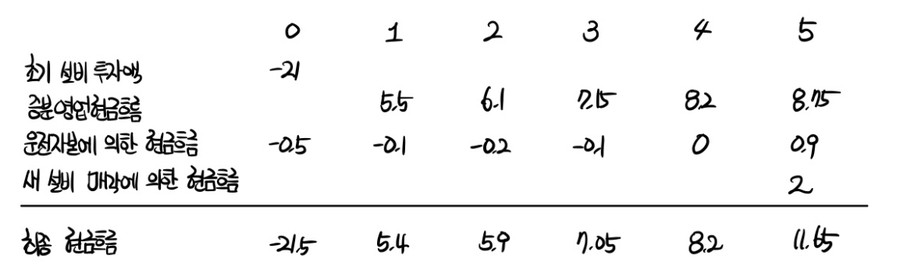

So finally, all cash flows are written out at a glance like this.

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.