Cost of Capital

Before diving into capital structure theory, let's get the basics straight — cost of debt, cost of equity, and why k is the discount rate that actually matters.

In the post after this one, I’m planning to cover “capital structure theory,”

and to do that, I think I need to organize some terminology first.

So that’s the post I prepared, well….

Well anyway… I wanted to menshun that the really important content comes after this?????

So let’s lightly get into organizing it.

Cost of capital means….

It’s a ‘cost’ incurred in return for using capital, cost.

To put it simply, it’s interest, interest.

But, would a company raise funds by borrowing money from a bank???

Rather than that, they’d raise funds by issuing bonds or stocks.

But, bonds and stocks have different natures…

A bondholder who buys a company’s bond

will provide funds to the company, and these funds are a liability for the company, a liability.

Liability is the concept of ‘other people’s capital.’

That is, the cost of capital on debt (bond interest) can be called “cost of debt.”

But stocks are a bit different.

For one, the compensation for using the funds obtained from shareholders goes out in the form of dividends, and

stocks are actually an equity stake in the company, right???

So the funds obtained from shareholders are not debt but the company’s “equity.”

That is, the compensation that shareholders get for providing funds should be called “cost of equity” rather than cost of debt~~ that kind of thing~

That is, the compensation for using capital can be divided into two like above: cost of debt and cost of equity.

<Bonds are low risk, so the yield is low to match, and stocks carry big risk, so in exchange the yield is correspondingly high~ that’s reasonable, reasonable>

Anyway, from the company’s perspective, they can’t get money for free,

so the interest or dividends paid in return are clearly costs,

but from the investor’s perspective,

the reason investors provide funds is to earn returns, isn’t it????

They’re providing funds in order to earn returns.

That is, that cost of capital to the company, thought about from these folks’ perspective, is the expected return, so

from the company’s perspective there’s something called the “minimum required rate of return” that must be realized.

<If the company can’t even realize this, investors will exit, and then the stock price will fall, right?>

So!!! the cost of capital is used as the discount rate (I’ll call the discount rate k.)

Well~ from the company’s perspective, since they have to provide k to investors in return for using the money,

the company has to fatten up its money at k.

No, it has to fatten it up at “at least” k, is what I’m saying.

Ah… then when discounting future money to present value, discounting at k kind of feels a bit more intuitive now.

Now, and an important conclusion!

The company must minimize the cost of capital k in order to maximize the value of the company (enterprise value)!!!!

But this cost of capital was divided into two, right?

Cost of debt and cost of equity?

What would be most appropriate to say “the cost of capital of the firm” is?

Probably just recklessly saying it’s the average between the two would be problematic.

I think it’d be most reasonable to take the “weighted average” of the respective costs of capital based on the ratios of debt and equity within total capital.

Then we first need to know how to compute each cost of capital before we can take a weighted average!!!

How do we compute each cost of capital?!

As mentioned earlier,

the cost of debt is the interest paid to bondhodlers, right?

This we can easily calculate.

If we write: annual interest amount I is what ratio of our total debt B??!?

If written that way, this k_D, which serves as the ‘coefficient of proportionality between the two,’ refers to “the ratio of annual interest I within total B,”

that is,

we can calculate k_D (cost of debt) from B and I, which we can observe.

But, for this interest expense, corporate tax has to be paid.

So on the cost we used, there’s corporate tax that goes out as t.

(t: corporate tax rate — if you think of the t as in tax, not the t as in time, it won’t be confusing)

So the more substantive cost of debt

is the after-tax cost of debt, which is

is the point!haha

Okay, now cost of debt is done, so let’s think about how the cost of equity going out through stocks etc. is calculated.

This one’s a bit tough because, unlike bond interest where how much will go out is already determined, so saying we don’t know the I value is a bit of a stretch,

since no one in the world knows how much the dividend will be, accurately measuring the cost of equity is actually said to be difficult. No, it’s just impossible, impossible.

But, this cost of equity, from the investor’s perspective, can be called the “minimum required rate of return,” right?

What’s the minimum required rate of return for an investor????

“The expected return determined by CAPM!!!!” — saying that is probably appropriate at our level.

It’d be fine to call the μ_i determined as above the cost of equity!!

Ah but, I don’t know CAPM!!!!

If you don’t know???????? ( http://gdpresent.blog.me/220891746214 you can read here )

CAPM(Capital Asset Pricing Model) [ Financial Management As I Studied It #12 ]

The content here is CAPM (Capital Asset Pricing Model), but before the full-fledged CAPM talk…

gdpresent.blog.me

For people who are like, I hate this!!! ( http://gdpresent.blog.me/220837271551 you can read here too)

Valuation of Bonds and Stocks [ Financial Management As I Studied It #4 ]

Previously, while saying that finance is an aristocratic field, the aristocrats said to a clever lower-class person, “Hey~ I’ve been promised to receive X amount in Y years…

gdpresent.blog.me

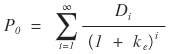

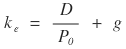

We said that the cost of capital is used as an appropriate discount rate for the company’s money, (let me call cost of equity k_e~yo)

then the value of a stock would be the sum total of all future dividends discounted by that k_e — that would be the current value of the stock.

If we do it like this, we can estimate k_e by trial & error method~

But honestly, we can’t know one by one what value each of D_1, 2, 3, ~~ would be, right…

So like in the earlier Chapter 4, if we insert the somewhat forced ‘assumption’ that

D_1 = D_2 = D_3 = ~~~~ = D

all of them are constant at D,

we could value the stock like this,

and then we can reach the conclusion that we can calculate k_e!

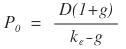

Since this is so unbearable, when we assume D grows at a constant growth rate g,

that stock valuation is done like this — that content was in Chapter 4.

Then here we

can say that the cost of equity

is determined as above.

But you know? Stocks can roughly be divided into two kinds, right?

Common stock which has voting rights, and preferred stock which has no voting rights but receives dividends first?????

Since preferred stock actually has “the dividend amount to be paid specified,”

so actually the cost of capital of preferred stock

can be valued as above….haha

But, preferred stock, unlike bonds, has no obligation of interest payment???? Well, there’s that kind of difference.

Even so, in the next post I’m gonna use CAPM rather than this kind of content;;;;;;hahaha

*Cost of capital of retained earnings

Retained earnings are the earnings left after paying dividends out of net income,

and since firms do investment activities using these retained earnings, it can be seen as a firm’s means of raising capital.

There’s also a cost to using these retained earnings —

since they were retained for investment instead of paying dividends to shareholders,

shareholders can be seen as wanting at least the minimum rate of return obtained from reinvestment back again, right?!?!

We could see this as the cost of capital for retained earnings.

But, thinking from the firm’s perspective,

if we hadn’t retained the earnings and spraed it all out as dividends,

the firm would have issued stock to raise funds, and the cost of equity would have been consumed~ ya could think that way.

So we can say the cost of retained earnings is the same as the cost of equity,

and we can also say the retained earnings have already been reflected in the cost of capital,

so we’ll consider that the cost of capital, as we saw above,

has these 2 — cost of debt, cost of equity — is what we’ll go with.

Almost, the retained earnings cost of capital is supplementary content.

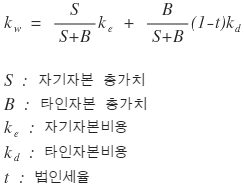

Then, from the firm’s perspective, how much should we say the overall cost of capital is consuming???

Cost of debt k_B and cost of equity k_e are different??

We slightly mentioned earlier that we would weight the capital a firm is using by ratio

and take the average.

The cost of capital thus taken as a weighted average

is called “weighted average cost of capital: WACC”;

The weighted average can probably be taken like this

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.